Multi-Asset Investments Views: It’s a mad world

KEY POINTS

President Donald Trump triumphantly branded 2 April ‘Liberation Day’, as he announced a wave of new tariffs but the occasion was anything but liberating for financial markets. What was meant to be a bold assertion of economic sovereignty quickly revealed itself as a high-stakes gamble with global consequences.

The US administration’s sweeping, across-the-board tariffs - applied indiscriminately to virtually every trading partner, from strategic allies to islands with more penguins than people - were implemented through a simplistic flat-rate formula and landed not as strategy, but as shock therapy.

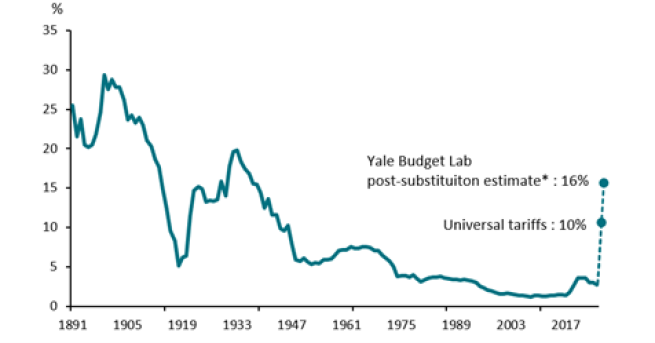

The effective US tariff rate on imports, after substitution effect could now be close to 16%, the highest level since 1934 (see chart). The White House justified the move as a necessary treatment to wrestle control of trade policy and industrial competitiveness back from global markets. But investors saw something else entirely: a destabilising policy misfire that ignored the complexity of global supply chains and threatened to derail an already fragile economic equilibrium.

Just on the basis of historic import weights, the US tariff rate is 25.6% - its highest since 1901. In reality, US consumers are expected to adjust spending behaviour to reduce reliance on newly expensive imports, a substitution effect that will reduce the effective tariff rate to 16%, according to Yale Budget Lab estimates.

Equities responded immediately and sharply, with global markets shedding trillions in value in a matter of days. US Treasuries, typically perceived as a haven in such moments, offered only limited relief as yields spiked in response to the inflationary implications of the tariffs. The White House’s decision to partially pause implementation - granting a 90-day reprieve for all countries except China - was taken by markets to be an implicit admission that the impact had been misjudged. But by then, investors’ psychology had shifted: the dominant force driving markets was no longer a balance of growth, inflation, and earnings, but the unpredictability of presidential decision-making.

Trump himself has been remarkably candid about his belief that economic hardship in the near term is not only acceptable but perhaps necessary. In his view, this would be the price of reasserting American leverage in global trade. In our view, he even sounds willing to tolerate market stress as part of that strategy. While the theoretical costs of tariffs are well-understood — higher consumer prices, weaker corporate margins, dampened investment — the true question now is one of degree. Will this policy deliver a transitory slowdown? Or will it pull the US into an outright recession? AXA IM macroeconomists believe it's a close call.

At the same time, the credibility of the Federal Reserve (Fed) is being tested. Trump’s repeated public attacks on Chair Jerome Powell, coupled with open demands for immediate interest rate cuts, have revived concerns about the Fed’s independence. At one point, Trump appeared to seriously consider removing Powell from his position, only to later dismiss the idea.

Still, the damage to perception has been done. When investors begin to question whether central bank policy is being steered by political expedience rather than macroeconomic reality, the very notion of Treasuries as a risk-free asset is eroded. This breakdown in confidence has accelerated a striking rotation in global portfolios.

Gold has soared to new highs this year, as both institutional and retail investors seek protection not just from inflation but from broader policy dysfunction. Flows into gold exchange-traded funds have accelerated sharply, while central banks — particularly in Asia — have been steadily building reserves, further reinforcing the sense that trust in dollar-denominated assets is no longer absolute.

Meanwhile, the equity market remains vulnerable. Even after recent declines, valuations have not adjusted sufficiently to reflect the new macroeconomic environment. The S&P 500 is currently trading at nearly 20 times 12-month-forward earnings, a level more typical of expansionary conditions than of an economic slowdown.

Consumer spending, the backbone of recent GDP growth, is losing momentum. Corporate capital expenditure is now declining outright, with several high-profile company chief executives citing policy uncertainty as a reason for shelving investment plans. The three pillars that had been supporting headline growth — government stimulus, services spending, and technology-led capex — are all showing signs of slowdown.

Among the hardest hit are US small-cap stocks. These companies tend to be more reliant on domestic growth, more exposed to rate-sensitive debt, and more vulnerable to cyclical slowdowns. The optimism that Trump’s domestic-first policy initially induced has now collapsed under the weight of rising interest rates and policy-driven uncertainty. Tariff-induced inflationary pressure, combined with persistent political interference, has pushed yields on longer-dated bonds higher. This is an additional hurdle for smaller firms, which generally have higher borrowing costs and fewer financing options. With the Fed boxed in between a weakening economy and inflationary pressures, policy options are narrowing.

The now underway corporate earnings season may offer a temporary reprieve — but only selectively. Financials could benefit from heightened volatility and elevated trading revenues. Some consumer goods companies may see front-loaded sales as buyers try to get ahead of potential tariff hikes. Still, beneath the surface, earnings revisions are moving lower, guidance is turning cautious, and corporate management teams are pulling back on forward visibility.

With valuations still elevated, political risk dominating headlines, and institutional confidence under strain, we remain cautious overall. In our view, the main risk is not that markets are mispricing recession but that they have not fully priced the structural instability now baked into policy itself.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ.

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

© 2025 AXA Investment Managers. All rights reserved

Image source: Getty Images

Risk warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.