Low volatility risk-adjusted fixed income returns in turbulent times

When markets get choppy, active, unconstrained and diversified fixed income strategies could help investors smooth out volatility while generating attractive fixed income risk-adjusted returns. Nick Hayes, portfolio manager of the AXA Global Strategic Bond Fund outlines why.

We believe the most important factors to deliver low volatility risk adjusted fixed income returns across the full market cycle are:

1. Allocating across both interest rate and credit spread risk

2. Tactically managing duration positioning

3. Maintaining structural diversification.

These become even more vital when markets are turbulent and the economic outlook is far from certain.

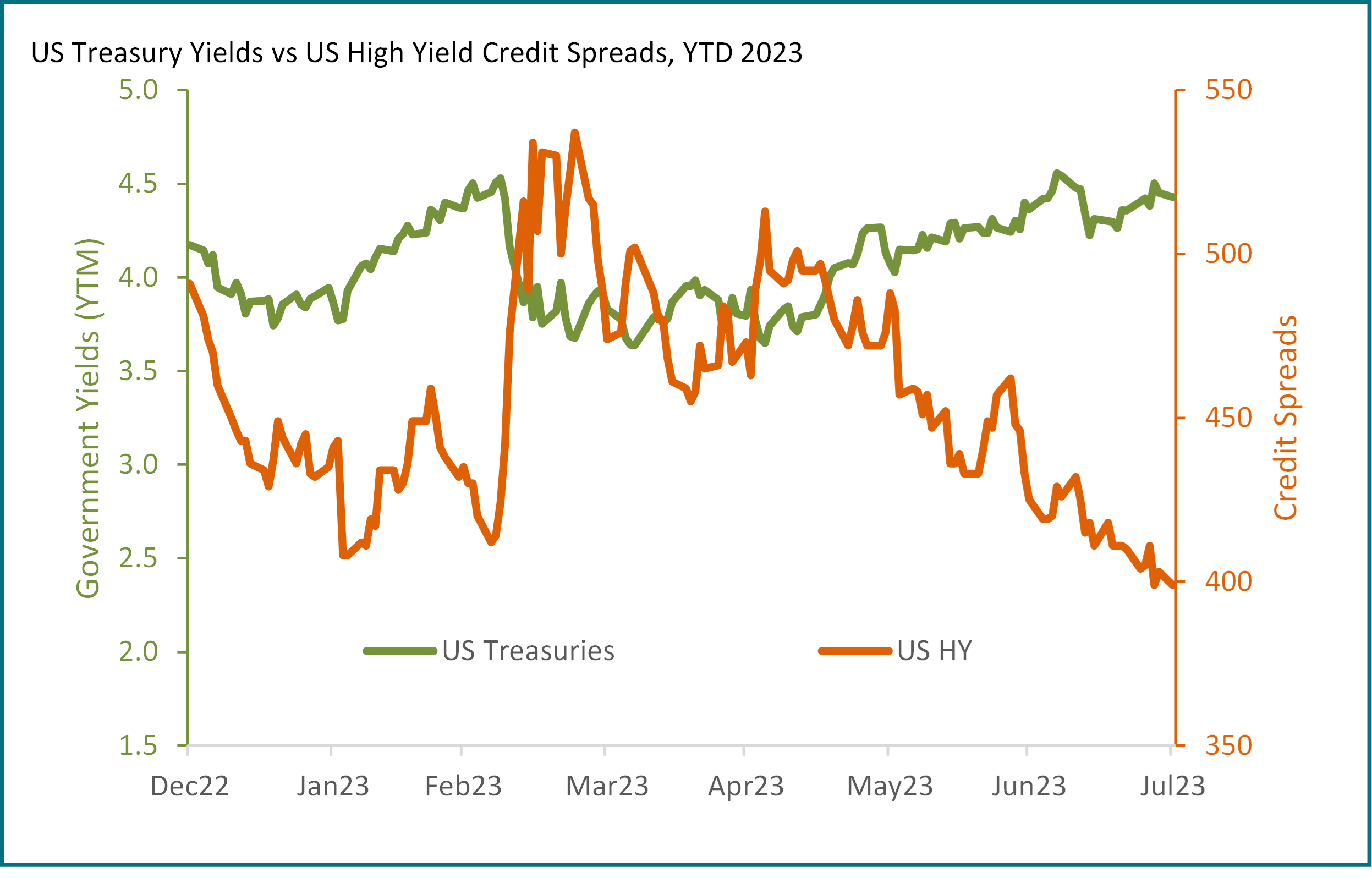

Markets are moving sideways but rates and spreads are negatively correlated

It doesn’t require any special insight to know that markets have been especially difficult in 2023. Government bond markets have swung by 30 to 50 basis points in both directions in very short order throughout the year, while credit spreads have ground tighter, although individual credit events have caused shorter-term spikes. Across the full fixed income spectrum, yields have trended sideways rather than downwards.

