COVID-19: How a new breed of bonds can help finance the fight

- 12 May 2020 (7 min read)

Executive summary

- The battle against the COVID-19 pandemic will incur a huge cost to the global economy. We anticipate healthcare systems, governments, financial institutions and companies will need hundreds of billions dollars to cope with and recover from the crisis. According to the International Monetary Fund: “the cumulative loss to global GDP over 2020 and 2021 from the pandemiccrisis could be around $9tn, greater than the economies of Japan and Germany, combined 1 .”

- Institutional investors have an important role in the recovery by ensuring availability of and access to financing through capital markets. The challengein this fast-moving crisis is to ensure that capital can flow where and when it is most needed.

- One response to this challenge has been the emergence of COVID-19 bonds. We see the nascent COVID-19 bonds market as a new area for impactful debt issuance, with similarities to green and social bonds. We believe these bonds can help to address the current and future societal challenges of the pandemic.

- AXA IM have already invested approximately €230m2 in COVID-19 bonds to support the fight against the pandemic. We have developed an investment framework which expects transparency from issuers around how proceeds will be used to support their response to the pandemic. We also call for a commitment to outcome and impact measurement. In our view, these bonds could also act to boost the growth of social and sustainability bond issuances.

COVID-19 bonds: what are they?

COVID-19 bonds are a new development in the sustainable bond market. They emerged in response to the spread of coronavirus around the world and the subsequent upheaval in healthcare systems and the wider economy.

In February, Bank of China came to the market with a “COVID-19 impact alleviation social bond”. This was the first of its kind, aimed at preventing and alleviating unemployment stemming from the pandemic. Since the COVID-19 crisis became a global issue, we have seen more issuers launching what we will dub “COVID-19 bonds”.

So far, two main types of COVID-19 bonds have been issued:

- General Purpose bonds (or ordinary operation bonds), as part of a broader COVID-19 response plan by the issuer;

- Use-of-Proceeds bonds, which can be issued under a framework that is aligned with the International Capital Market Association’s (ICMA) Green, Social & Sustainability bonds principles and guidelines (GSSBP) – or a specific COVID-19 response framework.

Regardless of the structure of the transactions, these are aligned with issuers’ willingness to take swift action in fighting the virus and mitigating its negative social and economic impacts. Generally, COVID-19 bonds are issued to:

- Finance or refinance activities that can help with combating the disease – by monitoring, testing and supporting public health services; and/or

- Assist businesses facing adverse economic impacts – by providing support to small and medium-sized enterprises (SMEs) facing cash flow issues for example.

Other activities may be financed through COVID-19 bonds, but we consider these two the principal justifications for urgent action.

AXA IM believes that COVID-19 bonds offer a financing tool to mitigate the adverse impacts of the pandemic and to address the recovery efforts in the aftermath. In line with our strong commitment to long-term sustainable investing3 , we think these instruments should address both current concerns – e.g. maintaining jobs, supporting public health – and broader long-term sustainability challenges. This includes considerations for minimizing the potential for unintended long-term negative consequences from the crisis.

This final point is crucial if we want COVID-19 response bonds to pave the way for a sustainable future – and it comes at a time of reflection about the deeper fallout and consequences of the pandemic from economic, environmental and societal perspectives4 .

The COVID-19 bonds market and its potential evolution

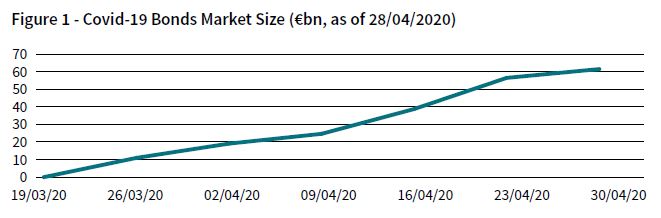

According to data we have collected from various sources5 , as of 28 April 2020, the COVID-19 bonds market had seen issuance worth about €60bn (see Figure 1). These include both General Purpose and Use-of-Proceeds COVID-19 response bonds. Our conservative estimate of the market’s potential size is €100bn outstanding by the end of 2020 – if current issuance rates continue.

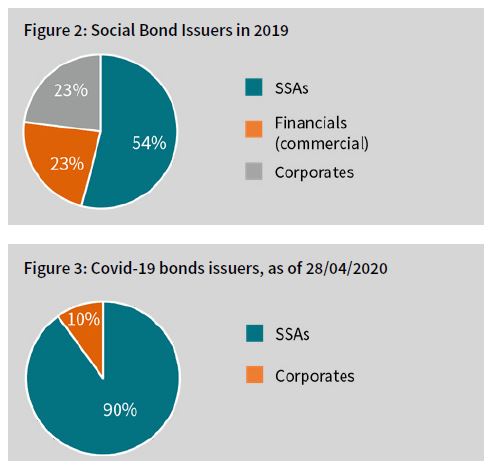

As with the early development of green and social bonds, it is Sovereign, Supranational and Agency (SSA) issuers that have been the main drivers of this market to date. Some corporates also listed deals with COVID-19 related assets as part of sustainability bond frameworks. For projection purposes, we compared COVID-19 bond issuers with social bond market participants in 2019. Issuers which already have a social bond framework in place are more likely to issue COVID-19 bonds – see Figures 2 & 3.

Thus far, financial institution groups (FIG) are missing from the market. We expect them to pick up and contribute to its growth, as some possible hurdles have now been lifted. As an example, ICMA has stated that government-guaranteed loans can be included in COVID-19 bonds issued by banks6 .

