B&M Strategy Update. How credit trading dynamics adapted to the COVID-19 crisis

In this Buy and Maintain Credit Market Update, Lionel Pernias – Head of Buy and Maintain was joined by:

- David Page, Head of Macro Research: discussing the outlook for UK recovery in the context of Brexit and global uncertainty, and

- Lee Sanders, Head of Fixed Income & FX Trading: examining liquidity in the bond markets, focusing on sterling credit

Macro conditions

- The UK has moved past the peak in new daily COVID-19 cases and in the death rate, which has allowed some easing of restrictions, but the UK is not typical in Europe and has seen a relatively protracted path of the virus – deaths per capita appear to be the second highest in the OECD. This may be due to a variety of factors, including but not limited to: higher population density; international interconnectivity; a relatively older population; and higher levels of obesity.

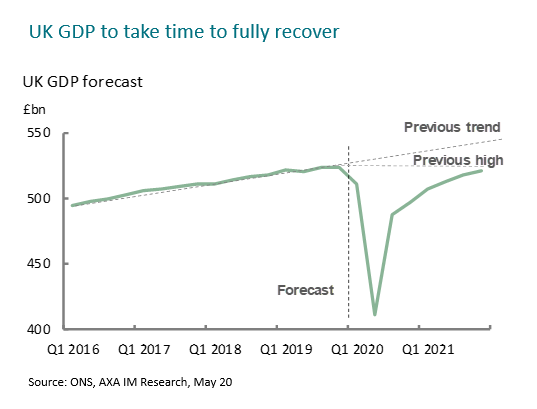

- This has slowed the loosening of the lockdown and should create a greater economic impact. We expect a contraction of about -20% for the second quarter (Q2), slightly worse than our previous forecast. We expect only a modest rebound in May at perhaps +4% with +4% to follow for June. There was some encouraging retail sales data on 19 June, but in this environment, such measures should be viewed with caution. We still expect a relatively solid rebound in Q3 – this has been an artificial economic shock and as such, the recovery has the potential to be significant, albeit not enough to regain the previous trend path. We expect GDP growth of 8% in 2021.

- Brexit remains a risk to the recovery. A full trade deal with the European Union (EU) always looked difficult, and now the pandemic has made progress far harder. The UK government has insisted it will not seek an extension of the transition period, but we continue to see this as a bargaining position designed to force concessions from the EU. We believe there are likely to be last minute changes of heart. The UK remains in a relatively weak position – the realities of the trade dynamic are unchanged and there remains a significant risk of supply shock at the end of transition. In the end, we expect the UK to move to new relationship with last-minute talks securing a hybrid deal/transition in some form.

Trading dynamics

- Liquidity in the corporate bond market has changed dramatically over the last 15 years. This latest crisis has delivered a spike in turnover. For 2020 we have already carried out transactions worth about €85bn, 57% of the total for the whole of 2019. March was a record month. This environment requires us to be on top of liquidity and organised in the way we approach execution – we need to be innovative and flexible.

- Since 2008, banks have relinquished some of their dominance of the market. However, we maintain strong relationships with all the major banking market makers and use our global footprint to ensure access to bank balance sheet at the right price. Banks still represent a significant percentage of our turnover. But at times of volatility or singled direction momentum, this route to market can hit issues.

- We have sought to mitigate potential liquidity gaps by building relationships with the Alternative Liquidity Providers (ALPs) that emerged after the 2008/2009 crisis. They have been very useful when bank liquidity has been more costly. We can add into the mix here the role of ETFs and portfolio trading, where we have seen a marked pick-up in activity, most notably in euros and dollars, but also in sterling.

- We crunch the data to better understand the intentions and inventory positions of market players. Our in-house ‘Axes’ tool constantly aggregates information from counterparties to address the liquidity challenge and enhance price discovery. This process offers an extra layer of market intelligence, allowing us to tap into liquidity more efficiently and delivering tangible benefits.

- Over the entirety of our fixed income trading we gained cost savings of 11 basis points (bps) from the observed bid/offer price in 2019 – in £ it was 16 bps. For the Buy & Maintain team over the last two years, we have consistently outperformed expected cost of execution – most importantly, we have completed over 95% of orders on the day they were created.

- The primary market has been boosted by purchase commitments from central banks. This has been most obvious among euro and dollar issuers who have come to the market with more than €/$1tn, while the sterling primary market has seen less than £100mn. The primary market has wider effects too: when issuance is light and demand high then liquidity in secondary markets can be challenging.

