Sterling Inflation-Linked Bonds: The importance of duration

Key points:

- Inflation linked bonds offer a rising return in line with inflation indexation

- Recent performance of the sterling inflation linked bonds market has disappointed relative to investor expectations, despite rising inflation in 2022, due to sensitivity to interest rates for longer-dated bonds; shorted-dated bonds meanwhile have outperformed

- Inflation-linked bonds can play a strategic role in asset allocation as a hedge against inflation and a source of diversification, but as recent market performance shows security selection can make a difference to overall return

The relentless march of inflation in 2022 has put inflation-linked bonds in the spotlight, resulting in significant inflows into the asset class. Yet despite an apparently supportive backdrop, returns for the asset class have been somewhat disappointing and thus confusing for investors.

Given that inflation remains stubbornly persistent, it is worth reflecting on the lessons that recent market performance hold for investors looking for protection against inflation. We continue to believe that inflation-linked bonds can have a strategic role to play in asset allocation – as a hedge against inflation and a source of diversification – but managing duration exposure is also critical.

What is an inflation-linked bond?

Like a regular bond (often to referred to as a ‘nominal bond’ in this context), an issuer of an inflation-linked bond (ILB) asks for a principal that it agrees to pay back on a certain date, and makes regular interest payments (called the coupon) at a defined rate over the life of the bond. Unlike nominal bonds, however, the value of the principal will vary according to the rate of inflation.

This means that as prices rise, so will the value of the principal. As the value of the principal increases, so too does the value of the coupon, meaning that the regular interest payments will also increase in line with inflation.

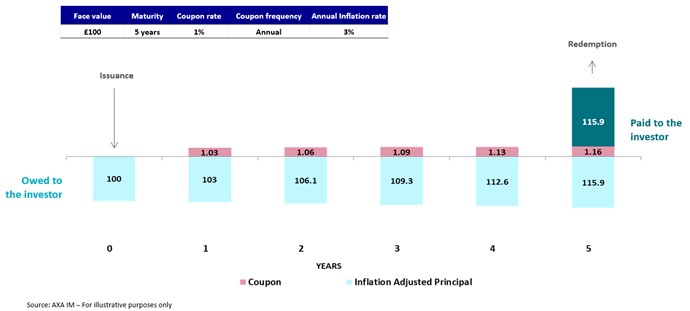

For example, a five-year ILB with a principal of £100 pounds and a coupon of 1% will initially have a redemption value of £100 and pay an annual coupon of £1.

If we assume a rate of inflation of 3% a year for the life of the bond, then at the end of year one the value of the principal will rise to £103 and the coupon to £1.03. In year two, the principal will rise to £106.10 and the coupon rise to £1.06, and so on over the life of the bond. The inflation impact will compound until, in the final year, the coupon will be £1.16 and the bond holder will get a payout of £115.90 for the principal.

The life cycle of an inflation linked bond

Of course this is a simplification of what can be a complex calculation – ILBs are typically revalued daily against an appropriate inflation index, such as RPI, CPI, or HICP, depending on the market and the issuer, and coupons can be paid more frequently than once a year.

Sources of return: break-evens and duration

Coupon rates for ILBs are usually lower than the rates for equivalent nominal bonds. This can reduce borrowing costs for issuers, while giving investors an opportunity to generate returns from a view on inflation. This introduces one of the key sources of return – break-even rates.

The break-even rate is the level of inflation where an investment made in an ILB equals the return of an investment made in a nominal bond. It reflects the expected rate of inflation until the bond’s maturity that is embedded in current market prices. For example, if you have a 10-year ILB offering a yield of 1% and a 10-year nominal bond of 3.25%, then the break-even rate of inflation for the ILB is 2.25% over the life of the bond. This is the level of inflation where the return from the ILB will match the return of the nominal bond.