AXA IM’s framework on COVID-19 bond investment

We have already invested approximately €230m7 in COVID-19 bonds across our portfolios on behalf of our parent AXA Group and third-party clients. At AXA IM, we will play an active role in shaping and supporting the development of this nascent market. This is in line with our sustainable and impact strategies’ approach, which seeks to deliver measurable effects through our financing activities. In this case, we believe it is important to contribute, through our investments, to the fight against the pandemic.

We support the development of the market but we will, of course, continue to analyse each and every COVID-19 bond issuance – as we do with green and social bonds. We will not simply accept the label at face value; every transaction in response to the pandemic will be studied to assess whether it should be eligible for this kind of investment.

While the primary concern is to protect our analytical credibility and robustness, we also understand that a certain level of flexibility and pragmatism is required in this rapidly evolving market. In order to reflect this, we have developed the following guidelines for investment into COVID-19 bonds:

Use-of-Proceeds bonds: These are the focus of our internal categorization as an “impact bond” – existing green, social and sustainability bonds are Use-of-Proceeds bonds. As such, we apply to the same extent possible the existing analytical process used for green, social or sustainability bonds. We will assess COVID-19 bonds according to the four pillars of AXA IM’s assessment framework8 :

- ESG quality and strategy of the issuer

- Use of proceeds and project selection

- Management of proceeds

- Impact reporting

We have assessed around 500 green, social and sustainability bond issuances over the past few years and, in general, around a fifth are not considered sufficiently credible or robust to merit inclusion. They do not pass our test. Given the scale of this public health emergency and the need for rapid financing solutions to tackle the COVID-19 crisis, we will allow some additional flexibility when assessing COVID-19 Use-of-Proceeds bonds.

We will not expect issuers to publish a detailed framework aligned with the Green and Social Bond Principles if they do not already have one in place. At issuance-level, we nevertheless still require credible approaches to:

- Use of proceeds and project selection: Transparency around the activities to be financed, and details of how vulnerable populations or regions are targeted;

- Impact reporting: Commitment to report outcomes and a stated ambition to assess/measure impact.

In a nutshell, we will focus on the most important criteria to ensure our investment will genuinely help alleviate the negative societal impacts of the outbreak.

These two are the necessary minimum criteria for inclusion in our impact investing strategies. Of course, these commitments can be adjusted over time, depending on the evolution of the crisis and of the related financing needs.

For bonds which are longer-dated, with maturities of more than 10 years, we ask that the issuer provides clarity upfront on what the use of proceeds will be once the COVID-19 related financing is concluded. For example, funds might be assigned to financing wider health-related projects (such as access to medicine) or loans to SMEs. We are assuming in these cases that COVID-19 will not be a long-term crisis and that most related financing will not be needed beyond 10 years.

At issuer level, we still require COVID-19 bonds to be issued by entities with robust sustainability practices and ambitions. We also have expectations that issuers will be open and willing to engage investors in ongoing dialogue on sustainability practices – especially on public health and human capital issues – after the issuance. This way we can ensure that COVID-19 bonds are not only short-term opportunistic instruments, but also fit into the longer-term sustainability strategies of issuers.

General Purpose bonds: These generally fall short of our internal categorization as an “impact bond”. We, nevertheless, acknowledge that in some cases such issuances represent a positive and important response to the crisis. So far, only SSAs have issued General Purpose COVID-19 bonds – but we recognize that other issuer types may follow. The issuers have demonstrated, on the whole, a strong mission to fight the pandemic and address broader sustainability challenges.

For the COVID-19 General Purpose bonds that we will invest in, we are focusing our analysis on the robustness and credibility of the issuer’s broader sustainability practices and reporting. We will focus in particular on any public health or human-capital-related factors and consider whether there has been involvement in any controversies related to these points.

- aHR0cHM6Ly9ibG9ncy5pbWYub3JnLzIwMjAvMDQvMTQvdGhlLWdyZWF0LWxvY2tkb3duLXdvcnN0ZWNvbm9taWMtZG93bnR1cm4tc2luY2UtdGhlLWdyZWF0ZGVwcmVzc2lvbi8=

- QVhBIEludmVzdG1lbnQgTWFuYWdlcnMgYXMgb2YgNCBNYXkgMjAyMA==

- RmluZCBtb3JlIGFib3V0IG91ciBjb21taXRtZW50IHRvIHJlc3BvbnNpYmxlIGludmVzdG1lbnQgaGVyZQ==

- U2VlIEFYQSBSZXNlYXJjaCBGdW5kIEV4cGVydCBTZXJpZXMgZm9yIGluc2lnaHRzIGFuZCB3YXlzIGZvcndhcmQgaW4gcmVzcG9uc2UgdG8gdGhlIGNyaXNpcyBoZXJl

- SFNCQyBHcmVlbiBCb25kIFJlc2VhcmNoLCBOYXRpeGlzIEdyZWVuICZhbXA7IFN1c3RhaW5hYmxlIEh1YiwgTmF0V2VzdCBNYXJrZXRz

- QWRkaXRpb25hbCBRJmFtcDtBIGZvciBTb2NpYWwgQm9uZHMgZm9yIENPVklELTE5LCBJQ01BLCBBcHJpbCAyMDIw

- QVhBIEludmVzdG1lbnQgTWFuYWdlcnMgYXMgb2YgNCBNYXkgMjAyMA==

- RmluZCBtb3JlIGFib3V0IG91ciBncmVlbiBib25kIGFzc2Vzc21lbnQgZnJhbWV3b3JrIGhlcmU=

Not for Retail distribution

This document is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document. Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ. In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.