Reduced volatility combined with environmental impact: the case for green short duration bonds

Short duration green bonds offer the investors lower volatility than longer-dated bonds in a time of economic uncertainty while making a measurable, positive environmental impact.

At a time of high uncertainty driven by tariffs threats, geopolitical tensions and fiscal slippage, the outlook for bonds has never been less clear. While valuations are attractive, with long-term yields close to historical highs, the macroeconomic backdrop means that bond markets are experiencing heightened volatility.

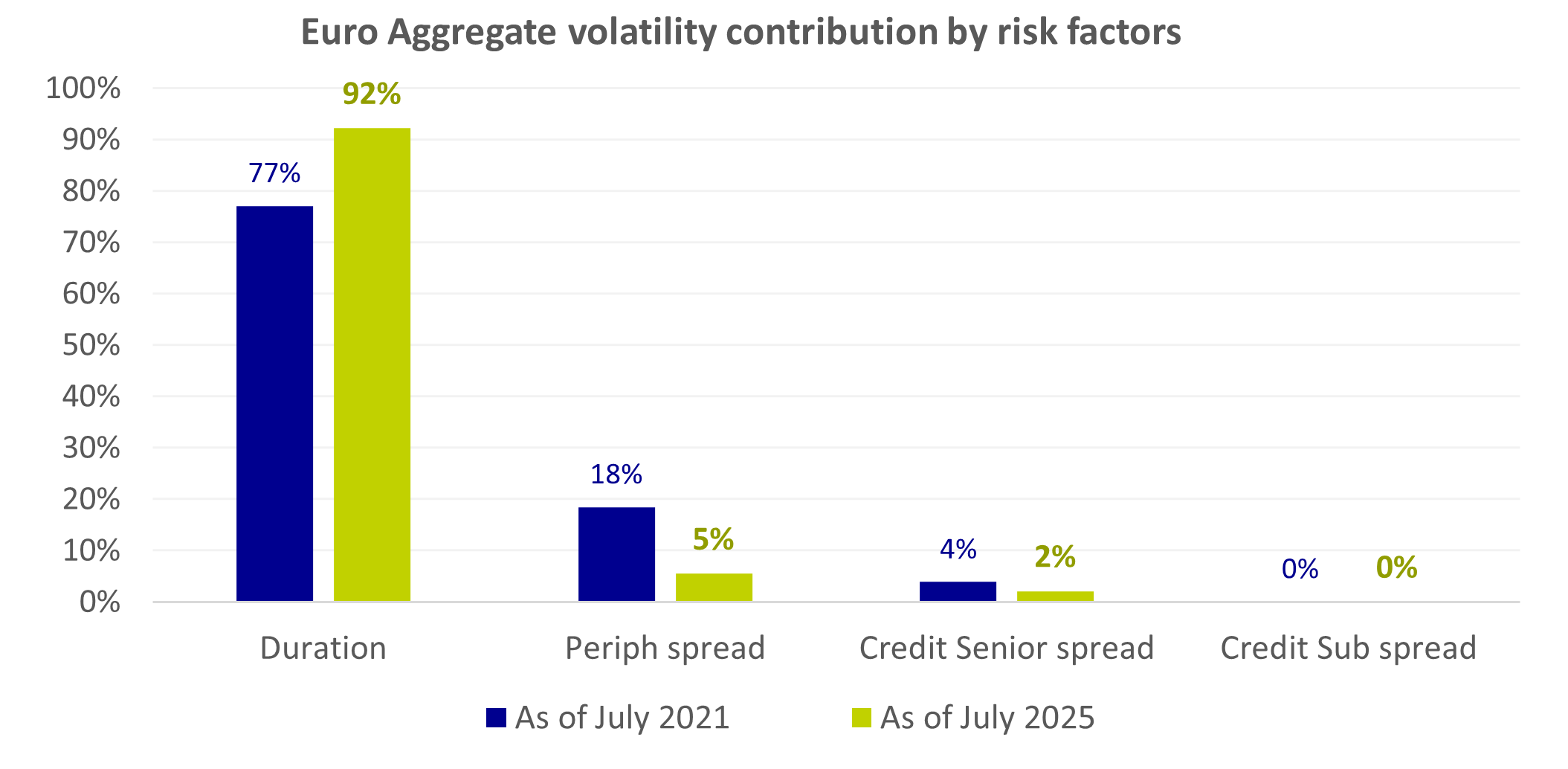

The bond market volatility has increased significantly over the past few years, with interest rate risk being a significant factor. In fact, duration risk – driven by interest rates - now makes up 90% of volatility for bonds.