While this persistent volatility has been challenging, we have seen a return to the negative correlation between interest rate sensitive and credit spread sensitive fixed income assets over 2023 as government bonds have rallied in the face of credit sell offs and vice versa. This negative correlation is something managers who invest across the full fixed income asset class spectrum can take advantage of.

Negative correlation between credit spread and interest rate sensitive fixed income assets

Source: AXA IM/Bloomberg as at 31 July 2023. Past performance is not a guide to future returns.

We are nearing the end of the rate hiking cycle

All major central banks hiked rates by 25bps at their last policy meetings and emphasised that further moves will be data dependent. And what is the data telling us? Amongst the noise, economic data indicates that inflation is coming down, albeit at different speeds in different markets.

This indicates to us that we are nearing peak rates. We may see a plateau before central banks start to cut –we expect the US to be first, followed by the euro area, while the UK still has some way to go in its fight against inflation.

Being forward-looking by nature, markets tend to become more volatile towards the end of hiking cycles as investors start trying to calculate what the peak, possible pause and eventual cuts could mean. We believe this is what we are seeing now – government bond yields are trending sideways rather than down, and credit spreads pushing out the expectations of a recession.

Active and Unconstrained

The global fixed universe is vast, and we like to think of it as many different sub asset classes, each to some degree driven by one of the two main fixed income risk factors, interest rates and credit spread, or a combination of the two. We do not view one risk factor as more severe than the other, but rather as different types of fixed income risk affecting parts of the fixed income asset classes differently.

The highest quality assets – government bonds and high-quality credit – are more susceptible to interest rate movements. As we move down the spectrum into lower quality credit and high yield, credit spread become more influential.

Where we are in the market cycle also determines how dominant each of these two risk factors becomes. In a slowdown and recessionary phase, rate-sensitive assets will drive fixed income returns; in a recovery and expansionary environment, credit spread-sensitive assets drive returns.

Active managers who take an unconstrained approach can tap into the full fixed income universe and find opportunities throughout the market cycle. From a top-down perspective, we can consider where we are in the market cycle and from a bottom-up perspective, we can consider which risk factors will dominate a particular issuer.

A third consideration for active fixed income managers is duration. Being active and unconstrained means we can choose our outright duration position and where to take exposure. Passive or benchmarked strategies tend to be more of a price taker of duration. With rate hiking cycles coming to an end at different speeds, being fully flexible in this regard is key in capturing the potential upside in markets and avoiding the worst drawdowns.

Diversification

Given the richness of the fixed income asset class, opportunities can be found across the full market cycle. But, avoiding over-exposure to any single fixed income risk factor is the key to smoothing out volatility, particularly in turbulent markets.

Investing across the global fixed income spectrum with powerful diversified risk exposure helps create the greatest potential to achieve attractive, risk-adjusted returns. Managers who ensure structural diversification within the portfolios they manage, gain access to multiple sources of performance but also tend to produce risk adjusted fixed income returns with lower volatility than single-fixed income strategies.

AXA Global Strategic Bond Fund

An unconstrained actively managed global fixed income fund that aims to achieve attractive risk-adjusted fixed income returns with low volatility across a full market cycle.

The primary driver of returns for the AXA Global Strategic Bond Fund is top-down asset allocation across the fixed income capabilities of AXA IM. Analysis of the macroeconomic environment drives the asset allocation, and subsequent curve positions and sector allocation. On top of this we add bottom-up security selection, supported by our global team of fundamental credit research analysts. The flexibility of the strategy gives our team the opportunity to adapt the way they look at risk, while efficiently capturing value in the market.

Structural diversification in the strategy minimises volatility relative to any of the individual sources of risk from credit or rates. At the centre of this is our proprietary investment framework based around three “risk buckets” Defensive (government and inflation), Intermediate (investment grade credit and peripheral government), and Aggressive (high yield and emerging markets), which are central to portfolio construction.

Within each risk bucket we have wide and transparent investing leeway’s” 0-100% in Defensive, 0-60% in Intermediate and 0-60% in Aggressive. Although this is not a target, the application of investing leeway’s is an active management decision which ensures that we are not overly correlated to any single fixed income risk factor and offers access to multiple potential sources of performance while minimizing overall risk.

We also actively manage duration to take advantage of environments with fluctuating interest rates. With a leeway between 0-8 years, we are able to dynamically adjust the portfolio to determine how much duration risk we want to take, according to the macroeconomic environment. The fund typically has a lower duration position than traditional government bond or higher quality credit strategies which allows the investment team to allocate towards different sources of credit risk. The result is a fund which is diversified across a broad range of alpha sources.

