Climate change: why insurers should consider their fixed income portfolios now

- 19 March 2021 (5 min read)

Insurance companies are operating in a “lower for longer” interest rate environment, where yield is hard to come by, and at a time when accounting and regulatory frameworks are shaping investment decisions. Climate change has risen rapidly up the agenda as a mounting awareness of climate-related risks accompanies a sharpened regulatory focus.

We believe climate-aware investing can be an opportunity for insurers to mitigate against an emerging and significant risk factor. This is essential for investors targeting predictability of cashflows alongside high resilience to market risks.

Highlights:

- Fixed income returns and climate resilience are two of the most prominent investment themes for UK insurers

- Climate-aware fixed income investing aims to mitigate against the current and future, physical and transition risks of climate change as well as aligning portfolios to the 2015 Paris Agreement

- Managing climate-related risks could increase predictability of income from asset cashflows, and potentially prevent downgrades and defaults from climate-related exposures

What are ‘climate-aware’ portfolios?

Insurers are rightly questioning how each component of their investment strategy will be impacted by climate change as part of their overall approach to managing climate-related financial risks across the firm. Climate-aware investing aims to:

- Mitigate the risks to investment portfolios from a range of temperature scenarios

- Help limit the global temperature rise to 1.5-2.0°C above pre-industrial levels by 2100 – investors can target this through aiming for zero greenhouse gas emissions by 2050 (‘Net Zero’)

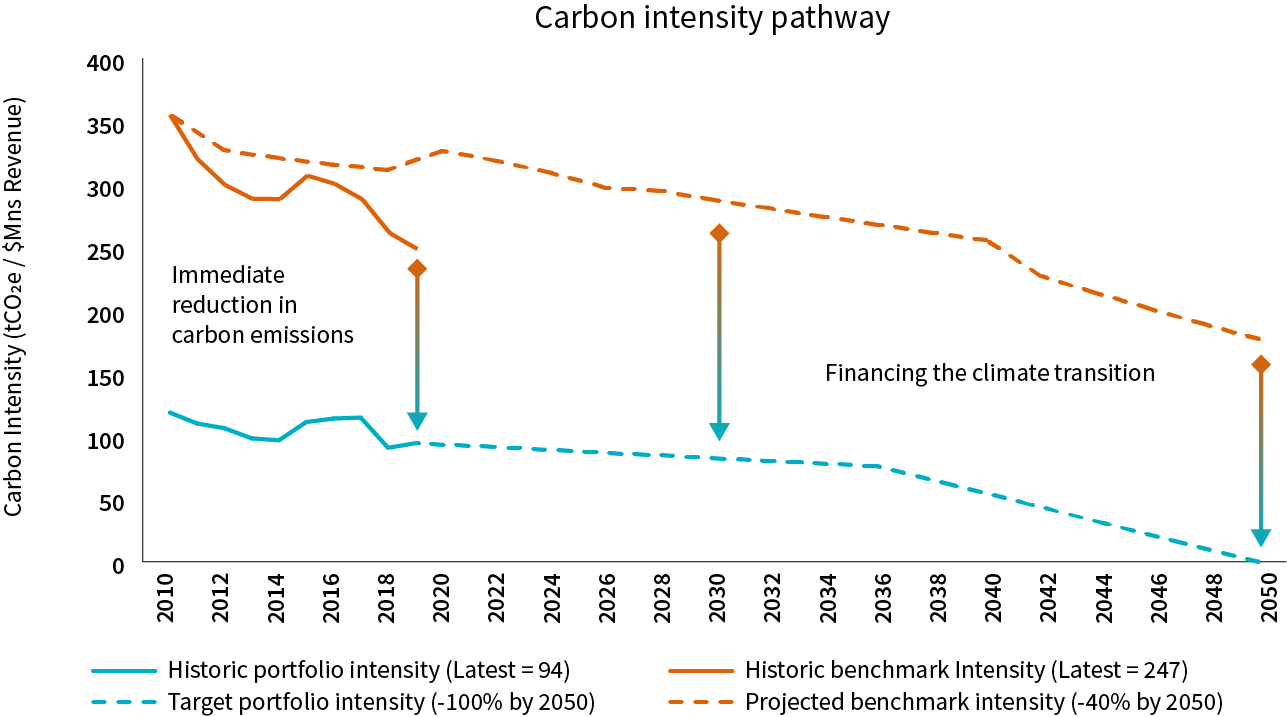

Climate-aware portfolios will typically have explicit climate objectives, such as reducing carbon emissions by 50% by 2030 and 100% by 2050, in line with the Institutional Investors Group on Climate Change (IIGCC) framework.

