New opportunities for bonds as the rules of the game evolve

As central banks and investors grapple with the problem of inflation, we are beginning to see what might be light at the end of the tunnel for bonds.

- Persistent inflation, rising interest rate expectations and geopolitical stress have combined to create what has been the worst first half of the year for bonds on record

- The stress has been felt most acutely in rates markets, where a lot is already priced in; attention is now starting to shift from the inflation story to weaker growth

- Yields are more attractive than they have been for some time, meaning that bond prices have fallen significantly and could provide gains when sentiment improves

Investors this year have had a lot to deal with. Crucially, surging energy prices and geopolitical uncertainties arising from the Russian invasion of Ukraine have added to the inflationary pressures that began to appear as the economy emerged from Covid-related lockdowns late last year. Central bank response has gradually become more hawkish as inflation has become more entrenched, meaning interest rate expectations have been rising throughout the year.

The toughest bond market ever?

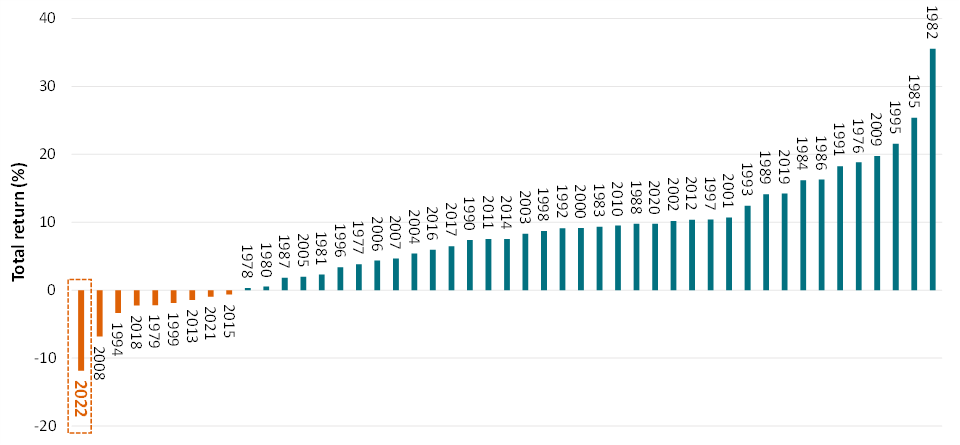

These factors have combined to create a negative environment for all parts of the fixed income market, with higher government bond yields and wider credit spreads leading to a correlated sell-off. Figure 1, below, shows year returns of the US Corporate Bond market since the index began in 1976, from worst to best, putting the extent of 2022’s drawdown into perspective.

Figure 1: US Corporate Bond Index Total Returns (1976 – 2022)

Source: AXA IM, Bloomberg, ICE BofA, as at 30/06/2022.

At the heart of this heightened volatility is the central question: where will inflation land? And this provokes a secondary question: how far central banks are prepared to go in raising interest rates to tackle inflation, whilst being conscious of avoiding a hard landing?

Clearly, a sort of regime change is underway after years of low inflation and low yields. Although we still believe that inflation will not remain entrenched at current levels, the jury is still out as to whether the landing point will be near central bank targets (i.e. 2%) or somewhere higher. The aggressive re-pricing of all asset classes in 2022 reflects this uncertainty.

Nowhere has the pain been felt more than in rates markets. Navigating through this environment has been very challenging, particularly managing duration. We have been quite active on our outright duration exposure, rather than structurally short, in the belief that a lot had been priced in already. This has not worked as we would have hoped. That said, outright negative contribution from rates was partially offset by the positive contribution from curve positioning, namely our preference for flattening trades and much greater concentration in long-dated US treasuries over short-dated.

Timing holds the key

As a long-only, total return strategy, we tend to focus more on how far through the journey we are to ‘peak’ inflation, interest rates and spreads, than on trying to time the bottom of the market. With this perspective in mind, we strongly believe that the re-pricing in rates markets is a good way already through the journey, even if inflation has not yet peaked. For spreads, however, we have already travelled some of the way, pricing in a pick-up in defaults, but not yet to levels which historically have pointed to more severe downturns. A lot should depend on whether we get a soft or hard landing from the current hiking cycle.

