Multi-Asset Investments Views: We can work it out

KEY POINTS

US exceptionalism is back - US equities continued to move higher and outpaced other major markets in July. This stemmed from a supportive market backdrop and a remarkably resilient US economy. Markets seem to have grown somewhat immune to trade risks, banking on incremental deal-making even amid the tough rhetoric. US corporate earnings have been strong overall, which has helped further boost investor confidence.

In contrast, Europe’s earnings season started on a more mixed note. Despite heightened trade tensions and tariff increases under President Donald Trump’s administration, the expected damage to corporate earnings has yet to materialise.

Trade policy uncertainty has eased since Trump’s ‘Liberation Day’ tariff announcement on 2 April, but increased again in July1 as the President ramped up pressure on major trading partners to secure favourable deals before the 1 August deadline.

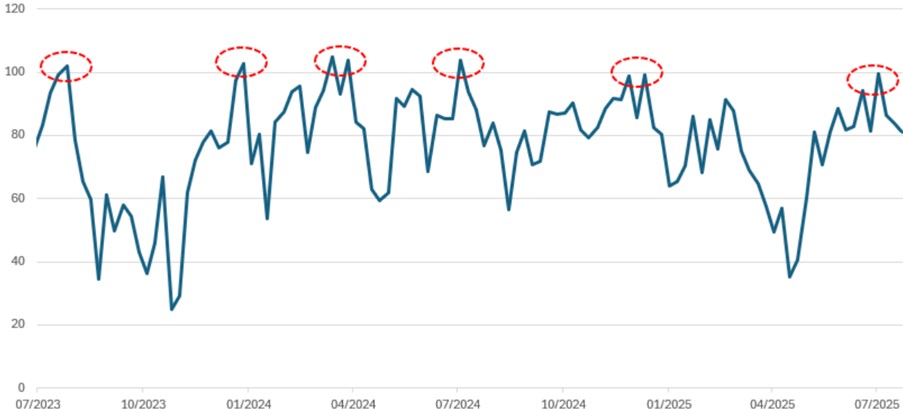

Unlike previous episodes of rising uncertainty which had triggered market sell-offs, US equities remained strong, with both the S&P 500 and Nasdaq indices reaching new highs in July - though this, in turn, raised investor complacency concerns. Late July brought relief as Japan and Europe both sealed trade deals with the US, with tariffs set at 15% - a considerable hike but significantly lower than the previously threatened rates ranging between 25% and 50%. Equities wasted no time in celebrating; US stock indices rallied to fresh highs further driving sentiment indicators to levels of extreme optimism (see chart below).

Bullish or complacent? US investors are back to high equity exposure

Source: US National Association of Active Investment Managers (NAAIM), Bloomberg, AXA IM, as of 28 July 2025. The NAAIM Exposure Index measures active investment managers’ average exposure to US equity markets.

- As measured for example by the Bloomberg Economics Trade Policy Uncertainty Index

Digging beneath the surface could however question the durability of this optimism. The new trade deals, while less draconian than feared, still represent a substantive increase in the effective tariff rate. Tariffs on the automobile sector in Japan and Europe dropped from a potential 25%-plus to 15%, in return for a commitment to significant spending plans in the US. Still, the real-world impact of punitive tariff rates applied to imports from key trading partners remains a significant headwind for trade and global corporate margins.

While the market’s initial reaction was relief, it may be more a case of investors clinging to the lesser of two evils, rather than any genuine improvement in trade fundamentals. Overall, we keep risk levels contained in our portfolios, given that market optimism has reached levels typically associated with potential consolidation, and positioning data now shows more balanced investor exposure.

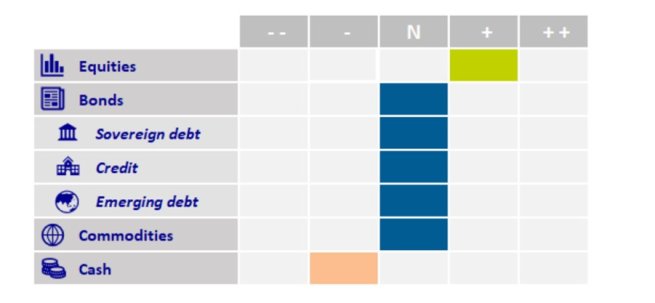

Within our unchanged modestly bullish stance, we favour US technology companies over US small caps, as the former continue to exhibit superior earnings quality. In Europe, we prefer small- and medium-caps, which are less exposed to the negative effects of euro strength. German mid-caps are particularly attractive, as Germany's private sector appears ready to complement public spending in efforts to revive the country's competitiveness.

In fixed income, recent weeks have seen a marked reconstitution of the term premium across major bond markets, with the long end of sovereign yield curves rising. This dynamic has been the most apparent in Japan, where upward pressure on long-term yields has been signalling a complete reshaping of market expectations.

Rising term premiums reflect the need for governments to compensate investors for holding increased long-term debt issued to finance growing deficits. Policy uncertainty, geopolitical instability, and diminished central bank intervention have compounded this effect, making long-term rates more susceptible to market dynamics.

Somewhat counterintuitively, these moves in term premia are unfolding even as inflation expectations remain anchored. Break-evens have shown little sign of de-anchoring despite fiscal largesse and high effective tariff rates, suggesting market participants still trust central bank credibility and the transitory nature of current price pressures. After this upward move in interest rates, our portfolios are back to a broadly neutral interest-rate sensitivity, with a preference for the short-end of the yield curve.

Meanwhile, the market consensus is decidedly bearish on the US dollar, anticipating further weakening versus the euro and other major currencies. We concur and continue to favour a bearish stance on the dollar over the medium term, and see any short-term dollar rebound as an opportunity to reinforce our positioning. First, the pace of US economic growth relative to other large economies appears to be decelerating. Second, political uncertainty and growing scepticism regarding Washington’s policy direction should continue to weigh on investors’ confidence in the greenback. Although in the short term we believe the market is overestimating the number of interest rate cuts, the Federal Reserve is likely to reduce rates over the medium term.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ.

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

© 2025 AXA Investment Managers. All rights reserved

Image source: Getty Images

Risk warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.