Themes in focus for Global Strategic Bonds

Key points:

- Having a flexible duration management approach has been key in these volatile markets

- Investment grade credit looks like the sweet spot following 2022’s repricing

- Picking the winners and losers in the high yield market

Many of the issues that have dominated the headlines for most of this year are still at large on the macro stage: central bank monetary policy, inflation and the energy crisis. However, within the fixed income market, there are now some positive signals emerging which are drawing the attention of bond investors keen on locking in a bargain.

High yield bonds are issued by companies with a relatively low credit rating, which may not have been able to access capital markets in the past. The asset class offers investors a higher risk, higher return opportunity than more traditional fixed income markets.

Here we look across the three risk buckets, Defensive, Intermediate and Aggressive1, that break down the fixed income universe for the Global Strategic Bonds strategy and discuss the themes that we are currently focussing on.

Defensive: Duration management

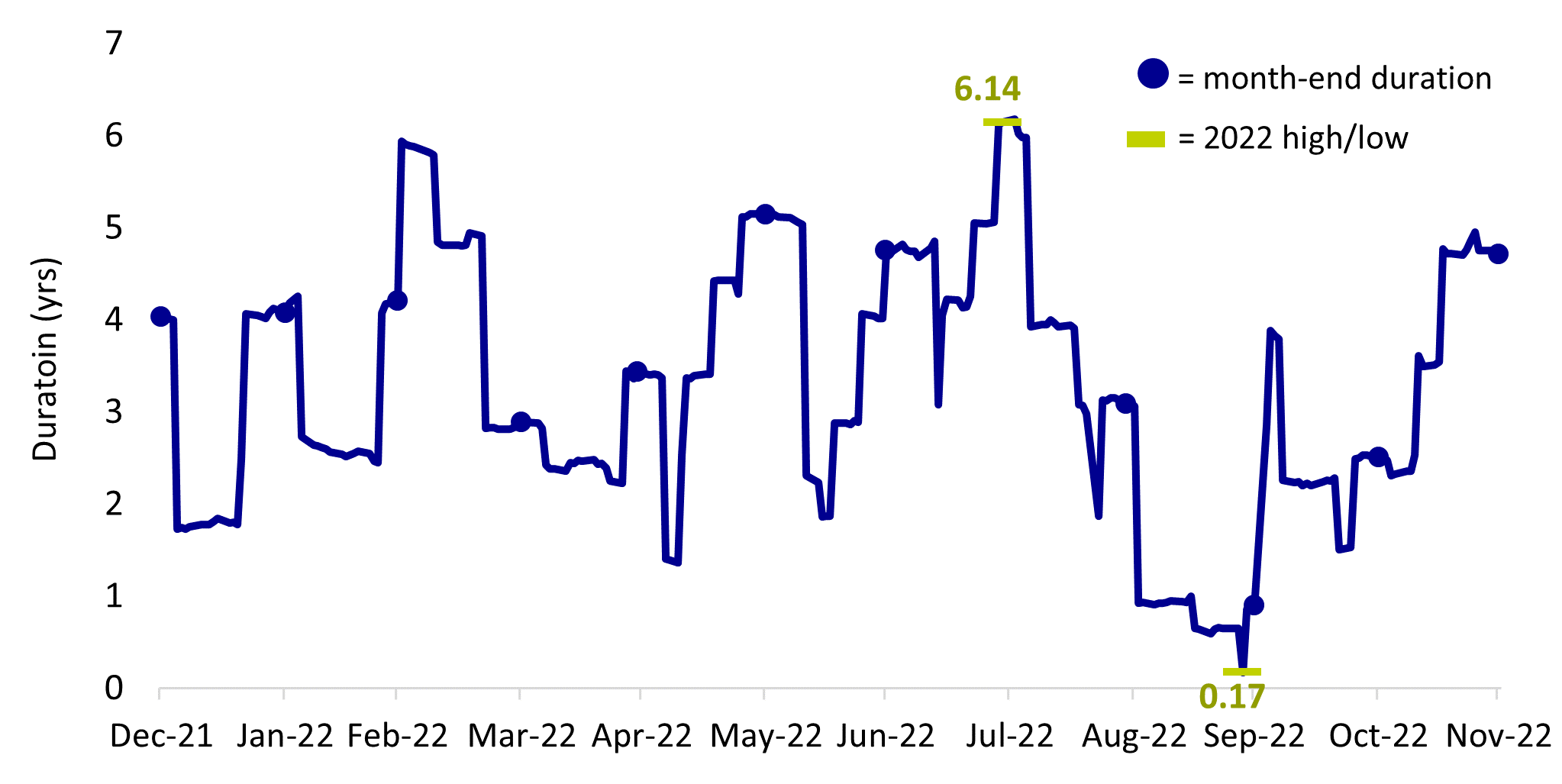

We view Defensive bonds as those where performance is predominantly driven by interest rate movements. Our flexible approach allows us to adjust our duration according to our tactical views and the point in the economic cycle. The rates environment has been volatile this year, with the global government bond market at the epicentre of the sell-off, driven by inflation which has proved to be stickier than many expected and central banks which were too slow to tighten financial conditions.

In the second half of the year, our duration management has worked much better than the first half, when we tried to add exposure on a couple of occasions, only for yields to head higher once more. We extended duration in July, capturing a bond rally driven by short-lived speculation that the Fed might slow the pace of interest rate hikes or pause entirely. We then cut our exposure in August and September following renewed focus by central banks on tackling inflation at all costs. To reflect this bearish view, the strategy began September with a duration close to zero years.

The strategy is long only with an overall duration leeway of 0-8 years, but we can implement negative duration strategies on the curve or on a cross-currency basis when we feel it’s appropriate. We came into the period of heightened UK volatility in late September with a slight negative GBP duration position. This was based on our view that UK gilts could underperform given double digit CPI prints that showed no signs of easing, and a new government with a fiscal policy agenda that seemed at odds with the Bank of England’s mantra to tighten financial conditions to fight inflation. This position helped to protect the strategy during the very negative market reaction to the UK government’s “mini-budget”. Upon the Bank of England’s intervention to support long-dated gilts, however, we added back to GBP duration, which worked well as gilts subsequently rallied back.