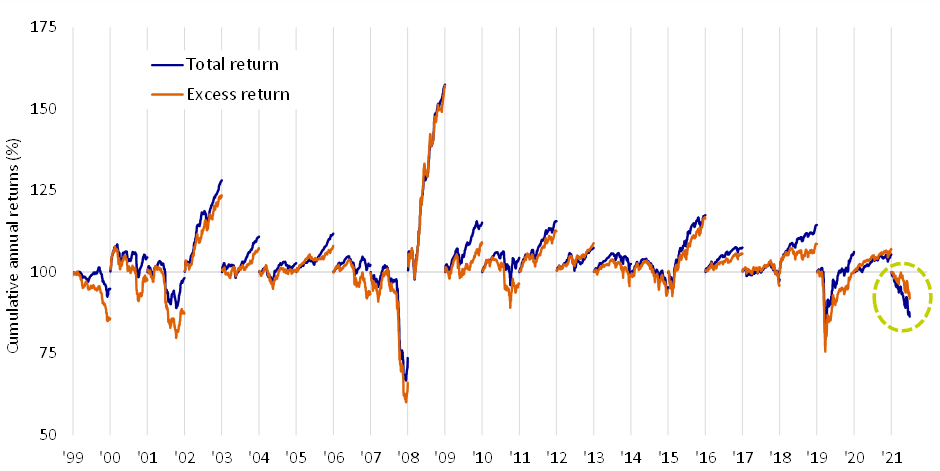

This is emphasised by comparing total returns and excess returns in the high yield market. During previous drawdowns, the spread component has tended to drag down returns. However, if we look at 2022, unusually the total return is currently underperforming the excess return, such as been the magnitude of the rates sell-off (Figure 2).

Figure 2: US High Yield Index – Cumulative Total vs. Excess Returns (2000 – 2022)

Source: AXA IM, Bloomberg, ICE BofA, as at 30/06/2022.

This suggests two things:

- We might see a weaker period for spreads in the coming months

- A lot has been priced into rates markets already

This means that we may have reached the point of peak bearishness towards government bonds and, with attractive entry points opening up, buyers may be coming back.

To reflect this, at a macro level we have been shifting our asset allocation away from lower-quality credit, given that we can now find very attractive yield in higher-quality investment grade names and government bonds.

At a micro level we are still comfortable holding lower-rated names in the US high yield market. We have 6% - 7% in CCCs, issued by companies with stable business models and predictable cash flows offering a high carry. Even if spreads do head wider, the fundamentals of the US high yield market remain relatively healthy after many years of strong monetary and fiscal support. We expect default rates to remain relatively moderate, albeit higher than today.

What goes down, must come up

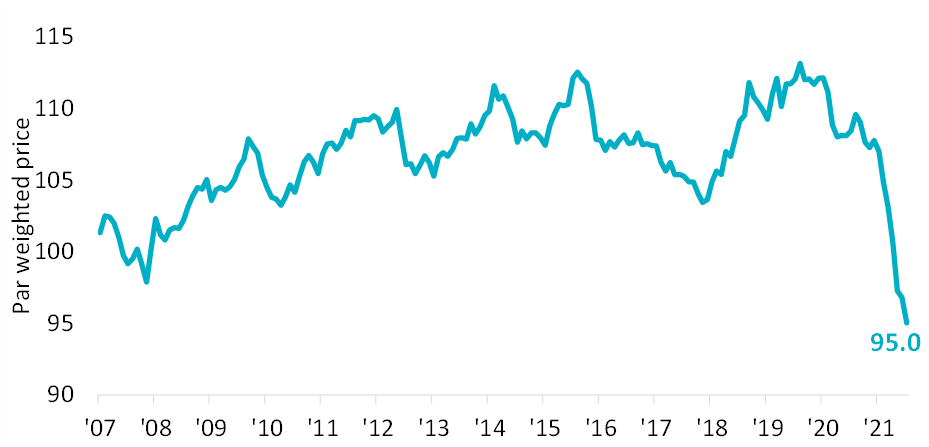

While we’re not out of the woods yet, the good news for fixed income investors is that the medium-term outlook appears to be much more positive than it has for some time. The flipside of falling bond prices is that yields are looking more attractive after many years of low, and even negative, yields. After a period of price depreciation there is also significant upside potential if we can avoid defaults amongst the bonds we hold, thanks to fixed income’s ’pull-to-par’ effect. Taking a Global Aggregate Index (composed of sovereigns and high-quality credit), the average weighted price of the underlying bonds is currently trading at around a cash price of 95 – the lowest level in recent memory.

Figure 3: Global Broad Market Index – Average Bond Price (2008 – 2022)

Source: AXA IM, Bloomberg, ICE BofA, as at 30/06/2022.

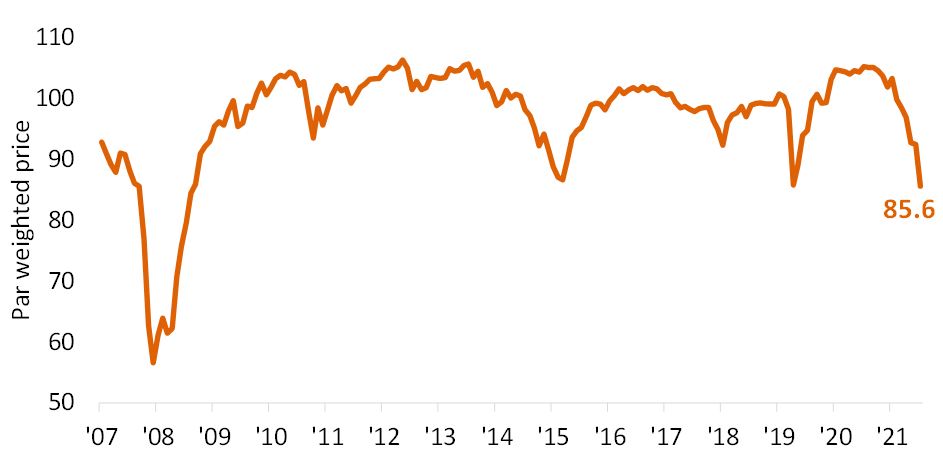

Turning to a much lower quality market such as US high yield, the current average index cash price of 86 is as low as any point since the global financial crisis.

