A cutting edge opportunity

- 25 November 2022 (5 min read)

AXA Framlington Biotech Fund

- Provides exposure to a rapidly expanding section of the healthcare sector – the Nasdaq Biotech Index now includes over 370 US-listed companies with a combined market capitalisation of over $1 trillion; biotech companies make up around 10% of the MSCI World Healthcare Index

- Biotech combines cutting edge innovative disruptors with established companies that provide more stable defensive returns, and offers distinct diversification benefits from general healthcare exposure

- AXA Framlington Biotech Fund brings analytical rigour thanks to the team’s science-focused academic backgrounds, which has contributed to long-term outperformance compared to benchmark and peers over 1, 3, 5 and 10 years1

Investors should not ignore biotech

Biotechnology is a burgeoning specialist field that is transforming the way diseases are treated. It continues to deliver on R&D pipeline progress and commercial growth despite the macro conditions impacting other, more cyclical sectors. These are the core fundamentals of the expected long-term growth in the sector, and they have arguably been strengthened further during the COVID pandemic.

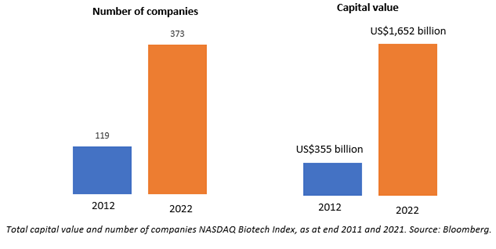

Over the decade from 31 December 2011 to 31 December 2021, the Nasdaq Biotech Index has grown from 119 US-listed biotechnology companies with a combined capitalisation of US$355 billion to 373 companies valued at over US$1.65 trillion (source: Bloomberg). And while the sector remains very US-centric, these statistics exclude similar levels of growth in in Europe and the rapidly emerging China biotech sector.

Figure 1: The biotech sector has expanded rapidly over the last decade

In terms of global equities, the biotechnology sector currently makes up around 10% of the MSCI World Healthcare Index and less than 2% of the MSCI AC World Index and S&P500.

Blossoming subsector, ready for investment

Following a challenging 2021 and going into 2022, with sentiment at lows, it is worth noting that from March onwards the sector has outperformed broader markets. There has been a clear change in sentiment and fundamentals are important for share price moves again, which is good to see.

Companies reporting excellent clinical data updates are being rewarded with large, appropriate share price moves and the ability to recapitalise. Large cap biopharma is taking advantage of some of the excessive share price declines to acquire companies for products and technologies. Commercial companies, meanwhile, are showing that drugs that are needed by patients will be prescribed and paid for irrespective of the macro backdrop.

What is biotech?

Very loosely, biotechnology is the use of living organisms and molecular biology to produce products, typically in the healthcare sector. It is the innovation engine of the biopharma/drugs sector, often sitting at the cutting edge of the next medical breakthrough.

In the early 2000s the sector was very much in its infancy, but since then it has become crucial to the global healthcare industry. The market for pharmaceuticals was once the exclusive domain of large-cap pharmaceutical companies. Today, all of the top-10 global best-selling drugs are derived from biotechnology (biological products and/or developed by biotechnology companies based on 2021 sales). (Source: Fierce Pharma, 31 May 2022).

Increasingly, the distinction between biotechnology companies and their pharmaceutical peers has become less defined. Traditional pharmaceutical companies have acquired biotech assets and then built on the technology bases to harness the innovation intrinsic to the biotechnology sector.

In investment terms, biotechnology is:

- High growth

- Defensive, commercial businesses

- Innovation-led

- Built on strong long-term fundamentals supported by structural shifts in demographics and lifestyles

It has a lower correlation to world equities than healthcare and therefore offers diversification benefits alongside a healthcare fund.

Not just start-ups and high-risk disrupters

Overall, the sector is still weighted towards loss-making, early-stage companies. This is where much of the disruptive innovation is to be found, but it is also the more binary, catalyst-driven part of the sector that many investors can find off-putting.

While these innovators are critical to the long-term growth of the sector, it is important to recognise that there are more developed companies within the sector. In fact, over 80% of the AXA Framlington Biotech Fund is invested in companies that are profitable and/or have commercial assets (as at October 2022). There are also a growing number of high-growth, innovation-driven mid-cap companies with commercial assets and compelling R&D pipeline products.

This mix of defensive top-line growth and pipeline leverage is an attractive area for long-term investment and a focus for the AXA IM’s Biotechnology Fund.