As the chart below shows, the ability to manage duration in a flexible way saw the strategy’s duration go from its highest to lowest exposure in a matter of weeks:

Daily duration management: 2022 YTD

Source: AXA IM as at 11/11/2022.

We sit today2 with a more bullish duration position following the first signs in early November that headline CPI in the US might be easing. We prefer US treasuries and expect the curve to steepen after many months of flat and inverted yield curves, with short-end valuations now pricing in a lot in terms of the Fed’s terminal rate.

Intermediate: Adding investment grade opportunities

Investment grade credit has been hit on both sides in 2022 by higher government bond yields and wider credit spreads. On a forward-looking basis, however, the asset class now looks attractive in terms of risk-reward opportunities: the combination of government bond duration risk and high-quality credit risk offers investors a yield of anything between 5% and 8%. Put another way: equity-like returns with fixed income risk. This stands in stark contrast to many years in which investors have been bereft of yield – turning to lower rated credit or even more illiquid asset classes instead.

The bulk of our 30% Intermediate bucket exposure is in sterling and euro credit (21%), which now price in a lot – both in terms of yield and spread. In October, a basket of A-rated sterling credit yielded close to 7% and euro credit above 4% – higher than anything seen in the last ten years.3 BBBs look particularly attractive to us on a spread basis, given the greater underlying credit risk, with 25% of our overall credit exposure invested in BBBs. We do also hold US credit exposure (10%), although do not think spreads in the US currently fully compensate for potential recession risk, considering how resilient the US economy remains for now.

Within the investment grade space, we like banks and insurance companies, which offer a yield premium for subordinated debt or bonds which have some sort of optionality over the call date, compared with simple bullet maturities from the same entity. This is because bank and insurance bonds that are issued below senior level will have call structures and be treated differently by the market, regulator and rating agencies depending on evolving capital requirement.

