Define ”Big”

Key points

- The Commission’s “Next Generation package” is a big step forward, but it’s no proper cyclical stabilization capacity.

- The ECB will have to top up its PEPP. We think they will do it this week already, even amid good news on monetary policy transmission.

- The tension between the US and China will not go away.

The European Commission “doubled down” on the Franco-German initiative and came out with a bigger quantum for its “Next Generation” package and proposals for new “own resources”. This is politically important. While we are still very far from a New Deal moment with the emergence of a proper “federal” budget, progress is undeniable, even if the negotiations will probably be long and noisy.

Still, the Commission’s documents suggest a very slow lift-off. Based on the proposed timeline, Italy would receive only EUR4bn in grants in 2021, less than 0.2% of its GDP. This is puny compared with the severity of the ongoing recession. Totaling 5% of the EU GDP spread over at least 4 years, the “Next Generation” programme is not a massive cyclical stabilization capacity. Beyond the numbers, we were surprised by some of the features of the “allocation formula” offered by Brussels. The scheme looks more like a (much) magnified cohesion fund, repairing the damage of the sovereign crisis of 2011-2012 for the peripherals and bridging the gap with the Eastern countries. This is very important but contributes only marginally to fighting the current downturn. National governments remain very much on the hook, which means that the ECB will have to continue ensuring their financial sustainability. We expect the ECB this week to announce a “top up” to its PEPP which would pass the symbolic bar of 1 trillion euros.

At least the ECB can find comfort in the swift transmission of monetary policy. The data for April confirmed the strength of credit origination for businesses. This is allowing them to continue building large liquidity buffers which will come handy when governments start reducing their direct support – e.g. via in-work unemployment schemes. Households also continued piling up bank deposits. Transmission is however not perfect everywhere. Lending to businesses halted in Italy in April. This may be due to teething problems with the state guarantees but given the specific fragility of this country this warrants close monitoring.

Outside Europe the market continues to take a lot of comfort from small things. The US equity market had a late rally on Friday following a press conference in which President Trump was not as harsh on China as expected. We provide this week some data illustrating how much public opinion hostility to China has risen in the US, across the political divide. This issue will not go away.

Beyond the political signal

The “Next Generation” package presented by the European Commission last week is a very significant breakthrough from a political point of view, which could go a long way in solidifying the monetary union as an institutional construct. Still, we do not think that on its own it can provide enough support to quickly absorb the GDP loss of 2020. National budgets will remain crucial, and this means that the ECB will have to continue for a long while to ensure their financial sustainability, even if this new “federal” capacity can complement them.

Let’s start with the positives. Two key elements sign the ambition of the Commission’s “Next Generation” proposal:

First, the “grant versus loans” issue is deftly dealt with while still nodding to the “frugals”. A new lending facility open to the member states of EUR250bn is created – coming on top of the loans available through the European Stability Mechanism - but this is smaller than the EUR 440bn in grants (non-repayable transfers) to the national governments through various channels, no too far away from the Franco-German initial proposal. The remainder of the EUR 750bn comes in the form of guarantees, following the EU’s habitual fondness for complex financial engineering.

Second, the European Commission wants to take another step towards fiscal federalism by creating new “own resources” which would contribute to the repayment of the debt issued to fund the Recovery and Resilience Fund (the main component of the package). This could take the form of a tax on plastic, a “digital tax” and a border-tax (i.e. introducing a custom levy proportional to the carbon footprint of imports). Creating a central, independent source of income against the new liabilities incurred by the federal government was a key plank in Hamilton’s reforms in the 1790s, as we discussed last week. This would pave the way for leveraging on the pandemic emergency to build up a more significant, permanent “federal budget”. We note however that these last two proposals – the digital tax and the border tax – will probably trigger some very negative reactions from some of the main trading partners of the EU (the US on both and China on the latter).

Still, we see the package more as a very promising fiscal redistribution system – a sort of magnified cohesion fund – which will help within the next 5 years to deal with intra-EU inequalities than as a substantial “recession-busting” fiscal capability.