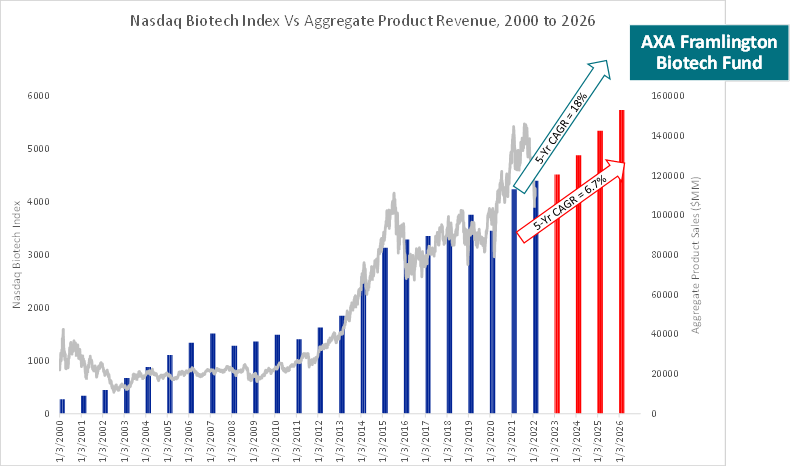

As shown in Figure 2 below, there is a correlation between biotechnology share prices and sales growth over time. The top line growth rate through 2026E for the AXA Framlington Biotech Fund is 15% per annum. This compares to the 7% growth for the wider biotechnology sector, and the 5-6% expected for the broader US and healthcare equity indices.

Figure 2 Sales growth powers returns

Source: AXA IM, Cowen Inc. May 2022. Index shown is price performance, not including income. Capital at risk. Past performance is not a guide to future performance.

Case study: Moderna

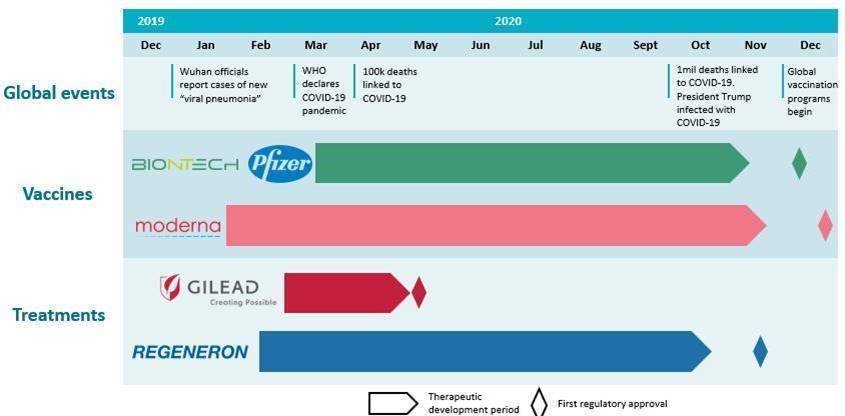

The key characteristics of a biotechnology company are perhaps best illustrated by Moderna, now a household name. Moderna spent years investing in a new technology, mRNA that carries instructions to make different proteins that could help our body fight infections or prevent diseases, with a priority focus on vaccines.

This research put the company at the forefront of COVID vaccine development after the release of the genetic sequence of novel SARS-CoV-2 virus (the underlying cause of COVID) in early 2020. It took just 63 days for Moderna and the US National Institute of Health to design, manufacture, quality test and commence clinical studies of their novel COVID vaccine. Following efficacy and safety read outs from large clinical trials, which exceeded even the most bullish expectations of what a vaccine could deliver, the product was approved for emergency use in the US within the year.

The Lancet Infectious Diseases reported that an estimated 14.4 million deaths from COVID-19 were prevented from December 2020 to December 2021 due to vaccination.2 It was likely the only option for ending the global pandemic and Spikevax was the fourth best-selling pharmaceutical in 2021.

The biotechnology industry is most often thought of in relation to pharmaceuticals. Therefore, it is worth remembering that it is only recently that an internally developed, COVID vaccine has become commercially available from the large, incumbent pharmaceutical vaccine manufacturers.

The adaptability and speed of this new biotechnology combined with the agility and focus of Moderna’s execution set them apart from large pharmaceutical rivals. The vast majority of these pharmaceutical rivals have since acquired or partnered with smaller mRNA biotech expertise to future-proof their businesses.

The AXA Framlington Biotech Fund – combining resources and experience

AXA Framlington has a long history of successfully running dedicated healthcare franchises. The AXA Framlington Biotech Fund was established in 2001 and has £470 million under management within the UK Unit Trust. The Fund has delivered continued long-term outperformance versus benchmark and peers over one year, three years, five years and 10 years, and across many market cycles.