Important information

All investment involves risk and capital is not guaranteed. The AXA Global Strategic Bond strategy invests in financial markets and uses techniques and instruments which are subject to sudden and significant variation, which may result in substantial gains or losses.

Capital at risk. The value of investments, and any income from them, can fall as well as rise and investors may not get back the amount originally invested.

Additional risks

- Counterparty Risk: failure by any counterparty to a transaction (e.g. derivatives) with the Fund to meet its obligations may adversely affect the value of the Fund. The Fund may receive assets from the counterparty to protect against any such adverse effect but there is a risk that the value of such assets at the time of the failure would be insufficient to cover the loss to the Fund.

- Derivatives: derivatives can be more volatile than the underlying asset and may result in greater fluctuations to the Fund's value. In the case of derivatives not traded on an exchange they may be subject to additional counterparty and liquidity risk.

- Interest Rate Risk: fluctuations in interest rates will change the value of bonds, impacting the value of the Fund. Generally, when interest rates rise, the value of the bonds fall and vice versa. The valuation of bonds will also change according to market perceptions of future movements in interest rates.

- Emerging Market Risks: emerging markets or less developed countries may face more political, economic or structural challenges than developed countries. As a result, investments in such countries may cause greater fluctuations in the Fund's value than investments in more developed countries.

- Liquidity Risk: some investments may trade infrequently and in small volumes. As a result, the fund manager may not be able to sell at a preferred time or volume or at a price close to the last quoted valuation. The fund manager may be forced to sell a number of such investments as a result of a large redemption of shares in the Fund. Depending on market conditions, this could lead to a significant drop in the Fund's value and in extreme circumstances lead the Fund to be unable to meet its redemptions.

- Credit Risk: the risk that an issuer of bonds will default on its obligations to pay income or repay capital, resulting in a decrease in Fund value. The value of a bond (and, subsequently, the Fund) is also affected by changes in market perceptions of the risk of future default. The risk of default for high yield bonds may be greater.

- Risks linked to investment in sovereign debt: Where bonds are issued by countries and governments (sovereign debt), the governmental entity that controls the repayment of sovereign debt may not be able or willing to repay the capital and/or interest when due in accordance with the terms of such debt. In the event of a default of the sovereign issuer, a Fund may suffer significant loss.

- High yield bonds risk: These bonds are issued by companies or governments with lower credit ratings and as such are at greater risk of default or rating downgrades than investment grade bonds.

The fund is also subject to geopolitical risk, securitised assets or CDO assets risk and contingent convertible bonds (“CoCos”).

Further explanation of the risks associated with an investment in this strategy can be found in the prospectus.

Disclaimer

Not for Retail distribution: This document is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This marketing communication does not constitute on the part of AXA Investment Managers a solicitation or investment, legal or tax advice. This material does not contain sufficient information to support an investment decision.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Before making an investment, investors should read the relevant Prospectus and the Key Investor Information Document / scheme documents, which provide full product details including investment charges and risks. The information contained herein is not a substitute for those documents or for professional external advice.

The products or strategies discussed in this document may not be registered nor available in your jurisdiction. Please check the countries of registration with the asset manager, or on the web site https://www.axa-im.com/en/registration-map, where a fund registration map is available. Please note that the management company reserves the right, at any time, to no longer market the product(s) mentioned in this communication in the European Union country by notification to its authority of supervision in accordance with European passport rules. In particular units of the funds may not be offered, sold or delivered to U.S. Persons within the meaning of Regulation S of the U.S. Securities Act of 1933. The tax treatment relating to the holding, acquisition or disposal of shares or units in the fund depends on each investor’s tax status or treatment and may be subject to change. Any potential investor is strongly encouraged to seek advice from its own tax advisors. In the event of dissatisfaction with the products or services, you have the right to make a complaint either with the marketer or directly with the management company (more information on our complaints policy is available in English https://www.axa-im.com/important-information/comments-and-complaints). You also have the right to take legal or extra-judicial action at any time if you reside in one of the countries of the European Union. The European online dispute resolution platform allows you to enter a complaint form (https://ec.europa.eu/consumers/odr/main/index.cfm?event=main.home.chooseLanguage) and informs you, depending on your jurisdiction, about your means of redress (https://ec.europa.eu/consumers/odr/main/?event=main.adr.show2).

Past performance is not a guide to current or future performance, and any performance or return data displayed does not take into account commissions and costs incurred when issuing or redeeming units. References to league tables and awards are not an indicator of future performance or places in league tables or awards and should not be construed as an endorsement of any AXA IM company or their products or services. Please refer to the websites of the sponsors/issuers for information regarding the criteria on which the awards/ratings are based. The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested. Exchange-rate fluctuations may also affect the value of their investment. Due to this and the initial charge that is usually made, an investment is not usually suitable as a short term holding.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ. In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

Risk warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.