Coronavirus throws down a challenge for credit analysis

Key points

- AXA IM’s credit analysis model has adapted quickly to incorporate new inputs as the COVID-19 crisis heightens sensitivity to regulatory and fiscal conditions.

- Credit analysis will have to anticipate the conditions applied to state support, and the divergent recovery paths between sectors.

- We expect those conditions, and future incentives, will favour companies committed to supporting the energy transition.

- Overall, the credit repricing has thrown up opportunities for investors whose credit analysis has kept pace with the changing conditions.

The dramatic impact of COVID-19 has created a challenge for even the most experienced credit analysts. The effects have gone far beyond those seen in the technology bubble of the early 2000s, the Enron scandal a year later, the 2008/2009 financial crisis, and in – what now seems like a small blip – the commodity crash of 2015/2016.

The depth of the downturn has been unfamiliar territory for most analysts and investors, but the response from policymakers around the world has been equally unprecedented. This collective effort has delivered some much-needed stability, but also created its own challenge for credit analysts. At AXA IM, our toolbox has evolved and expanded to take into consideration both the new market conditions and the varied suite of support measures in place around the world.

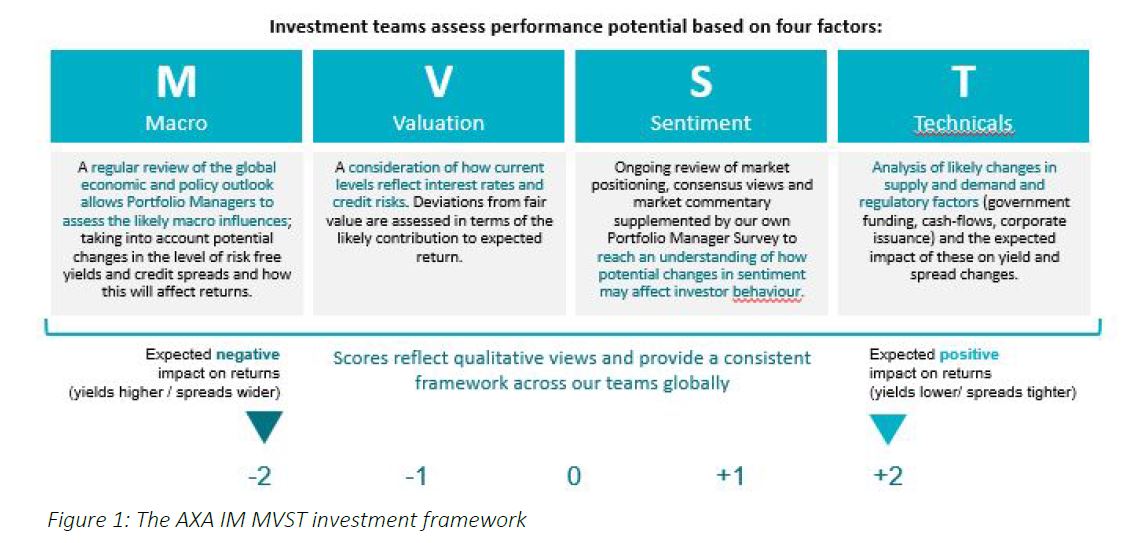

Our MVST framework (see Figure 1) draws from a number of sources. It looks at macro research on the economic and monetary policy outlook, valuation issues around credit risks, sentiment analysis that examines market behavior, and technical work which looks at the effect of regulatory measures and supply/demand factors on fundamentals. Into this have arrived a series of updated considerations – including, for example, closer scrutiny of supply chains and manufacturing footprints that may become more localised in the aftermath of the crisis.

The daily process of credit research now carries a heightened sensitivity to the pace and scale of changing conditions. As such, we closely watch government briefings for subtle changes in nature and scope of support for some companies, as well as more lingering restrictions for others. This is crucial to understanding the short-term impact on company cash flows.

A single common investment language: MVST

For an example of this we can look to France, which in late April announced it would keep large shopping centres closed after 11 May, while most other stores would be able to re-open around the country. Such policy shifts are happening on a daily basis, and cause uneven effects. In this case we had to consider how it might penalise retail landlords with large flagship assets compared with those owning a higher share of local, smaller shopping centres.

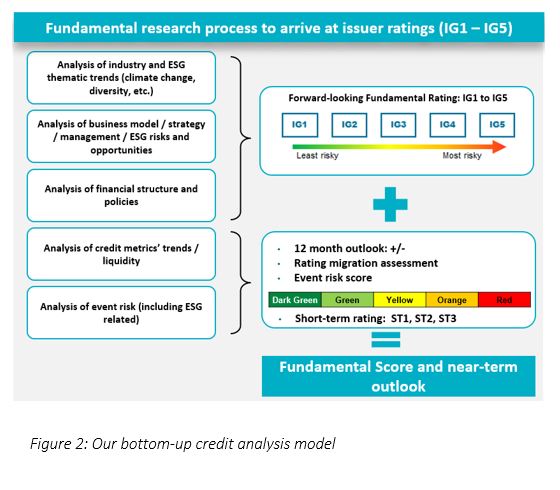

Our overall credit analysis model combines this top-down approach, with a nuts and bolts, five step bottom-up process (Figure 2) that has proved its worth over time. The goal is to create a model that can adapt quickly to the kind of new – and nuanced – inputs thrown up in this unprecedented crisis.