We believe there are two types of issuers that can help achieve these objectives:

- Issuers that currently have low greenhouse gas (GHG) emissions and/or positively contribute to climate change mitigation

- Issuers that may have a high current level of emissions but have a robust and credible future decarbonisation plan. These companies are crucial to the impact goal of targeting net zero emissions by 2050.

Figure 1: Reducing emissions – the task ahead for companies and investors

Source: AXA IM. For illustrative purposes only

Climate-aware portfolios will also typically have explicit climate objectives, such as reducing carbon emissions by 50% by 2030 and 100% by 2050, in line with the Institutional Investors Group on Climate Change (IIGCC) framework.

It is important to note that climate-aware investing should help, and not hinder, the overarching financial objective of insurers, which is to pay their policy holders and make a positive return on capital.

What are the risks of climate change on credit portfolios?

Climate-related risks are of uncertain magnitude, irreversible and uneven. They present in two main forms:

- Physical risks relate to the impact of climatic events if temperatures continue to rise. They might include extreme weather, such as a flood causing supply chain issues, or more chronic risks such as higher disaster insurance costs for companies

- Transition risks arise from the shift to a low carbon world and include the abrupt introduction of regulation, shifts in consumer demand, technological changes and investor sentiment. For example, the ban on sale of petrol and diesel cars in the UK from 2030

These risks could materially impact an issuer’s balance sheet and access to capital markets, both of which are key inputs in credit ratings and risk analysis. It is also clear that there is enormous investor, political and regulatory momentum in climate-aware investing. This momentum alone, irrespective of how the physical risks will impact asset prices, justifies the integration of climate risk into our analysis due to the material financial impact it could have on credit portfolios.

While some energy companies have drawn intense investor pressure over what have been seen as underwhelming emissions targets, we do not see at present that a ‘winners and losers’ story in the climate transition is impacting spreads in the credit space. This is perhaps due to the current extraordinary global monetary stimulus, or due to the risks being underestimated by investors. However, the cost of borrowing for climate laggards could start to rise as investors fully appreciate the risks that climate change poses and shift to climate-aware strategies.

We have experienced changing investor appetite impact sectors historically. The tobacco sector, for example, which a large proportion of investors, including AXA IM, have excluded from their portfolios, has underperformed the wider index by 5% over the last five years, as the chart below shows.

Figure 2: Falling out of favour – the tobacco discount

Source: BoAML, US Investment Grade Tobacco Sector (USTO) versus the US Corporate Index (C0A0), 04/01/2016 to 04/01/2021. For illustrative purposes only.

Further, the cost of issuing debt for US tobacco companies has changed from being 50 basis points (0.5%) cheaper than the overall corporate market in 2016 to now being 50 basis points more expensive. In the context of the current low yield environment this is an enormous change in the funding costs for these companies.

We expect the transition to the low-carbon economy to be of greater magnitude and across a larger proportion of the market and so will have a much larger impact on portfolio returns.

It will be no surprise to hear that, from the end of 2021, UK insurers will be required by the Prudential Regulatory Authority (PRA) to embed an approach to managing climate related financial risks following previous consultation1 . We have already seen several large insurers and other asset owners publish and start to implement their own climate strategies. We could see being a ‘first-mover’ in the climate transition as the difference in being able to execute fully and more cost-efficiently.

How can a climate-aware, credit portfolio mitigate against these risks?

Climate-aware investing in credit portfolios means being aware of and mitigating this emerging material risk factor, as well as targeting alignment to the 2015 Paris Agreement and fulfilling regulatory obligations. This is a magnified version of the shift in attention and assets towards environmental, social and governance (ESG) investing, both in terms of scale and importance.

