Sisyphus Happy?

- 26 July 2021 (7 min read)

Key Points

- We review the latest instalment of the “debt ceiling drama”, the spread of the “delta variant” and the ECB’s new forward guidance.

As Macrocast is about to take its usual summer breather, we looked back at what we were writing exactly a year ago: focus was on a pandemic resurgence and political difficulties getting fiscal decisions through in the US. The impression of “déjà vu” is striking. It does not mean that the world economy is not making progress though.

We have no doubt as to the ultimate resolution of this new instalment of the debt ceiling drama in the US. It may take a bit of time – Republicans would relish a “Democrats only” debt ceiling extension which would help them to brand their opponents as spendthrift in the mid-term elections, while Biden’s party will want to show they are being forced to do so to avoid an economic catastrophe – but the market is probably quite blasé about it. Paradoxically, while in principle the dispute should be consistent with a higher risk premium on US federal securities, the suspension of debt issuance for some weeks, adding to the scarcity of US paper chased by massive liquidity, may contribute to keep US yields transitorily lower than what fundamentals would suggest.

Obviously, the spread of the “Delta variant” is a significant risk to the reopening of our economies. However, we take some comfort in the shift towards tailoring restrictions to individuals’ vaccination status. Allowing the continuation of contact-dependent activities for fully vaccinated people would eliminate the need to reinstate blanket prohibitions in key services industries which have been badly hit by the pandemic. Since the beginning, in advanced economies every new wave of the pandemic has been less economically destructive than the previous one. This pattern may not change this time, even if some additional damage is unavoidable.

Still, massive policy support remains needed and from the point of view the ECB’s new forward guidance came out even more dovish than we thought. They promised more of the same for longer with unexpected clarity. A more intense stimulus seems out of question though. The ECB will probably continue to face a “credibility gap” versus the Fed when it comes to delivering on its now more ambitious definition of price stability.

So, yes, policymakers and economic agents at large are still grappling with the same kind of issues 18 months into this pandemic, but in the hope our readers will allow us a non-economic reference, “one must imagine Sisyphus happy”.

Debt ceiling: a twist on the market impact

Senate Republican leader Mitch McConnell did not leave much space for compromise when he stated last Wednesday that “I can't imagine there will be a single Republican voting to raise the debt ceiling after what we've been experiencing”. The debt ceiling had been suspended by the Bipartisan Budget Act of August 2019 until July 31, 2021. If no legislative action occurs, the debt limit will be reset at USD 22trn – the previous ceiling – plus the cumulative borrowing since the beginning of the suspension, in effect forcing the US government to stop borrowing. Janet Yellen has indicated that without a deal in Congress on extending or suspending the debt ceiling again by August 2, the Treasury would be forced to take “extraordinary measures” to avoid a default. Some specific decisions have already been announced: the sales of State and Local Government Series (SLGS) Securities are suspended from July 30th. This programme allows states and municipalities to invest the cash proceeds of their own debt issuance into non-marketable Treasury debt (they are not allowed to engage in “carry trade” by investing in higher-yielding bonds) which counts towards the federal debt ceiling. Still, even after taking on board other measures – e.g., suspending the payments into some federal employees’ pension plan – according to the politically neutral Congress Budget Office (CBO), the federal government would run out of cash by October/November.

Relatively simple institutional solutions exist though to circumvent Republican opposition. A debt ceiling extension could be voted by Democrats only through the “reconciliation process”. It is not obvious however that they would want to move too quickly. The Republicans would relish another extension supported by the Democrats alone as this would give them a strong talking point ahead of the mid-term elections, branding Biden’s party as being overly spendthrift and taking risks with the future of US public finances. The Democrats will want to send the message to public opinion that another debt extension is the only way to avoid an economic catastrophe in the form of a sudden stop in government spending while the economy is recovering from the pandemic, something the opposition is forcing them to do. In other words, some more political drama may be needed before we see a resolution on the issue, even if we have no doubt on a positive outcome ultimately. Yet, this may have some counter-intuitive consequences on the market.

