Unconstrained fixed income: Harnessing the diversity of the universe

As an asset class, fixed income goes well beyond the notions of low risk and low return. Today’s global fixed income universe comprises a broad spectrum of sub-classes with the potential to deliver outcomes ranging from capital preservation to income and capital growth. An unconstrained approach can aim to access this range of opportunities, rather than being limited to a particular area of the universe.

In our view, most investors look to unconstrained fixed income strategies to deliver attractive risk-adjusted returns through the market cycle. We believe the key to achieving this is actively managing a portfolio of different types of risk factors. In managing our Global Strategic Bonds strategy, our focus is on constructing a portfolio which is structurally diversified, holds liquid fixed income assets and applies careful risk budgeting.

Maintaining an appropriate balance

Risk management is an integral part of our asset allocation approach. We aim to manage the portfolio in a volatility-controlled way because we think that most investors are not looking for their bond allocation to be the most aggressive segment of their total portfolio.

However, that is not to say it is not a high conviction strategy. We strongly believe we can create potentially attractive returns by using our flexibility to be opportunity-driven and selective, rather than being tied to a specific benchmark. We place a great deal of emphasis on implementing active strategies that are conviction-driven and designed to weather short-term noise, rather than trying to aggressively time markets.

We know the economic cycle is in constant motion and different asset types will perform better or worse at different points. This does not make asset allocation as easy as it sounds. Firstly, we need to be able to identify where we are in the cycle to get ahead of the market and obtain the right assets at the right price. Secondly, hugely unpredictable market events can happen at any time.

Managing an unconstrained strategy through a changing market environment is not about predicting the unpredictable. Rather, it is about positioning for the right, long-term reasons based on observable facts - and having the agility to respond as markets move.

Simplicity and transparency

Unconstrained fixed income is a broad concept, and strategies can vary in complexity and objectives. Some areas of today’s fixed income universe are more complicated and exotic than traditional bonds. While they can offer compelling yields and perform well in risk-on phases, being overly concentrated in these areas may expose investors to more risk than they anticipate.

So, investors should always know what’s ‘under the bonnet’ of any strategy they choose. We prefer simplicity and transparency to mitigate negative surprises. This reflects our central philosophy that investors do not want their core fixed income portfolio to be too aggressive, but rather prefer to aim for optimised total returns while avoiding the worst of the lows through the cycle.

We think of our strategy as something of a ‘best ideas’ portfolio. We rely on the engines of expertise we have around the world in terms of our extensive global fixed income resources, to generate ideas across the fixed income spectrum and then apply a proprietary framework which allows us to filter than spectrum in a different way.

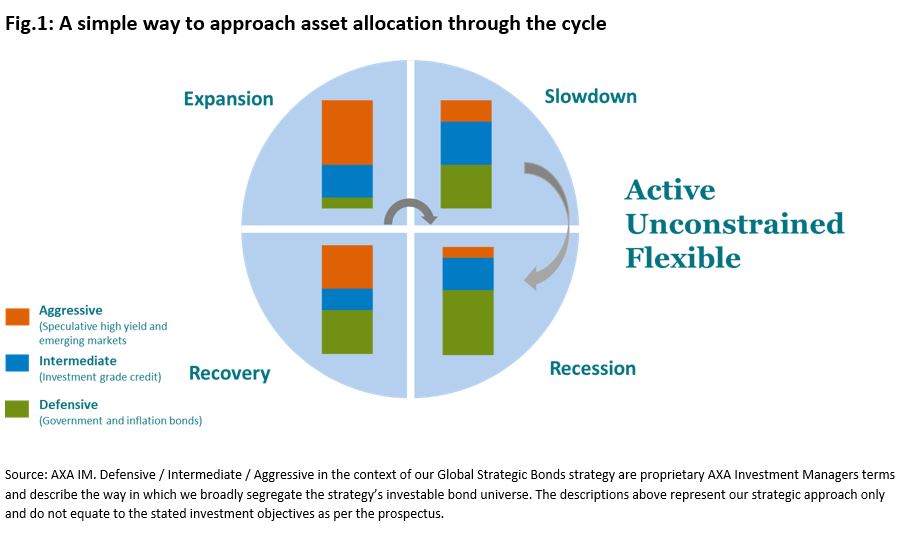

This framework breaks down the universe into three categories of sub-asset types and allocates between them, taking account of prevailing economic and market conditions and valuations.

The first category is Defensive. Defensive assets would be the highest rated, most liquid, purely interest rate-sensitive assets - so, mainstream government bonds.

The next category is Intermediate assets. These are high-quality, investment grade credit. Qualitatively, we would include peripheral European government bonds, as there is currently credit spread in those assets.

Lastly, Aggressive assets. These are what we consider somewhat equity-like. They are high yield and emerging markets (whether it is government bonds, investment grade or high yield). For simplicity’s sake, we define aggressive assets as those that have the most credit risk or default risk.

Above all, we are confident that the structural diversification in the strategy minimises volatility relative to any of the individual sources of risk from credit or rates. Our framework relies on understanding correlations between different fixed income assets, duration and credit ratings, as well as the notion of negative correlation between pure rate risk (duration) and pure credit risk (excess return). The skill of our investment team is understanding how to balance our positioning tactically across this very broad spectrum, throughout the market cycle.

Not for Retail distribution

This document is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document. Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ. In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

Risk warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.