Where can investors potentially seek income in today’s low yielding environment?

The coronavirus pandemic has created uncertainty no matter what your investment objective. But for income seekers, who had already been short-changed in terms of attractive bond yields, the near disappearance of dividend pay-outs has further exacerbated the problem.

Lockdowns and changes in customer behaviour have had a significant negative impact on 2020 earnings for many businesses across sectors including travel and leisure, retail and energy.

What’s more, in a move to protect capital reserves, the European Central Bank has asked banks across the bloc not to pay dividends or to buy back their own shares until January 20211. In the UK, the Prudential Regulation Authority asked British banks to suspend dividends until the end of this year, and to cancel payment of any outstanding 2019 dividends2.

Research has highlighted that globally, dividend pay-outs fell some 22% to $382.2bn in the second quarter (Q2) of 2020, followed by a decline of 14.3% in Q33.

But while these developments have dominated headlines, there are still companies that are continuing to return cash to shareholders or planning to do so in future. In the UK for instance, Q3 dividends were the lowest in a decade, falling 49% from the period last year, or 45% excluding special dividends. But there was still a positive trend with fewer cutting or cancelling pay-outs in Q3 compared to Q24.

In fixed income, where yields were already extremely low, the spread of the virus and its economic consequences have pushed even more money into traditional ‘safe-haven’ assets such as government bonds – in turn, driving prices up and yields down. At the mid-point of the year, more than 60% of the global bond market yielded less than 1%, according to reports5.

For now, the hunt for income has become trickier, but the game is far from up. Investors still have potentially attractive options to explore.

AXA IM CIO Core Investments, Chris Iggo, said: “Dividend and bond yields are historically low in the current low growth and interest rate environment. This is unlikely to change unless we see significant improvements in nominal GDP growth in the years ahead. In turn this means income is harder to come by.”

He explained that investors may need to diversify their sources of income even more – and could potentially look to selective and actively managed equities, corporate bonds including high yield, emerging markets, inflation-linked bonds and even some securitised products, where the underlying cash flows are of high-credit quality.

Iggo said: “Relying on equity dividends alone is unlikely to satisfy the requirements of many investors who are seeing income. In the US, for example, share buy-backs have also played a major role in total returns for equity investors – this is typically a feature of higher-growth companies which have built up large cash balances.”

Below, four AXA IM experts explain why, in their view, investors seeking income may have to look deeper into each market, cast their net across asset classes and consider taking on more risk if appropriate.

AXA UK Equity Income strategy manager Simon Young

Dividends have come further down the priority list for companies following the COVID-19 outbreak. Company management teams have rightly prioritised cash generation and conservation, especially those unable to operate their business during lockdowns. The recent news from first BioNTech and partner Pfizer, and subsequently Moderna – that they had developed the first effective coronavirus vaccines - is a potential gamechanger, providing a significant boost to markets, and the outlook for 2021 and beyond. While this is very positive news, the challenge will be mass-deployment logistics. But certainly, I believe this development bodes well for dividend-seeking investors.

Investors have asked about the likely speed of any bounce back in dividends. 2020 will see the biggest cut in UK dividends for the past 50 years, with the overall decline likely to be 40-50%. The good news is that despite the cuts, the FTSE All Share Index yields a little over 3%6, well in excess of inflation, and we expect dividends to start to recover in 2021.

Most management teams understand the importance of dividends and the role they play in compounding returns. In our conversations with senior management across a wide range of sectors it is clear to me that company boards are keen to return to paying dividends. Indeed, we have seen a growing number of companies across a range of sectors – such as Admiral and Sabre in motor insurance and engineering company Rotork – reinstate previously deferred dividends. Allied to this, trading for many companies has been better than the scenarios they put out amid the first lockdown and we have seen a definite pickup in consumer demand over the summer. We can also potentially look forward to the banks sector, which was advised by the Prudential Regulation Authority to defer dividend payments in 2020, resuming payments in 2021. I envisage 5-10% growth in dividends paid by UK companies in 2021.