Indeed, a likely delay in extending the debt ceiling is consistent with the treasury drawing further on its cash reserves in the weeks ahead, rather than issuing debt. In principle, a political battle around the debt ceiling should be consistent with a higher risk premium on US sovereign yields. However, investors are probably quite blasé at this stage when it comes to “debt ceiling crises” which have become a recurring feature of the US political life. What may matter more in the short run is that massive existing liquidity will meet scarcer debt issuance, possibly taking yields further down transitorily.

Still, looking ahead, the battle on the debt ceiling does not bode well for progress towards bipartisanship in the US on other crucial fiscal issues. Last week, a procedural vote in the Senate failed amid united opposition from the Republican caucus on advancing on the bi-partisan investment programme pledging USD579bn in additional spending over 8 years, which Biden wants to see enacted together with a Democrats-only social expenditure package worth USD3.5trn. Negotiations are continuing and the resolution may be tabled again as early as this week, but it cannot be ruled out that ultimately the investment programme will need to be tagged to a reconciliation bill as well. A “Democrats-only” infrastructure plan would probably trigger much more spending that the bi-partisan deal currently negotiated, pushing the supply of federal debt higher.

Virus resilience

We have been focusing for some weeks on the “technical factors”, such as the gyrations in the federal government cash reserves, which may help explain the recent correction in US long-term yields. But proper macro factors are also at play and we need to take a hard look at the latest developments on the pandemic front.

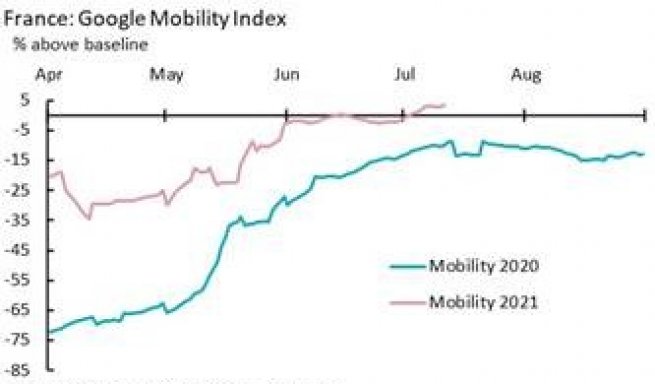

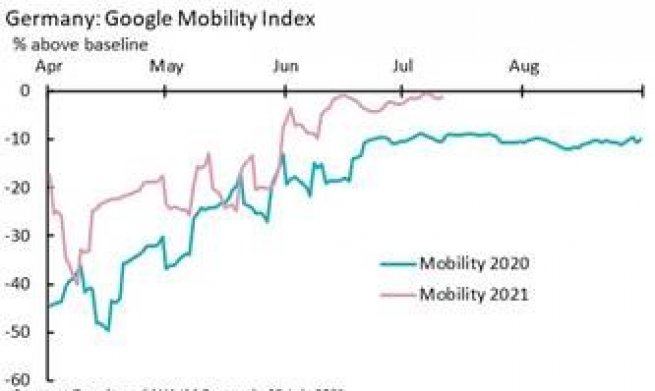

For now, the reopening is still in full swing across most of the developed world. The real-time indicators such as the Google mobility indices suggest that the level of activity is significantly higher than during last year’s “false dawn”. Since the starting point in the spring was less negative, sequential GDP growth between Q2 and Q3 2021 may be less spectacular than in 2020 (see Exhibits 1 and 2) – but over the two quarters taken together, for now it looks like the gains are going to be very strong, unless of course restrictions have to resume.