Naturally as bond investors we are focused on yield and spread, but the other aspect worth bearing in mind is the potential for significant capital appreciation, given how much bond prices have fallen this year. The average price on a Global Corporate Index – composed of investment grade credit – recently fell to 85 for the first time this millennium.4 Although default rates are set to pick up, there are plenty of good quality single name opportunities that offer a significant “pull-to-par” benefit as they approach maturity – making short duration credit an attractive place to invest.

Aggressive: Benefitting from dispersion in high yield

Our largest allocation in what we describe as “equity-like” fixed income is US high yield, where we see great value. The broad US High Yield Index currently yields around 9%.5 Clearly, it’s a fixed income asset class, but with much higher default risk and most of its yield derived from credit spread, rather than rates. Hence its returns correlate more with equities than the government bond market.

That said, this is not a market in which we think “passive investing” wins. We see a real mix of opportunities in the current market given the growing dispersion, making the ability to ignore whole sectors or single names key to driving outperformance versus the market. For example, we are currently avoiding segments of the retail sector, most notably department stores, due to pressure on the consumer that should come through in the higher rates regime.

The other theme within our US high yield exposure is the ability to overweight lower rated (Bs and CCCs) smaller issue sizes compared to the broader market. Nearly a third of our US high yield allocation is in issue sizes smaller than $500m, which would not be included in some ETFs’ investable universe. We have found great relative value in these smaller issues, partially due to a high liquidity premium for bondholders and the inability of larger strategys and passive strategies to invest in these credits, resulting in a higher yield for these securities.

While market volatility continues to be a headwind, the medium-term prospects of higher yields, combined with a weakening global economy, which should be positive for fixed income, suggests to us a much greater return potential moving into 2023. In the meantime, we feel that our bias towards higher quality government bonds and credit, together with the structural diversification in place across our three risk buckets, means we are well-positioned for unpredictable markets.

- Defensive / Intermediate / Aggressive in the context Global Strategic Bonds strategy are proprietary AXA IM terms and describe the way in which we broadly segregate the strategy’s investible bond universe. We view Defensive bonds as those where performance is predominantly driven by interest rate movements, such as government bonds. Intermediate bonds are those where performance is driven by a mixture of interest rates and credit spread, such as investment grade corporate bonds. Aggressive bonds are those where performance is driven predominantly by credit spread. The descriptions above represent our strategic approach only and do not equate to the stated investment objectives as per the prospectus.

- Source: As at 18 November 2022

- Source: AXA IM, Bloomberg, 9 November 2022

- Source: AXA IM, Bloomberg, ICE BofA Global Corporate Index, as at 31 October 2022.

- Source: AXA IM, Bloomberg as at 18 November 2022

Investment Risks

Counterparty Risk: failure by any counterparty to a transaction (e.g. derivatives) with the strategy to meet its obligations may adversely affect the value of the strategy. The Strategy may receive assets from the counterparty to protect against any such adverse effect but there is a risk that the value of such assets at the time of the failure would be insufficient to cover the loss to the Strategy.

Derivatives: derivatives can be more volatile than the underlying asset and may result in greater fluctuations to the Strategy's value. In the case of derivatives not traded on an exchange they may be subject to additional counterparty and liquidity risk.

Geopolitical Risk: investments issued or traded on markets in different countries may involve the application of different standards and rules (including local tax policies and restrictions on investments and movement of currency), which may be subject to change. The Strategy's value may therefore be impacted by those standards/rules (and any changes to them) as well as the political and economic circumstances of the country/region in which the Strategy is invested.

Interest Rate Risk: fluctuations in interest rates will change the value of bonds, impacting the value of the Strategy. Generally, when interest rates rise, the value of the bonds fall and vice versa. The valuation of bonds will also change according to market perceptions of future movements in interest rates.