There is always a balance for investors between getting paid dividends today and returns being reinvested to generate greater dividends in future. This is where stock selection plays an important role. The pandemic has highlighted areas of weakness for many businesses and brought a realisation that businesses and their employees need to be more adaptable in future. This flexibility comes in many forms, whether it is helping staff to work from home, hosting events virtually, doing more business online or adapting a product range to cater for a change in consumer demand or circumstances. I prefer to invest in companies that keep investing, especially where it increases their likely resilience in the event of a second or third wave of coronavirus or to ward off growing competition in the future. These are the businesses that are potentially more likely to compound earnings and grow their dividends over the longer term.

AXA IM global income generation strategy manager Andrew Etherington

Companies that pay a higher dividend have tended to provide a greater total return with dividends reinvested – but this year has shown that is not always the case.

The chart below compares the MSCI World High Dividend Yield Net Total Return Index, which includes large and mid-cap stocks with higher than average dividend yields that are deemed to be both sustainable and persistent7, with the broader MSCI World Net Total Return Index. But this year, companies that have paid consistently good dividends have not necessarily been those whose share prices have performed best, as gains have been driven in part by growth companies often with high levels of cash and paying little or no dividends.

Source: Bloomberg/MSCI, in US dollar terms, as of 30 October 2020.

So, in the current market environment, investors who are seeking income should ask themselves whether it is income alone, or also capital growth with the valuation risks associated with it, that is important to them in the short term, while they balance this with their longer-term objectives.

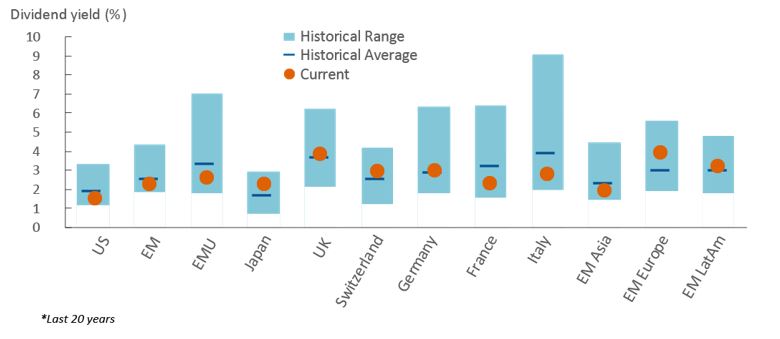

What’s more, dividend yields also vary widely across equity markets, and what investors in one geography might consider an acceptable yield could be very low for another. The chart below shows the historical range and average dividend yield across various markets over the last 20 years – we can see that currently, yields are in most cases below their historical average, but in some countries, the yield is above average. It therefore makes sense for investors seeking yield to consider diversification across geographical equity markets – as well as across asset classes.

Source: Datastream and AXA IM, as of 30 October 2020

However, while central banks’ policies remain extremely accommodative, bond yields will likely remain historically depressed.

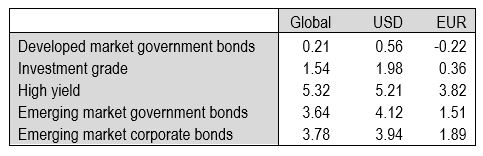

The table below shows the yields that were on offer at the time of writing across different classes of bonds, in local currency terms (global), US dollars and euros. Of course, the exchange rate can have a big impact on returns, but there is nonetheless a significant difference between developed market government and investment grade corporate bonds, and the riskier areas of high yield and emerging market government and corporate bonds.

Source: ICE Indices, via Bloomberg, as of 4 November 2020. ‘Global’ comprises US dollar (USD), euro (EUR) and pound sterling (GBP) bonds.

In terms of our conviction across multi-asset strategies, we took steps earlier this year to increase the risk mitigation capacity of our strategies. As we passed the nadir and central banks put their balance sheets to work, we increased our exposure to credit and from April, increased exposure to global equities and later to emerging markets equities.

With interest rates expected to remain low for some time, and central bank stimulus strategies seeing them purchase not only investment grade but also parts of the high yield universe, it is perhaps as important as ever for investors with an income objective to retain a globally diversified exposure in their portfolios.