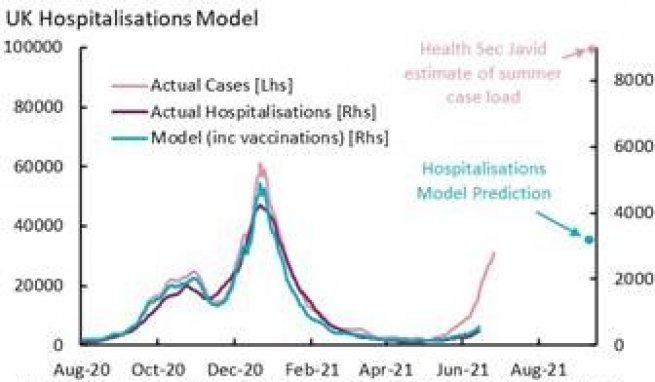

We continue to look to the UK for clues. Habitual readers of Macrocast will know of our modelling attempts, predicting hospitalizations with the number of new cases and the vaccination rate. If we apply this to the UK’s Secretary of Health’s recent estimate of possibly a 100,000-case load by the end of the summer, this would get us to a level of pressure on the healthcare system last seen in February, past the last wave’s peak but still problematic (see Exhibit 3). The latest data from the UK are more encouraging than what the Minister’s estimate implied though, with the beginning of a deceleration in the number of new cases over the last 5 days. Since lately schools had been a key source of new infections and the school year is ending, often ahead of schedule because of the number of children asked to isolate, this may not be surprising. The improvement still needs to be confirmed though, as all restrictions have now been lifted and alternative sources of infection may be emerging.

In most other European countries and in the US the number of infections is accelerating, and in most cases the vaccination rate of the population is lower than in the UK, which would be consistent with even more pressure on their healthcare systems down the road. However, in most advanced economies, every new wave has had a lower impact on economic activity than the previous one. There are good reasons to think the same pattern will apply to this one. A key development there is the beginning of a shift towards tailoring mobility restrictions to vaccination status. This raises all sorts of thorny legal and political issues but allowing the continuation of contact-dependent activities for fully vaccinated people would eliminate the need for blanket prohibitions in key services industries which have been badly hit by the pandemic, a key source of economic damage. France and Italy are clearly taking this route.

It would be impossible to avoid all the adverse effects on the growth trajectory though. Beyond government decisions, the impact of a new wave on activity depends on people behavior, and a measure of “precautionary avoidance”, including by people already fully vaccinated, will likely affect contact-dependent activities. On the supply-side, some level of disruptions is likely to persist, if only as “contact tracing” forces some workers to isolate (in the UK the impact is already visible in key sectors such as retailing and transport). Looking beyond domestic industries, the resurgence of Covid-related concerns in the West should act as a reminder that in many countries, vaccination rates remain too low to seriously dent another wave. This is of course the case in many developing countries, but some advanced nations such as Japan and Australia are in the same situation. This will impair the overall normalization of the world economy and hence global trade.

ECB: more of the same for (much) longer

Given those mounting risks, the need for protracted monetary support remains extremely high. Last week we stated our expectations for the ECB’s Governing Council meeting: some dovish news on forward guidance, with a shift towards an “outcome based” approach and the recognition of the potential need for some inflation overshooting, but nothing on the calibration of the stimulus beyond the PEPP’s current envelope and pace. This is what we had, but with a twist on the “outlook-based” angle: the ECB has clarified its reaction function when it comes to its forecast with a level of details which surprised us. Two issues remain pending in our view: whether the new forward guidance effectively extends to quantitative easing, and not “just” policy rates, and – perhaps more fundamentally – how in practice the ECB is expecting to fill its widening “credibility gap” when it comes to deliver on its new, more ambitious inflation target.

The central part of the “old” version of forward guidance read this way: ““we expect [policy rates] to remain at their present or lower levels until we have seen the inflation outlook robustly converge to a level sufficiently close to, but below, 2 per cent within our projection horizon, and such convergence has been consistently reflected in underlying inflation dynamics”. It now reads: “the council expects the key ECB interest rates to remain at their present or lower levels until it sees inflation reaching two per cent well ahead of the end of its projection horizon and durably for the rest of the projection horizon, and it judges that realized progress in underlying inflation is sufficiently advanced to be consistent with inflation stabilizing at two per cent over the medium term. This may also imply a transitory period in which inflation is moderately above target”. Later during the Q&A, the ECB President made it plain that “well ahead” meant the “mid-point” of their forecasting horizon.