Securitised assets or CDO assets risk: Securitised assets or CDO assets (CLO, ABS, RMBS, CMBS, CDO, etc.) are subject to credit, liquidity, market value, interest rate and certain other risks. Such financial instruments require complex legal and financial structuring and any related investment risk is heavily correlated with the quality of underlying assets which may be of various types (leveraged loans, bank loans, bank debt, debt securities, etc.), economic sectors and geographical zones. Emerging Market Risks: emerging markets or less developed countries may face more political, economic or structural challenges than developed countries. As a result, investments in such countries may cause greater fluctuations in the Strategy's value than investments in more developed countries.

Liquidity Risk: some investments may trade infrequently and in small volumes. As a result, the strategy manager may not be able to sell at a preferred time or volume or at a price close to the last quoted valuation. The strategy manager may be forced to sell a number of such investments as a result of a large redemption of shares in the Strategy. Depending on market conditions, this could lead to a significant drop in the Strategy's value and in extreme circumstances lead the Strategy to be unable to meet its redemptions.

Credit Risk: the risk that an issuer of bonds will default on its obligations to pay income or repay capital, resulting in a decrease in Strategy value. The value of a bond (and, subsequently, the Strategy) is also affected by changes in market perceptions of the risk of future default. The risk of default for high yield bonds may be greater. Risks linked to investment in sovereign debt: Where bonds are issued by countries and governments (sovereign debt), the governmental entity that controls the repayment of sovereign debt may not be able or willing to repay the capital and/or interest when due in accordance with the terms of such debt. In the event of a default of the sovereign issuer, a Strategy may suffer significant loss.

High yield bonds risk: These bonds are issued by companies or governments with lower credit ratings and as such are at greater risk of default or rating downgrades than investment grade bonds.

Contingent convertible bonds (“CoCos”): these financial instruments become loss absorbing upon certain triggering events, which could cause the permanent write-down to zero of principal investment and/or accrued interest, or a conversion to equity that may coincide with the share price of the underlying equity being low. It is possible in certain circumstances for interest payments on certain CoCos to be cancelled in full or in part by the issuer, without prior notice to bondholders. Further explanation of the risks associated with an investment in this Strategy can be found in the prospectus.

Important information

No assurance can be given that our investment strategies will be successful. Investors can lose some or all of their capital invested. Our strategies are subject to risks including, but not limited to: equity; emerging markets; global investments; investments in small and micro capitalisation universe; investments in specific sectors or asset classes specific risks, liquidity risk, credit risk, counterparty risk, legal risk, valuation risk, operational risk and risks related to the underlying assets.

Disclaimer

Not for Retail distribution: This marketing communication is intended exclusively for Professional, Institutional or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This marketing communication does not constitute on the part of AXA Investment Managers a solicitation or investment, legal or tax advice. This material does not contain sufficient information to support an investment decision.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Information concerning portfolio holdings and sector allocation is subject to change and, unless otherwise noted herein, is representative of the target portfolio for the investment strategy described herein and does not reflect an actual account . The performance information shown herein reflects the performance of a composite of accounts that does not necessarily reflect the performance that any particular account investing in the same or similar securities may have had during the period. Actual portfolios may differ as a result of client-imposed investment restrictions, the timing of client investments and market, economic and individual company considerations. The holdings shown herein should not be considered a recommendation or solicitation to buy or sell any particular security, do not represent all of the securities purchased, sold or recommended for any particular advisory client, and in the aggregate may represent only a small percentage of an account’s portfolio holdings.

Representative Accounts have been selected based on objective, non-performance based criteria, including, but not limited to the size and the overall duration of the management of the account, the type of investment strategies and the asset selection procedures in place. Therefore, the results portrayed relate only to such accounts and are not indicative of the future performance of such accounts or other accounts, products and/or services described herein. In addition, these results may be similar to the applicable GIPS composite results, but they are not identical and are not being presented as such. Account performance will vary based upon the inception date of the account, restrictions on the account, along with other factors, and may not equal the performance of the representative accounts presented herein. The performance results for representative accounts are gross of all fees and do reflect the reinvestment of dividends or other earnings.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.