Tense times

It is worth recalling how the evolution of the coronavirus crisis has impacted corporate issuers in Europe in particular. In the early stages, the focal point was on near-term liquidity and refinancing needs. Many investment-grade (IG) corporate issuers benefited from an extended period of ultra-low financing costs, partly supported by corporate QE1, which drove an overall lengthening of debt maturity profiles. However, numerous issuers also relied heavily on the short-term commercial paper (CP) market, where even more attractive funding conditions could be found.

The need to ensure the continued functioning of this this market became evident in mid-March as tensions rose. On 18 March, European Central Bank (ECB) announced the Pandemic Emergency Package Programme (PEPP)2 including the purchase of short-dated commercial paper. That meant analysts could once again include access to CP in liquidity calculations – but with the caveat that we must remain mindful of any excessive use of short-term funding in debt capital structures.

The ECB has not been operating alone. European governments are countering the economic disruption through massive fiscal packages, with targeted support to households and corporations which needs to be considered as part of our credit analysis.

In the UK, the Bank of England (BoE) launched the Covid Corporate Financing Facility (CCFF)3, a short-term lending facility available for eligible large IG corporates, with a maximum amount of up to £1bn for issuers with the most solid short-term ratings i.e. A1/P1/F1. This facility was quickly tapped by UK-based companies operating in the severely disrupted transportation sector.

In France, a sizeable state-backed loan of €5bn4 was set aside for partly state-owned automaker Renault, while the national flag carrier Air France-KLM secured a €7bn aid package from the government, including €4bn state-backed loan (guaranteed by the French state up to 90%) and €3bn direct shareholder’s loan. It also secured support from the Dutch government5.

National champions?

Such moves are encouraging when we consider a company’s ability to bridge this crisis in reasonable shape. However, no government will sign a blank check. Analysts need to fully appreciate the role a company or an industry plays in each country in order to estimate whether state aid will be forthcoming or not, and how sustained it might be.

Anticipated support may be included in the credit analysis of a company considered as strategic (perhaps from a technology or national security perspective), or one which is significant national importance, for example as a key employer. The European automotive sector is an obvious case here. On the other hand, we have seen examples of large companies in financial distress failing to secure state support because their national importance is considered less pressing, notably for entities registered in tax havens.

These nuances in the market emphasise how vital is has been for our credit analysts to reinvigorate their recovery analysis skillsets.

Part of that is understanding how the ripples of this will land on the shore – any state aid is likely to come with strings attached. This is perhaps best illustrated by comments from French Finance Minister Bruno Le Maire, who said6 that a prerequisite for state aid, whether in the form of deferred taxes and/or charges or in the shape of government-backed loans, would be the cancelling of dividends. He added that the moderation of dividend payments and management pay would be expected, in any case, to demonstrate solidarity with employees affected by the crisis.

For a credit analyst, moderation of dividend payments and suspension of share buybacks should be welcome news. However, we need to consider, at least for modelling purposes, if such a decision will be permanent or if the company will simply defer shareholder distributions to a later date.

Positively, from an environmental, social and governance (ESG) perspective, we’ve seen targeted support from governments being linked to environmental commitments, with the above-mentioned aid package to Air France-KLM assuming “an ambitious environmental roadmap to accelerate the Group’s sustainable transition”7. We could also expect increased incentives for the purchase of electric and hybrid personal vehicles to boost the recovery in the troubled European automotive sector. An acceleration of a sustainable energy transition would benefit investors – and society – over the long term.

Survival rations

At some point, businesses need to stand on their own two feet. Once any urgent liquidity concerns have been addressed, credit analysts quickly turn their attention to earnings, cash flows and leverage. While government-backed loans and bond

purchases from central banks will help alleviate immediate liquidity pressure and ensure the survival of sustainable businesses, they will not prevent the unavoidable fallout from the crisis on corporate leverage as measured by debt-to-EBITDA ratios. For companies with sizeable underfunded pension obligations, leverage metrics could be further stretched as a result of low discount rates and reduced asset values.

This will be an uneven recovery, marked by pockets of strength and weakness. At AXA IM, our credit analysts will closely monitor sector-specific considerations as discrete demand recovery curves emerge. Not only will different industries see divergent patterns of growth, but there will likely be material differences within sectors, for example between airlines and cruise companies.

This is a moment for adaptability in credit analysis. Our deep and agile research into the distinctive nature of this crisis and its aftermath will allow us to separate the wheat from the chaff – and to continue providing value-adding ideas for sustainable investment opportunities to investors. Despite many challenges, one thing is certain: this ongoing crisis has provided new, attractive investment possibilities in a broad repricing that has drawn in many high-quality credits.

- ECB’s CSPP program announced in March 2016 https://www.ecb.europa.eu/press/pr/date/2016/html/pr160310_2.en.html

- €750bn Pandemic Emergency Purchase Program https://www.ecb.europa.eu/press/pr/date/2020/html/ecb.pr200318_1~3949d6f266.en.html)

- Covid Corporate Financing Facility https://www.bankofengland.co.uk/news/2020/march/the-covid-corporate-financing-facility.

- Reuters, 29 April. https://uk.reuters.com/article/uk-health-coronavirus-renault-eu/eu-clears-french-five-billion-euro-loan-guarantee-to-renault-idUKKBN22B2GG-billion-euro-loan-guarantee-to-renault-idUKKBN22B2GG

- KLM, 25 April. https://news.klm.com/klm-grateful-for-2-4-billion-in-state-aid-pledged-by-dutch-government/

- Ref. Le Journal du Dimanche, 4 April 2020.

- Air France press release, 24 April 2020 https://www.airfranceklm.com/en/system/files/press_release_air_france-klm_group_and_air_france_secure_funding_of_eu7_billion_ve.pdf

Not for Retail distribution

This document is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document. Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ. In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.