We view both ESG and climate-investing as a method to protect portfolios against ‘tail’ risks such as climate change or controversies while the fundamental ESG research undertaken by our credit analysts builds another layer of risk mitigation. Avoiding tail risks is one of the most important characteristics of a credit portfolio.

When looking at credit portfolios, we aim to improve the predictability of income and ultimately create resilience to market shocks in a range of market and temperature scenarios. One way to measure this resilience is by undertaking scenario analysis using climate value at risk, which measures the potential impact to a portfolio in different temperature scenarios.

Figure 3: Measuring the risk – breaking down the climate impact

Source: AXA IM. For illustrative purposes only.

We believe it is important to first reduce the magnitude of the impact of climate change compared to a traditional universe and second, to ensure that the impact on portfolios in either a ‘hot’ or a ‘cool’ scenario are not dramatically different, for the purpose of minimising the range of potential outcomes.

We must also consider how the bonds selected align with the maturity of the portfolio and fulfil the requirement to both finance climate solutions and positively allocate to rapidly decarbonising issuers. We discuss this aspect more in our next paper which focusses on the role of long term credit as an annuity backing asset, and the importance of integrated climate awareness in the approach.

Complementing existing insurer objectives

Implementing a climate-aware strategy should not mean only investing in bonds with the lowest ‘temperature’ or lowest carbon emissions, irrespective of their price. On the contrary, we wholeheartedly support creating a climate strategy that complements your existing objectives in terms of portfolio-level risk and return characteristics. Climate-aware investing should help mitigate against the risks of a range of temperature scenarios while protecting the world in which your policy holders and other stakeholders live in.

Integrating climate considerations into the investment process does not need to come at the expense of reduced returns - the world is moving towards a lower carbon economy and future technological advancements and regulatory developments will require insurers to significantly progress this over time. The transition presents an opportunity for insurers to mitigate against emerging risks and enhance sustainable profitability in the future.

Insurers who integrate climate objectives alongside – not in isolation to – other financial objectives should be able to successfully achieve both their climate and long-term return goals.

- RGVhciBDRU8gU2FtIFdvb2RzIFBSQSBsZXR0ZXIg

Cashflow Driven Investing

Cashflow driven investing is changing the defined benefit pensions investment landscape

Explore nowVisit the fund centre

The aim of the Fund is to provide an income and capital return (net of fees) in line with the market for sterling denominated, investment grade bonds issued by companies over the long-term while maintaining a low turnover of bonds held by the Fund.

View fundsThe Sub-Fund seeks both income and growth of your investment, in EUR, and a sustainable investment objective, from an actively managed bond portfolio, in line with a socially responsible investment (SRI) approach.

View fundsThe Sub-Fund seeks to achieve a mix of income and capital growth measured in USD by investing mainly in investment grade corporate debt securities from issuers located worldwide, over a medium term period.

View fundsNot for Retail distribution

This document is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This promotional communication does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee that forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Before making an investment, investors should read the relevant Prospectus and the Key Investor Information Document / scheme documents, which provide full product details including investment charges and risks. The information contained herein is not a substitute for those documents or for professional external advice.

The products or strategies discussed in this document may not be registered nor available in your jurisdiction. Please check the countries of registration with the asset manager, or on the web site https://www.axa-im.com/en/registration-map, where a fund registration map is available. In particular units of the funds may not be offered, sold or delivered to U.S. Persons within the meaning of Regulation S of the U.S. Securities Act of 1933. The tax treatment relating to the holding, acquisition or disposal of shares or units in the fund depends on each investor’s tax status or treatment and may be subject to change. Any potential investor is strongly encouraged to seek advice from its own tax advisors.

Past performance is not a guide to current or future performance, and any performance or return data displayed does not take into account commissions and costs incurred when issuing or redeeming units. The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested. Exchange-rate fluctuations may also affect the value of their investment. Due to this and the initial charge that is usually made, an investment is not usually suitable as a short term holding.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.