This makes the ECB’s forward guidance significantly more precise, even if the Governing Council will of course retain large discretion. It’s probably easier to explore this with a concrete example. Since the ECB focuses on maintaining price stability “in the medium run” and used to be content with inflation remaining slightly below 2% (without clarity on the “tolerance range”), so far, an inflation forecast at 1.8% even at the very end of their forecast could have warranted a monetary tightening (there is no official position of the ECB on what precisely constitutes the “policy relevant” horizon). In December 2021, the ECB will add 2024 to its forecasting horizon, which means that 2023 will become the “mid-point”. Under the new forward guidance, if in these projections inflation is not at or above 2% in 2023, then the ECB can’t move rates next year. If moreover the inflation forecast is below 2% in 2024, the market would be right to believe that – given the current available information – the earliest the ECB can move (or is “thinking about moving” if one’s suspicious mind considers the forecast as a pure signaling device) is 2025.

The ECB’s discretion now essentially lies in its capacity to move its forecast. Indeed, nothing would stop the central bank from drastically revising up its inflation forecast in March 2022 for instance – we are being purely illustrative here – and upgrade 2023 to 2%, opening the door to hiking rates at some point in 2022. Three caveats there though, on top of the qualitative “judgement call” which Lagarde also mentioned. First, it would not be enough to hit 2% at mid-horizon. Inflation would need to stay there for the remainder of the projection. This will allow the ECB to dismiss “inflation humps” more easily than before. Second, even if the ECB were to maintain inflation above 2% for the remainder of its o forecast, such trajectory could well qualify for the “transitory” inflation overshooting period the ECB may want to tolerate.

Finally, the forecast alone would not be enough. It would have to be “cross-checked” by actual, observed developments in core inflation. In the old version of forward guidance, we interpreted the mention of “underlying inflation dynamics” as code-word for a shift from headline to core inflation in the ECB’s focus, but there was an ambiguity as to when these “dynamics” should materialize, i.e., in observed data or merely in the forecasts. That’s why adding the word “realized” is crucial. It’s not enough to project an acceleration in core inflation. The process will need to have started in earnest before the ECB can move.

The market has responded to the recent signals of the ECB. Forward contracts were consistent with a first hike as early as mid-2023 at the end of June. At the end of last week this had been pushed to the autumn of 2024 (although of course it’s impossible to distinguish the impact of the return of pandemic-related concerns from that of the ECB communication). Still, at this juncture, quantitative easing is by the ECB’s own admission its most effective instrument, and after Lagarde’s press conference, there are some questions on how the new forward guidance applies to QE.

The text itself of the statement is unambiguous. While the key sentence of hitting 2% inflation mentions only policy rates, the ECB in another paragraph has kept its sequencing intact: “The Governing Council continues to expect monthly net asset purchases under the APP to run for as long as necessary to reinforce the accommodative impact of its policy rates, and to end shortly before it starts raising the key ECB interest rates”. Interpretation should then be completely straightforward: if the central bank does not intend to hike rates before 2025 at least, then bond buying would continue for almost as long. However, in her Q&A, Christine Lagarde said “we revisited and revised our forward guidance on ECB interest rates. That's what we did, and our exercise of revisiting it was limited to interest rates”. These two sentences, together with Christine Lagarde’s absolute refusal to engage in discussion on the future of the QE programmes, could signal a readiness to review at some point the “sequencing”.

We suspect this will be the hawks’ main battle in the months and possibly the years ahead. Pierre Wunsch, Governor of the National Bank of Belgium, confirmed in a TV interview that he had voted against the new forward guidance (according to various press reports, Bundesbank President Jens Weidmann also dissented). To precisely quote him, he said “"We might be faced with issues of fiscal dominance, issues of financial dominance, and I just, at the end of the day, did not feel comfortable taking a commitment for five or six years”. Since quantitative easing is the most problematic tool from a “fiscal dominance” point of view, there is probably some significant sensitivity there beyond the small number of hawks who formally objected last week, and Christine Lagarde may have chosen not to dwell too much on the “sequencing” problem in the internal discussions.