AXA IM Head of Total Return & Fixed Income Asset Allocation Nick Hayes

The current positioning within our global active fixed income strategies rests on a barbell approach which balances high quality developed market government bonds, with short to medium duration, with higher-yielding credit and emerging markets bonds. This reflects our view that high quality credit appears a very crowded trade at the moment, and we prefer to delve deeper into the credit universe in search of value.

High yield and emerging markets are two of the areas within fixed income where investors can potentially find income right now. For example, Asian high yield is a fairly leveraged environment and therefore quite risky – but there are names that are yielding between 8% and 12%, which is very attractive. US high yield is also interesting from an income perspective, particularly in the CCC-rated space which we have favoured for some time.

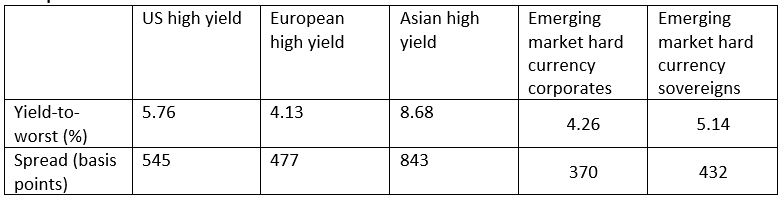

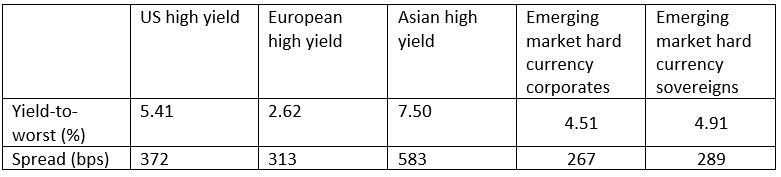

The table below compares the yield-to-worst – that is, the lowest possible yield without the bonds in question defaulting, and the spread - the difference in yield compared to US Treasuries - across various high-yield and emerging market indices, as of 30 September 2020 against the same metrics at the end of December 2019. While yields have risen across most of the markets, albeit apart from emerging market hard currency corporates, spreads have widened considerably, as the level of risk is deemed to have increased.

30 September 2020

31 December 2019

Source: Bloomberg and JP Morgan, using data from ICE BofA US High Yield Index, ICE BofA Euro High Yield Index, Ice BofA Asian Dollar High Yield Corporate Index, EMBI Global Diversified Index, CEMBI Broad Diversified Index.

However, the coronavirus pandemic has affected sectors and companies in different ways, meaning fundamental credit analysis is more important than ever. We are evaluating opportunities with an issuer by issuer approach, paying close attention to factors like balance sheet liquidity.

There are also opportunities in inflation-linked bonds, in the US and to a lesser extent in the UK. The possibility that central banks could aggressively target higher inflation in a world where nominal yields will remain low could potentially push breakevens – the difference between a nominal bond yield and an inflation-linked bond of the same maturity - even higher.

Even for investors who are seeking income there is, we believe, still a place in the investment strategy for lower-yielding government bonds. They can offer some protection against volatility and to offset holding riskier assets.

We maintain a diversified pool of different fixed income assets across our global bond strategy, combining top-down asset allocation and macro views with bottom-up fundamental analysis and security selection throughout the economic cycle.

To find value within the investment grade spectrum, we are investing in subordinated financial bonds in European and sterling credit, combined with high yield bonds in the US, Europe and Asia, as well as a well-diversified pool of sovereign and corporate emerging market assets.

At the same time, we are using credit default swap indices as a hedging strategy to potentially provide protection given the prospective headwinds on the horizon.

Phil Roantree, manager of AXA IM’s sterling corporate bond and sterling strategic bond strategies

Investors who do not want to take too much risk might potentially look to government bonds – but are likely to find themselves short on income at the moment. For example, the yield on the six-year UK government bond is currently negative. An investor would need to look at bonds with a longer maturity to get a positive return, so must decide is it worth risking capital to get a higher return (yield) – a combination of income and capital growth?