While in the Commission’s papers the contribution of each country to the repayment of the debt merely follows their share in the EU’s GDP, the allocation key – how the transfers and loans will be apportioned across member states – is the redistribution instrument. We suspect the formula presented in the staff working paper is only an opening gambit, but we find it interesting that it contains no variable representative of the pandemic or of the ongoing contraction in activity. The share of each country would depend on its share in the EU’s total population, controlled for the relative level of its GDP per head (countries with GDP/head above the EU average would receive less money) and for the relative level of unemployment (countries with an unemployment rate above the EU average, over 2015-2019, would receive more money), with some “caps” on the variables to avoid “excessive concentration of resources”. An allocation directly driven by the pandemic shock would have focused on deviations from the GDP and unemployment benchmarks by year-end 2020 for instance.

It so happens – but we suspect the Commission staff has tried quite a few different combinations before getting to this result – that all southern peripheral countries would be net beneficiaries of the system. So would most of the Eastern countries, which we thought could be tempted to block the initiative for fear the new scheme would divert resources from the “traditional” structural funds which remain crucial to them (see Exhibit 1). In a way, we could see this allocation key as a “reparation” for the austerity cure which the peripherals had to go through at the time of the sovereign crisis, while bridging the gap with the Eastern “new members” faster.

Still, some thorny discussions on the “formula” are unavoidable. We were surprised that the Commission chose to rely on headline unemployment, without considering the structural differences across the EU. A “disciplinarian country” could object that while it would make sense to help a member state deal with a bigger than average rise in cyclical jobless numbers, there is little reason to pay for a country where the labour market institutions are conducive to a higher level of structural unemployment.

This may become a particularly sensitive issue in the negotiations if the “frugals” insist on macroeconomic conditionality, for instance to make sure reforms are implemented to reduce structural unemployment. According to the “regulation proposal” put forward by the Commission last week, governments would have to wrap the various projects up for funding in a “Recovery and Resilience plan” in which they would have to show how the intended measures would contribute to dealing with the economic and social consequences of the pandemic crisis, with due respect to the green and digital transitions (article 15). The Commission would have the power to reject those plans, as well as suspending payments if pre-agreed milestones are not met (articles 17 and 19). In our understanding this is a form of “project conditionality” without any direct impact on structural policies in member states nor on their “ordinary” fiscal policy. But it is a fine line. Governments which were very reluctant to take ESM loans precisely because of the macro conditionality they entail will probably want to limit as much as possible the scope of the Commission’s assessment of their plans.

Incidentally, we could not find in the regulation proposal any mention of an appeal procedure to another institution in case of rejection of their plan by the Commission. In the Stability and Growth Pact, ultimately the European Council is the deciding force when it comes to sanctions. Here, the Commission would retain very significant power, since it would be both the payer and the controller of funds’ utilisation. Article 21 only mentions that the Council and the European Parliament would be “informed” of the process. We would expect national governments to object to this – and we note that the “frugal four” are often particularly sensitive to any centralisation of decisions in the EU.

The official reaction of the “frugal four” so far has been “guarded” but there was no straightforward rebuttal – although under the Commission’s proposal they would be the net “losers” of the allocation”. Our view last week was that they could trade their support for the principle of the schemes against a specific rebate on their own financial contribution. The document the Commission issued last week on the Multiannual Financial Framework, which incorporates the “Next Generation” scheme within the overall EU budget strategy over 2021-2027, explicitly mentioned the possibility to maintain such “rebates”.

Assuming the size of the package is not up for negotiation – we think at this stage any back-pedalling on this would send a very negative message to the market – this could entail some redistribution of the frugals’ share towards other “non fragile” member states. It may well be that the two countries who pushed for the initiative in the first place (France and Germany) could have to shoulder even more of the “net payments”. The frugals stand for only 14% of the EU’s GDP and hence their contribution to the debt repayment, but any significant reduction in their payments could test political acceptability in France and Germany.