If inflation goes above this break-even rate, then ILBs start offering a superior return to the equivalent nominal bond. This can be particularly helpful if inflation rises to a level where real returns on nominal bonds are negative, providing a hedge against high inflation within a bond portfolio.

As with nominal bonds, duration should be taken into consideration. ILBs are also sensitive to changes in interest rates depending on their maturity, and rates return can be an important contributor to performance.

Longer-duration ILBs tend to perform better when interest rates are stable or falling; historically they have delivered the best return in the ‘late stages’ of an economic cycle or during episodes of quantitative easing. Short duration ILBs are less sensitive to interest rates and tend to perform better when inflation rises sharply due to their higher sensitivity to inflation indexation.

Recent performance: short duration wins the race

As inflationary pressures have risen, many sterling-based investors turned to inflation-linked gilts looking for protection from inflation. As well as using mutual funds, many investors also chose to buy individual ILBs directly. This comes with tax advantages, but can be a risky strategy given the need to buy the ‘right’ bond for the 'right’ environment, rather than benefitting from the greater diversification that a fund investment can offer.

Given the sharp move higher in yields this year, the relative performance of these investments has been driven by the underlying maturity profile. The sterling inflation-linked gilt index is weighted heavily towards longer-dated bonds. This structural feature has developed over recent decades, as the UK government has tended to issue longer-dated bonds, in part to meet the demand from pension funds to hedge their long-term inflation risk.

As a consequence, the value of an investment into the all-maturity sterling inflation-linked index has fallen sharply in value in 2022 due to its high duration component. Longer-dated ILBs are highly sensitive to interest rates moves and, in the current rising-rate environment, long duration has made a strong negative contribution to performance. In contrast, short-dated ILBs have been able to offer protection through the positive contribution of inflation indexation.