UK 10-year government bonds are currently yielding around 0.27% - only marginally more than cash - but buying a longer maturity increases the duration, or price sensitivity to a move in yield, meaning if interest rates rise, the value of the bond could fall and wipe out the extra yield.

With government bonds a so-called safe-haven asset, they have benefitted from recent COVID-induced uncertainty; the downward move in interest rates and bond yields has resulted in strong capital gains. Yields might rise on improving economic sentiment/removal of uncertainty, although this may be a way off in the current pandemic-affected world.

Higher yields can be found in corporate bonds but there is not only duration risk but also credit risk, which considers the company’s ability to repay its debt. The least risky from a credit perspective are those rated AAA, but such bonds only offer a relatively small spread compared to gilts. The lowest rated investment grade bonds – BBB rated – are riskier but offer higher spreads.

Looking at the overall market, corporate bonds offer an extra yield of 153 basis points (bp) over government bonds, with a total yield of around 1.78%8. AAA rated spreads are 36bp (yielding 0.44%) while BBB spreads are 202bp (yielding 2.24%). A broad portfolio reduces individual credit risk, although with most corporate bonds having a minimum dealing size of £100,000 nominal, investors would need a significant sum in order to achieve a diversified portfolio.

Subordinated bonds have proven popular in a low yield environment where investors are searching for income. Frequently issued by banks and insurance companies to raise capital, they are increasingly being used by corporates. As the name suggests, they rank below the senior bonds a company issues, with lower credit ratings to reflect this.

To compensate investors for the extra risk, spreads are higher than for senior bonds issued by the same company. However, these bonds usually have a long final maturity date, but with a much earlier (five to 10 year) call date. This uncertainty of maturity removes some of the traditional UK investor base from investing in this type of bond.

Remember though, when markets are in risk-off mode, prices of lower rated and subordinated bonds can fall by substantially more than high quality corporate bonds and gilts.

A combination of exceptionally low interest rates and government support is likely to underpin this market for some time even if the shape and strength of the economic recovery remains uncertain.

Some sectors, however, are still operating significantly below pre-COVID-19 levels, putting pressure on companies’ near-term profitability and ability to pay debt - but with significant cash and access to funding, bonds in some of these companies offer attractive yields. Ultimately, investors seeking income must decide how much risk – and what type of risk - they are willing to take.

The hunt for yield continues

While it cannot be denied that finding income in the current conditions is not as easy as it has been in the past, these different perspectives demonstrate that there is yield on offer – but it is a question of risk versus reward. There may be alternative asset classes that provide better income streams, but for most investors, these are harder to access, and less liquid. However, while returns are weaker, so is inflation – so for investors who want ‘real income’ above inflation, the bar is set a little lower. A diverse approach across equities and fixed income, spanning geographies and the investment grade spectrum, combined with careful active selection, could potentially give investors some of the income they are looking for – and leave them positioned to reap the benefits when the market environment improves.

- https://www.bankingsupervision.europa.eu/press/pr/date/2020/html/ssm.pr200728_1~42a74a0b86.en.html

- https://www.bankofengland.co.uk/prudential-regulation/publication/2020/pra-statement-on-deposit-takers-approach-to-dividend-payments-share-buybacks-and-cash-bonuses

- Janus Henderson Global Dividend Index, August 2020, https://cdn.janushenderson.com/webdocs/JHGDI+Ed+27+Report+_Global.pdf and November 2020 https://cdn.janushenderson.com/webdocs/Report+28+-+UK.pdf

- https://www.investmentweek.co.uk/news/4021989/uk-dividends-suffer-49-fall-q3-link

- Financial Times, 27 July 2020 https://www.ft.com/content/b44281c0-2ddb-46ae-83e2-150461faed65

- Source: Bloomberg, as at 19 November 2020

- https://www.msci.com/documents/10199/74fe7e16-759e-405c-96aa-8350623fae65

- As of 9 October 2020. Source: ICE

Not for Retail distribution

This document is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document. Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ. In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

Risk warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.