Why should investors consider sustainability in CDI?

KEY POINTS

Whilst institutional investors may have a sustainability approach for their core fixed income portfolio, reflecting it within a cashflow driven investment strategy (CDI) is still a growing concept. CDI strategies are designed to provide a regular income stream from bond coupons and maturities to help address a pension fund’s income requirements. Given their long-term nature and broad fixed income allocation, they are well placed to reflect outcomes beyond that of income requirements.

This is where sustainability can come in. Sustainability aims to generate long-term financial returns while contributing positively to society and the environment. A sustainable approach to investments should help to mitigate risks associated with environmental degradation and social issues.

Of course, it isn’t just about environmental, social, and government factors; sustainability also emphasises long-term considerations such as carbon intensity reduction or the contribution towards net zero.

We believe there are three key reasons why institutional investors should consider sustainability for their CDI strategies.

- Strategic importance - CDI strategies often make up a large proportion of client portfolios and are a long-term, strategic allocation. Therefore, the impact of any sustainability risks, and the impact from becoming more sustainable, are higher. The time horizon over which many sustainability themes are expected to emerge are closely aligned to the maturity of CDI strategies.

- Risk mitigation - The primary purpose of a CDI strategy is to reduce risk – whether that be sequencing, re-investment, or growth risk in portfolios. This means that any risk factor which could impair the ability of the portfolio to pay its bond cashflows, including Environmental, Social, and Governance factors, should be considered throughout in the investment process.

- Ability to act – Liquid fixed income, the primary asset class in CDI strategies, is one of the easiest asset classes to integrate sustainability considerations into. This is thanks to the large investible universe, range of instruments available, and the naturally maturing nature of the asset class. If funds want to improve their sustainability credentials, then a CDI portfolio is possibly one of the best places to start.

How can CDI portfolios integrate sustainability to meet financial and non-financial goals?

There are five methods through which sustainability can be integrated within CDI portfolios. These methods are over and above traditional ‘ESG assessment integration’ which are standard and part of the day-to-day financial management of portfolios. These five methods can be targeting individually but are most often used in combination to achieve the most impacted financial and non-financial impact.

- Decarbonisation – The most common objective for our client base is seeking to reduce the carbon emissions of their CDI portfolio, often aligned with wider portfolio-level objectives. This can be through explicit decarbonisation objectives e.g. a 50% reduction in emissions by 2030, or a softer target that seeks to reduce emissions to Net Zero by 2050.

- Net Zero Alignment – While global decarbonisation is often the end goal, investors often choose to focus on portfolio-level alignment. This is a forward-looking approach to climate change rather than one looking at historical emission.

- Green, social and sustainability bonds (GSS) – As part of the drive to achieve Net Zero, the world needs to invest in issuers that create the products and services that allow companies to decarbonise. Within fixed income, this is primarily through the issuance of green and sustainability bonds. These bonds can play an important role in improving the portfolio’s sustainability profile and provide a positive net impact.

- Engagement – Fixed income investors have a huge power to engage thanks to the large universe size and the ability to interact with issuers not available to other asset classes e.g. governments/quasi-governments, private companies and the regular new issuance cycle giving a natural point of engagement, particularly for GSS.

- Exclusions – Many, although not all, clients have historically started their sustainability journey by looking at exclusions. This could be to mitigate the potential risk of unsustainable investments on portfolio performance (single-materiality), or to exclude issuers that have a large negative impact on the wider world either environmentally or socially.

With each of the above methods, we work closely with our clients to ensure that any sustainability integration strikes the right balance of achieving the financial objectives of the portfolio while improving the sustainability footprint.

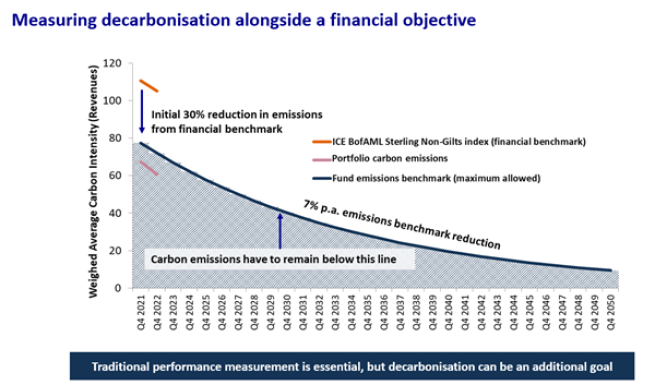

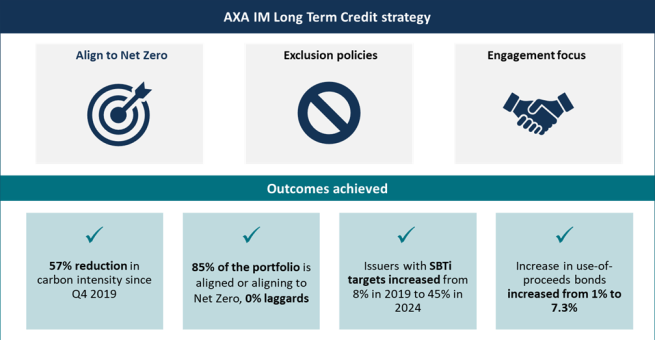

Outcomes are the objective

While a lot of attention is focussed on having the right framework, tools and talent to implement sustainability, we are equally focussed on delivering the outcomes clients are seeking through their sustainability objectives. The diagram below shows the client-specific goals and outcomes achieved since 2021 for a live CDI portfolio, all while maintaining the cashflows, duration, rating and spread-level in-line with the clients’ objectives.

Thanks to improving data on ESG and Engagement, the impact of that sustainability approach can also be assessed. We have market-leading reporting which allows asset owners to monitor our success through the below factors:

- a clear overview of the portfolio’s ESG integration,

- carbon emissions and decarbonisation evolution

- Net Zero alignment through a range of metrics

- Engagement breakdowns and case studies

By aligning CDI portfolios with long-term sustainability goals and mitigating ESG-related risks, institutional investors should be able to safeguard against future liabilities and tap into the growing market for green investments. As the landscape continues to evolve, those who embrace sustainability within their CDI strategies should be able to create a strategy that seeks financial targets while also providing a positive impact on society and the environment.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.