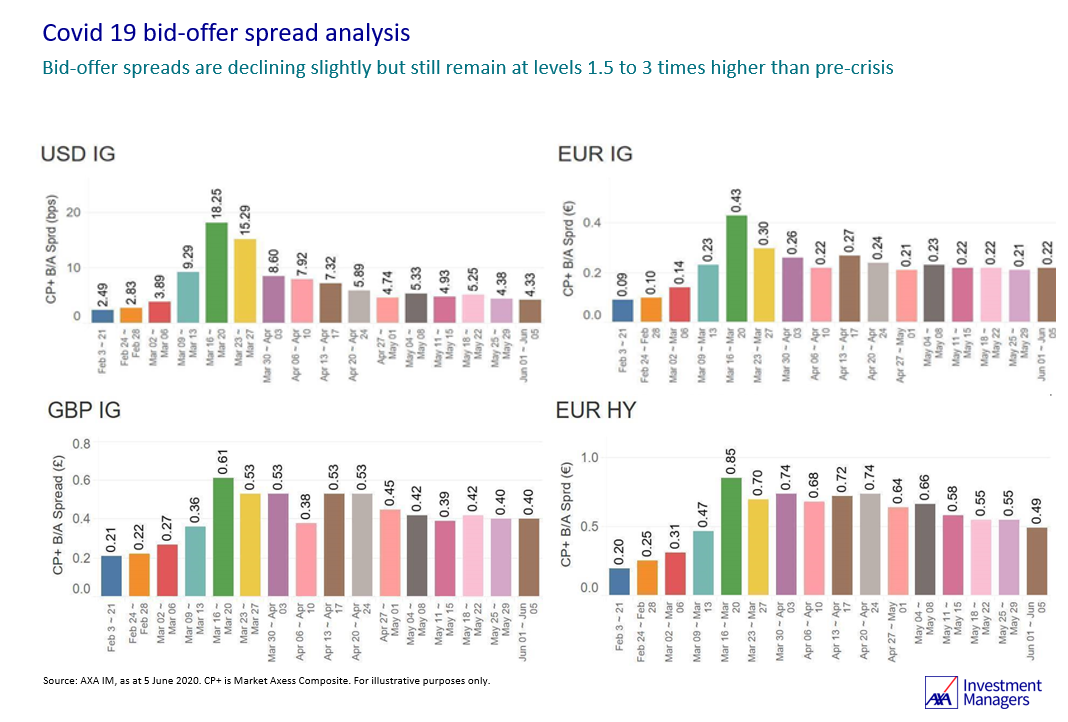

- This crisis has also seen dramatic movements in credit spreads and market velocity – when trades come thick and fast. The chart below shows $ investment-grade (IG) credit normalised more swiftly than €IG, but the £ bid/offer still remains wide. Increased velocity has also been generated by the introduction of algorithms which some firms use to build new positions or unwind old positions or to capture market share.

- We have embraced open trading, dark pools and auctions, through which we can match opposing flows without on-boarding new counterparties. Open trading has been a great addition to the tool kit and significantly helped to reduce transaction costs. This is part of a wider trend that has seen records broken in use of such tools during this period.

- In 2008, the market took a lot longer to touch the wides and therefore the period of illiquidity and crisis was longer and more systemic than the recent government-induced correction. In addition to that, the factors affecting liquidity – from the declining dominance of bank balance sheet to our own robust price discovery tools – have perhaps prepared us better to weather this new storm.

Credit market conditions

- Sterling spreads have clearly come back from their wides but are still as much as 40% cheaper than pre-crisis. This makes a big difference when you lock that spread in for 30 years.

- The backstop from central banks for fixed income remains strong and recent heavy bond issuance means that IG companies are sitting on a comfortable pile of cash and have extended debt maturities while strengthening balance sheets.

- The market will suffer bouts of volatility, that should bring new opportunities to lock in higher level of returns.

- Risks remain due to the long-term damage suffered by some companies, which emphasises the huge importance of credit research. We continue to think that the sharp economic contraction favours defensive and non-cyclical allocations which are generally less vulnerable to a downturn.

- Credit is an attractive option for insurers looking to bring risk back into portfolios, seeking credits which are less at risk from multi-notch downgrades.

- Dollars offer value, roughly a 40 bps pick up like-for-like in single-A versus sterling. We think this is a good moment to capture attractive levels of spread in long-dated credit, and we don’t expect this opportunity to last as pension schemes and insurers move in. This means we are typically looking to increase dollar allocations, targeting around 15% in credit portfolios.

Investments involve risks including loss of capital.

Not for Retail distribution

This document is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document. Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ. In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.