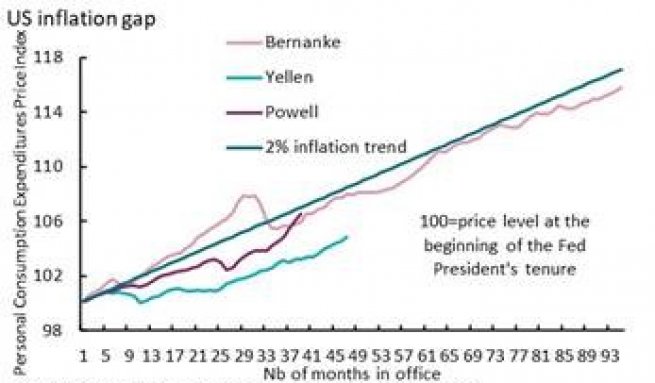

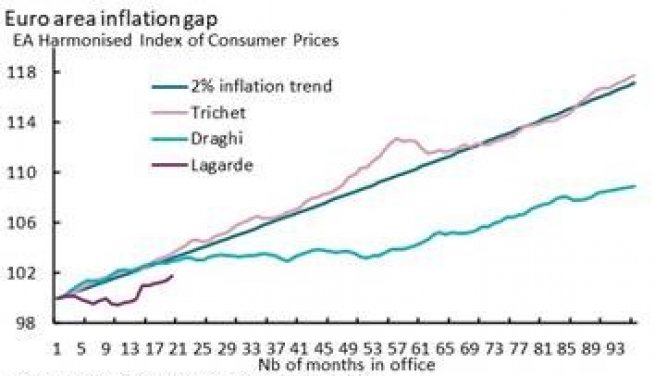

Still, the biggest issue for the ECB under this new forward guidance may well be its now wider credibility gap. Indeed, there is something challenging for a central bank in raising its inflation objective when it has been unable for a very long time to deliver on its old objective in the first place. From this point of view, the comparison with the Fed is unflattering to the ECB. We highlighted last week that in the US, thanks to the ongoing “inflation spike”, the price level gap accumulated since 2012 has shrunk significantly and may have completely disappeared by year-end. While very similar issues are making it more difficult for central banks everywhere to deliver on their target (the decline in the natural interest rate, the possibility inflation has fallen structurally because of technological change etc.…), the Fed has not been far away from still being able to achieve it (see Exhibit 4). For all Draghi’s magic touch, he presided over a very long period of under-delivering (see Exhibit 5)

Two interconnected explanations are usually put forward to explain this European under-performance. First, the possibility that these structural challenges are more acute there, and second that institutional limitations make it more difficult for the ECB than for the Fed to do “whatever it takes” to bring inflation back to 2%. It is indeed highly likely that the Euro area’s equilibrium interest rate is lower than in the US (if only because potential growth is also lower). This puts the ECB more often against the effective lower bound of policy rates, which in theory would force a more frequent and forceful recourse to unconventional policies such as quantitative easing. This is where institutional limitations come into play. For all his conviction more unconventional tools had to be deployed, it took Mario Draghi much time and effort to get the Governing Council to take decisions which unavoidably put the central bank’s practice close to the “outer limits” of the European Treaty. The ECB thus ended up acting “too little, too late”.

As the new ECB President is now dealing with her own price level gap, it is quite clear that the entire policy discussion at the Governing Council is focused on the durability of the current level of stimulus, while any intensification of monetary action is firmly out of scope. This is how we interpret Lagarde’s reference in the Q&A to “steady hands” and insistence on avoiding past mistakes and remove the stimulus too early. More of the same, for longer, but no addition to the arsenal, in all likelihood. This is probably enough to avoid major financial stability issues arising from debt sustainability concerns – sovereign yields will probably continue to get a significant measure of support once PEPP is over – but we would not hold our breath on the ECB’s capacity to deliver on its inflation objective.

One indirect source of support for European inflation, ultimately, may ultimately stem from a growing interest rate differential with the rest of the world when monetary policy starts normalizing outside the Euro area earlier. Indeed, if the Fed ends up removing its stimulus much faster than the ECB, taking most other central banks in its stride, the ensuing euro depreciation could help lift European prices. But we are probably discussing a fairly far away horizon.

Disclaimer

This press release should not be regarded as an offer, solicitation, invitation or recommendation to subscribe for any investment service or product and is provided for information purposes only. No financial decisions should be made on the basis of information provided.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.