Figure 4: US High Yield Index – Average Bond Price (2008 – 2022)

Source: AXA IM, Bloomberg, ICE BofA, as at 30/06/2022.

Discounts at these historic levels could tempt investors to close their long-standing underweight positions in fixed income, now that it offers more yield and spread. We are not quite there yet: we need inflation prints to have peaked, or to be further along the Fed rate hiking cycle before the tipping point arrives. But we would argue that fixed income should now start to compete for capital once more.

No quick fixes, but we are finding a way through

We expect 2022 to remain volatile. The ongoing conflict in Ukraine, the expected shift in monetary conditions and the gradual reduction of asset purchasing programmes by central banks are all weighing on investors. To navigate a path through these headwinds we will continue to use our flexibility and tactical portfolio hedges, for example using futures to dynamically manage duration, and credit default swaps to adjust credit risk.

However, after such a tough period, we think that a lot of bad news has already been priced into bond markets and their ability to surprise to the upside should not be underestimated. With this in mind, we are starting to consider options for an improving outlook.

Important information

No assurance can be given that our investment strategies will be successful. Investors can lose some or all of their capital invested. Our strategies are subject to risks including, but not limited to: equity; emerging markets; global investments; investments in small and micro capitalisation universe; investments in specific sectors or asset classes specific risks, liquidity risk, credit risk, counterparty risk, legal risk, valuation risk, operational risk and risks related to the underlying assets.

Additional risks

Investors in this strategy should be aware of the following additional risks:

- Counterparty Risk: Risk of bankruptcy, insolvency, or payment or delivery failure of any of the Sub-Fund's counterparties, leading to a payment or delivery default.

- Operational Risk: Risk that operational processes, including those related to the safekeeping of assets may fail, resulting in losses.

- Liquidity Risk: risk of low liquidity level in certain market conditions that might lead the Sub-Fund to face difficulties valuing, purchasing or selling all/part of its assets and resulting in potential impact on its net asset value.

- Credit Risk: Risk that issuers of debt securities held in the Sub-Fund may default on their obligations or have their credit rating downgraded, resulting in a decrease in the Net Asset Value.

- Impact of any techniques such as derivatives: Certain management strategies involve specific risks, such as liquidity risk, credit risk, counterparty risk, legal risk, valuation risk, operational risk and risks related to the underlying assets. The use of such strategies may also involve leverage, which may increase the effect of market movements on the Sub-Fund and may result in significant risk of losses.

Unconstrained Fixed Income

This provides the potential flexibility to capitalise on opportunities across the fixed income spectrum as and when they arise.

Find out moreVisit our fund centre

The aim of the strategy is to generate income and any capital growth over the long term (being a period of five years or more).

View fundsDisclaimer

Not for Retail distribution: This marketing communication is intended exclusively for Professional, Institutional or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This marketing communication does not constitute on the part of AXA Investment Managers a solicitation or investment, legal or tax advice. This material does not contain sufficient information to support an investment decision.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Past performance is not a guide to current or future performance, and any performance or return data displayed does not take into account commissions and costs incurred when issuing or redeeming units. References to league tables and awards are not an indicator of future performance or places in league tables or awards and should not be construed as an endorsement of any AXA IM company or their products or services. Please refer to the websites of the sponsors/issuers for information regarding the criteria on which the awards/ratings are based. The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested. Exchange-rate fluctuations may also affect the value of their investment. Due to this and the initial charge that is usually made, an investment is not usually suitable as a short term holding.

Information concerning portfolio holdings and sector allocation is subject to change and, unless otherwise noted herein, is representative of the target portfolio for the investment strategy described herein and does not reflect an actual account . The performance information shown herein reflects the performance of a composite of accounts that does not necessarily reflect the performance that any particular account investing in the same or similar securities may have had during the period. Actual portfolios may differ as a result of client-imposed investment restrictions, the timing of client investments and market, economic and individual company considerations. The holdings shown herein should not be considered a recommendation or solicitation to buy or sell any particular security, do not represent all of the securities purchased, sold or recommended for any particular advisory client, and in the aggregate may represent only a small percentage of an account’s portfolio holdings.

Representative Accounts have been selected based on objective, non-performance based criteria, including, but not limited to the size and the overall duration of the management of the account, the type of investment strategies and the asset selection procedures in place. Therefore, the results portrayed relate only to such accounts and are not indicative of the future performance of such accounts or other accounts, products and/or services described herein. In addition, these results may be similar to the applicable GIPS composite results, but they are not identical and are not being presented as such. Account performance will vary based upon the inception date of the account, restrictions on the account, along with other factors, and may not equal the performance of the representative accounts presented herein. The performance results for representative accounts are gross of all fees and do reflect the reinvestment of dividends or other earnings.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.