Strong long-term performance

| One year | Three year | Five year | Ten year | |

| AXA Framlington Biotech Fund (Z share GBP, net of fees) | 7.7% | 63.1% | 64.7% | 368.9% |

| Benchmark (NASDAQ Biotechnology Index) | -2.1% | 36.9% | 43.9% | 317.4% |

| Peer group average (EAA Sector Equity Biotechnology) | -10.1% | 20.0% | 21.9% | 233.4% |

Source: AXA IM, Morningstar as at 31/10/2022. Capital at risk. Past performance is not a guide to future performance. Return may increase or decrease as a result of currency fluctuations. Within the peer group, funds are grouped into categories according to their actual investment style, not merely their stated investment objectives, nor their ability to generate a certain level of income. To ensure homogeneous groupings, Morningstar normally allocates funds to categories on the basis of their portfolio holdings. Several portfolios are taken into account to ensure that the fund´s real investment stance is taken into account.

The team manages £1.6bn across all AXA Investment Manager’s global healthcare franchises and sits within the broader global equities team that spans London, China, Singapore, Hong Kong and Paris. This presents a wide resource for sector funds like this.

The managers bring a wealth of dedicated healthcare and biotech experience having a collective 33 years covering the sector.

Lead manager, Linden Thomson has nearly two decades of buy-side and sell-side experience as one of the early specialists within the biotechnology sector. Importantly, our managers also have strong, science-focused academic backgrounds that bring credibility to their analysis of the sector. These include MSc Medical Microbiology (Hons), PhD Biochemistry, MPhil Statistical Science; most recently, Cinney Zhang graduated completed an MBA with a thesis titled The Rise of China’s Biotech Sector: What the Future Holds.

Many managers do not gain significant exposure to this innovative, high-growth sector through generalist US funds or indeed many broader healthcare funds. Within AXA IM, for example, only 27% of stocks held in the AXA Framlington Biotech Fund are held in AXA Framlington Health, and other funds hold less than 14%.

Gaining exposure though a dedicated biotechnology fund run by managers with specialist knowledge is one of the best ways to make the most of current attractive valuations and long-term growth opportunities within the sector.

- U291cmNlOiBBWEEgSU0sIE1vcm5pbmdzdGFyLiBBcyBhdCAzMS8xMC8yMDIyLiBQZWVyIGdyb3VwIGlzIHRoZSBFQUEgU2VjdG9yIEVxdWl0eSBCaW90ZWNobm9sb2d5LCBiZW5jaG1hcmsgaXMgTkFTREFRIEJpb3RlY2hub2xvZ3kgSW5kZXguIENhcGl0YWwgYXQgcmlzay4gUGFzdCBwZXJmb3JtYW5jZSBpcyBub3QgYSBndWlkZSB0byBmdXR1cmUgcGVyZm9ybWFuY2Uu

- U291cmNlOiBMYW5jZXQgSW5mZWN0IERpcyAyMDIyOyAyMjogMTI5M+KAkzMwMi4gUHVibGlzaGVkIE9ubGluZSBKdW5lIDIzLCAyMDIyIGh0dHBzOi8vZG9pLm9yZy8xMC4xMDE2L1MxNDczLTMwOTkoMjIpMDAzMjAtNg==

Not for Retail distribution: This marketing communication is intended exclusively for Professional, Institutional or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

Calendar year performance:

| 2021 | 2020 | 2019 | 2018 | 2017 | |

| Portfolio % | 2.35 | 31.42 | 18.15 | -7.34 | 8.55 |

| Benchmark % | 0.28 | 28.1 | 19.61 | -3.69 | 10.58 |

Source: AXA IM. Past performance is not a reliable indicator of future results. Performance calculations are net of fees, based on the reinvestment of dividends. Benchmark: NASDAQ Biotechnology Index. The index's performance is calculated on the basis of net dividend. Please refer to the factsheet for more information.

Additional risks

- Single Sector Risk: as this Fund is invested in a single sector, the Fund's value will be more closely aligned with the performance of that sector and it may be subject to greater fluctuations in value than more diversified funds.

- Currency Risk: the Fund holds investments denominated in currencies other than the base currency of the Fund. As a result, exchange rate movements may cause the value of investments (and any income received from them) to fall or rise affecting the Fund's value.

Disclaimer

Unless specified all data source: AXA Investment Managers as at 31/5/2022.

Not for Retail distribution: This document is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

Past performance is not a guide to current or future performance, and any performance or return data displayed does not take into account commissions and costs incurred when issuing or redeeming units. The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested. Exchange-rate fluctuations may also affect the value of their investment. Due to this and the initial charge that is usually made, an investment is not usually suitable as a short term holding.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities. The strategies discussed in this document may not be available in your jurisdiction.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate, London EC2N 4AJ. In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.