Coronavirus: How ESG scores signalled resilience in the Q1 market downturn

Key points

- Companies with the highest ESG ratings have proven more resilient in the coronavirus market crash than those with the lowest, AXA IM analysis of stock and bond market in Q1 2020 shows.

- In equities, stocks in the ESG Leaders category outperformed those in ESG Laggards by 16.8 percentage points in Q1.

- In fixed income, bonds in the ESG Leaders category outperformed those in ESG Laggards by 5.2 percentage points in the same period.

- In both asset classes, the ESG Leaders’ basket also outperformed its parent benchmark index.

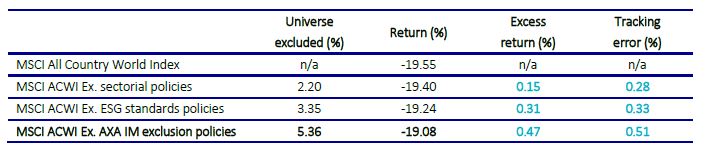

- In a separate analysis, we looked at the impact of our firm-wide investment exclusion policies. We show that a portfolio of stocks which apply our exclusion lists outperformed the parent benchmark index by 47 basis points.

The growth of responsible investment over the past decade has largely coincided with the longest stock market bull-run in history. This has meant that we have not been able to observe how companies with different environmental, social and governance (ESG) ratings perform in a severe market downturn.

The coronavirus pandemic, which originated in Wuhan, China in late 2019, has resulted in a severe and rapid stock market decline. Some of the world’s major equity indices, such as the S&P 500 and FTSE 100, have experienced their worst quarter since 1987. The MSCI All Country World Index (MSCI ACWI), an index of equities from developed and emerging markets, fell by a third from its peak in early February to its quarterly low in late March1.

At the end of the first quarter, we conducted an analysis of how companies with different ESG ratings performed in the bear market for stocks. We also conducted the same analysis for the bond market. We observed that in both asset classes, investments with higher ESG ratings – according to AXA Investment Managers’ in-house ESG quantitative scoring methodology2 –performed notably better and were more resilient in the quarter compared to investments with lower ESG ratings.

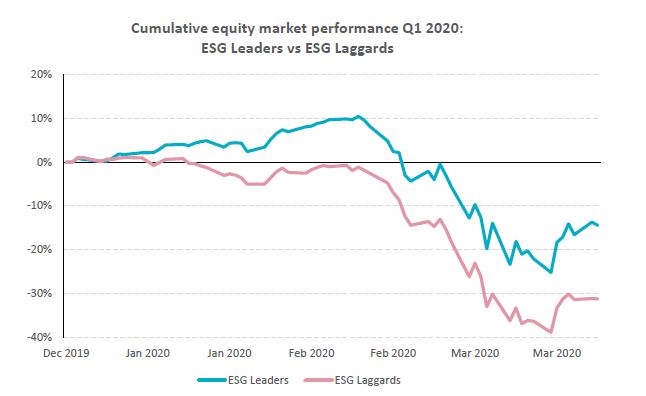

Equity market

A basket of stocks consisting of ESG Leaders outperformed ESG Laggards by 16.8 percentage points in Q1 2020.

For this analysis, we used the MSCI ACWI 3as the base index, and used it to create two sub-groups:

- Stocks with the highest ESG rating (scoring 8 or higher on a 10 point scale) – we dub these the ESG Leaders.

- Stocks with the lowest ESG rating (scoring 2 or lower a 10 point scale) – we dub these the ESG Laggards.

We created two market-capitalization weighted portfolios. The results for Q1 performance were as follows:

The chart below shows the cumulative total return between the two portfolios.

When we delved into performance at the sector-level, we observed that Healthcare, Financials and Utilities had the most

marked differences in returns between ESG Leaders versus Laggards in Q1 2020.

We also conducted a risk analysis and found that the annualised volatility for the parent index, for the ESG Leaders and the ESG

Laggards was largely in the same range.

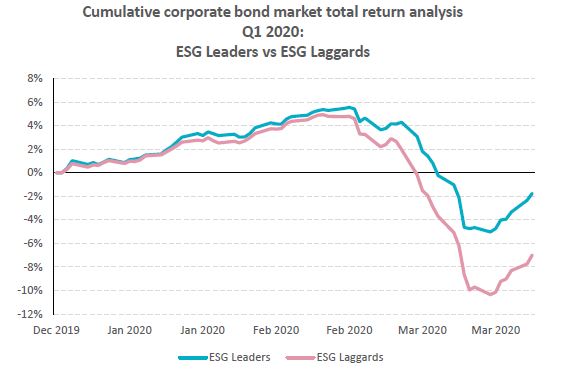

Corporate bond market

A basket of bonds consisting of ESG Leaders outperformed ESG Laggards by 5.2 percentage points in the same period.

We conducted the same analysis for the corporate bond market. We used Bloomberg Barclays Global Corporate Aggregate Bond Index4 as the base index.

We created two issuance-weighted bond portfolios. The results for Q1 total return analysis is as follows:

The chart below shows the cumulative total return between the two portfolios.

When we delved into performance at the sector-level, we found that all of the difference in total return could be attributed to corporate bonds from industrial issuers (corporate issuers excluding utilities and financial institutions). This sector group accounts for more than half of the index weighting. Also, ESG Leaders had lower volatility than the ESG Laggards.

AXA IM Exclusion Policies and Standards – Q1 Update

Earlier this year, we published an analysis of how our various exclusion policies and ESG investment standards at AXA IM had affected our investment returns5 over time. We re-ran the same analysis for Q1 2020. The results showed that our exclusion policies and ESG standards added to investment outperformance. The results were as follows:

We are very conscious that ESG scores cannot tell the whole story in what has been a dramatic time for the global economy. However, our initial analysis seems to show clearly that good ESG scores can be a signal of quality and resilience in tumultuous stock and bond markets. This would suggest that a portfolio skewed to higher ESG scores would offer a more defensive positioning for times of market stress. Further analysis will reveal whether ESG scoring offers similar results as the hoped-for recovery emerges.

- MSCI ACWI – Q1 peak on 12 Feb 2020 to trough on 23 Mar 2020

- For details of AXA IM’s ESG quantitative scoring methodology: https://www.axa-im.com/responsible-investing/framework-and-scoring-methodology

- MSCI All Country World Index, net return, in euro currency unhedged.

- Bloomberg Barclays Global Corporate Aggregate bond index, total return, in euro currency unhedged.

- “How responsible investing standards and policies affect returns” – Mar 2020, AXA Investment Managers.

Not for Retail distribution

This document is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document. Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ. In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.