Rates volatility now accounts for around 90% of volatility

Source: ICE, AXA IM as of June 30, 2025. The risk factors are constructed to explain the source of return and volatility of asset classes, they are mutually independent to ensure that any interdependence between them has been eliminated. We use Euro Aggregate to illustrate as green bond market is dominated by EUR issuances and exhibited more than 95% historical correlation with Euro Aggregate.

This has made short duration bonds look attractive. A shorter maturity profile not only reduces overall volatility but also helps balance volatility contributions from the rates and the spread component, bringing them closer to equilibrium.

With central banks cutting rates more or less aggressively over the past year, this could be a good time opportunity step out of money markets to get exposure to higher potential returns from the bond market without taking too much additional risk.

The Green bond opportunity

These drivers are seeing more investors take an interest in short duration strategies. But the environmental impact of a portfolio can also be a concern, especially for mandates with significant environmental ambitions.

This is where green bonds come in.

Green bonds are bonds that direct capital towards environment-friendly projects. They can finance renewable energy, green buildings or low carbon transport, as well as sustainable ecosystem projects such as biodiversity preservation and water-related infrastructure.

The risk is the same as a conventional bond, but issuers provide additional transparency, identifying the projects funded and providing reports with dedicated KPIs to measure the projects’ positive impact.

The green bond market has grown significantly over the past few years, reaching US$2 trillion in 2025. It has developed into a diversified global market covering many sectors and regions.

The UK has a growing green bond market, with the UK government having issued close to £70 billion, while corporate issuers like National Grid, SSE or Segro Capital are using green bonds to fund their low-carbon transition investments.

European issuers still dominate, but the UK now accounts for close to 5% of the total green bond market. This has happened despite the absence of UK Green Taxonomy, illustrating the attraction of using green bonds to fund the carbon transition and demonstrate commitment.

This growth is a dynamic source of investment opportunities, and the green bond sector now offers the granularity to build exposure with specific risk profiles, like short duration, combining the benefits of a short duration portfolio with enhanced environmental impact.

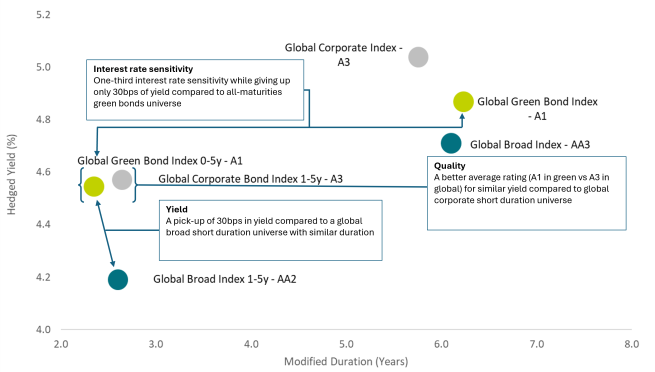

Green short duration bonds compare favourably to other segments of the bond universe

While the green bond universe offers a well-balanced exposure across sovereigns and credit debts, the short duration segment has a higher exposure to credit. Sovereigns have tended to favour longer time scales to fund the net zero investments, while around 75% of the short duration universe is made up of financial and corporate debts.

In a world where carry cannot be ignored, this provides a good opportunity to reduce interest rates risk without conceding too much yield. Breaking down

When comparing the broad green short duration bonds with other segments of the broad and green bond universes, we see benefits in terms of interest rate risk, quality and yield.

Delivering impact with green short duration bonds

Of course, the opportunity in green bonds is not just financial. Green bonds offer investors the unique opportunity to direct capital directly towards climate-friendly projects and measure their benefit to the environment with reliable KPIs.

The funding gap to enable a just transition to a low-carbon economy is significant and green bonds are well-placed to channel much-needed capital to the critical investments needed in key sectors like energy, transport, and buildings. They offer the chance to support issuers that are putting their own capital to work to meet their climate mitigation objectives and are already on a pathway to decarbonization.

Delivering impact requires not just investing in green bond projects and the KPIs that illustrate their benefits, but also through engagement with issuers. Green bonds are a great entry point for engagement, and green bond issuers tend to be more open to – and constructive on – discussions about sustainability than regular issuers.

At a time when studies demonstrate the positive impact green bonds deliver when accompanying net zero transition (for example, BIS study showed how green bond issuers decarbonize faster than non-green bond issuers1) this represents a unique opportunity for investors willing to benefit from the attractiveness of the bond market, with limited rates exposure while delivering tangible environmental and societal benefit.

- {https://www.bis.org/publ/qtrpdf/r_qt2503d.htm;BIS Quarterly Review March 2025}

Disclaimer

Not for Retail distribution: This marketing communication is intended exclusively for Professional, Institutional or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

Risk warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.