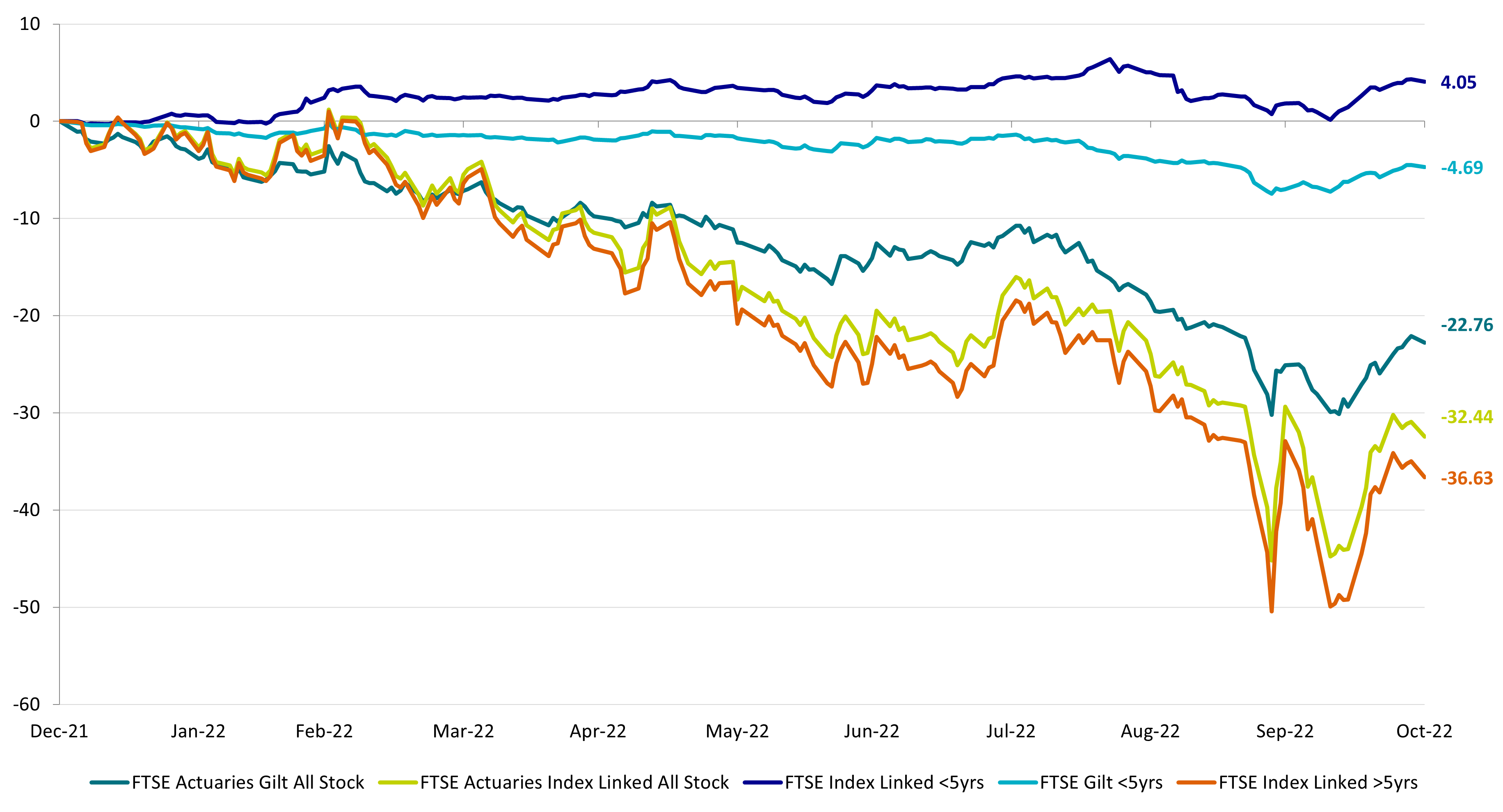

The chart below shows the impact of rising inflation and interest rates expectations on performance of both nominal and inflation-linked gilt indices of different maturities since the start of the year.

Short duration linkers – positive return in an otherwise negative market

Year-to-date returns as at 31/10/2022. Source: AXA IM, Bloomberg.

As the chart demonstrates, the sharp rise in inflation has been especially powerful for short-duration ILBs, driving them into positive territory when virtually all other asset classes have been strongly negative. Meanwhile, without the protection offered by the short end and the even-longer duration, >5-year ILBs have fallen the most over the year to date.

The impact of inflation protection that ILBs bring can be seen in the difference between the <5 year nominal gilts (the light blue line) and <5 year inflation-linked gilts (the dark purple line): the difference of around 9% is just shy of the rate of UK inflation at the end of October.

It is worth bearing in mind that ILB performance will differ according to the relative inflation expectations of different markets. Inflation in the UK is potentially set to remain higher for longer than in the US and Europe, driven by supply chain issues exacerbated by Brexit and sterling weakness that is driving up the cost of imports. This will have an impact on returns relative to other territories.

The place of ILBs in portfolios

Investors clearly recognise the value of inflation protection, as billions have poured into the sector since inflation started to rise. An allocation to ILBs could help to maintain the value of coupons and the real value of the principle of bonds nearing maturity. And of course, a properly managed allocation to ILBs can continue to be a source of returns, as can be seen by the returns of the asset class over the years.

However, 2022 has shown us that there is a need to be wary of the duration component within an ILB allocation. It is worth considering an approach to inflation protection that increases the contribution to performance from inflation indexation and break-even management, while reducing the overall rates component, or a more dynamic approach to managing duration to adjust exposure according to economic conditions.

Perhaps more so than with many other asset classes, expertise and active management are required within an inflation-linked bond strategy. A considered approach could provide inflation protection when it is needed most and avoid any nasty surprises that may be lurking beneath the surface.

Fixed Income

We cover a broad spectrum of fixed income strategies to help investors build diverse portfolios that can be more resilient to economic and market shifts.

Find out moreDisclaimer

Not for Retail distribution: This marketing communication is intended exclusively for Professional, Institutional or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.