Too small and too slow

The list of potential bones of contention is long, and it seems the Europeans want to take their time. No decision is expected by the European summit on 19 June. This first delay, followed by the necessary ratifications by the European and the national parliaments – plus the time it would take to prepare the Recovery and Resilience plans at the national level (they could be presented in October according to the Commission’s document) and their assessment by the Commission (up to 4 months) suggest that spending is unlikely to start before next year.

In addition, the funding side of the project is barely sketched out in the Commission’s documents. All we know is that the debt would be issued with a long maturity. For our part we have no real concern about the market’s capacity to absorb this from a highly rated issuer given the current search for duration, but we would welcome differentiated issuance. Since the projects would need to contribute to the green transition, we think it would make sense to “carve out” a green bond out of the new EU debt, given the growing interest for this kind of assets.

Beyond starting the institutional process, the Commission’s document presents a very gradual lift-off of the Fund. The first year, in 2021, only 6% of the grants would be effectively paid. As of 2023 still less than half of all the grants would be paid. As much as we believe the European economy will need long term policy support on its way out of the pandemic shock, we believe the scheme would need to disburse much more quickly than this. To take a precise example, the Commission’s document is consistent with only EUR4bn in grants disbursed to Italy in 2021, i.e. less than 0.2% of its GDP. This is puny when compared with the depth of the current Italian recession.

As per the name of its main component, the initiative pursues two objectives: “recovery” and “resilience”. Given the time it would take to reach cruise speed, we think it is more suited to address the latter than the former. Anyway, the overall size of the package (5% of the EU GDP including the loan component) remains too limited if spread over several years. To use again the historical analogy we mentioned last week, this is not a “New Deal” moment when a federal budget fills the vacuum left by individual states’ incapacity to provide fiscal support. This is a federal redistribution system which will level off some of the asymmetries in the varying fiscal response capacities across member states in the medium term, but they will still need to do the heavy lifting in the coming 18 months.

PEPP needs a top-up

A potential side-effect of the “Next Generation” package is that national governments expecting “federal” resources gradually coming their way would choose to limit their ambitions on their own, “ordinary” fiscal stimulus. We have already noticed outside Germany some hesitation on the quantum of discretionary measures. National governments must be reassured on their domestic financial conditions and this is why massive ECB intervention is still needed.

Although purchases through the Pandemic Emergency Purchase Programme (PEPP) have retreated from the peak at 8.5bn per day at the beginning of May, the latest pace is still consistent with all the EUR750bn being spent by the end of September, while the ECB has pledged to maintain it until at least the end of the year. Mechanically, the ECB would need to “top it up” by at least EUR350-400bn – i.e. to bring it above the symbolic level of 1 trillion euros – to be comfortable until December. Communication from the ECB before they went in “purdah” was very open to such extension. Political economy factors would favour such a move next week already instead of waiting until the July meeting. Indeed, there is no point in delaying decisions to incentivise governments to “do their bit” since the European Commission has already released its project.

Yes, since every time the overall quantum is raised it becomes more difficult to comply with the limits to quantitative easing which the German Constitutional Court has explicitly incorporated in its reasoning, doing it at the first Governing Council since the Court ruling could be seen as provocation, but equally not moving now – while the market consensus has shifted towards a June decision – could be seen as a signal the central bank is sensitive to Karlsruhe’s pressure. We continue to think that signalling that PEPP would be reinvested over a long horizon would be welcome – it would give the central bank more time to re-converge towards the capital key and would be powerful guidance for the market. Finally, we expect for this week a decision on keeping the fallen angels – entities losing their investment grade status – eligible to quantitative easing operations.

An ocean of liquidity

A month ago, in Macrocast we focused on monetary policy transmission in the Euro area and found comfort in the combination of very strong flows of lending to the business sector in March with a majority of banks expressing their intention to loosen credit standards in the near future. It is usually difficult to be less optimistic than your humble servant, but some commentators were pointing out at the time the possibility that the flows were merely reflecting businesses hastily drawing on their existing credit lines before banks closed them. They were thus expecting a “backlash” in the following months.

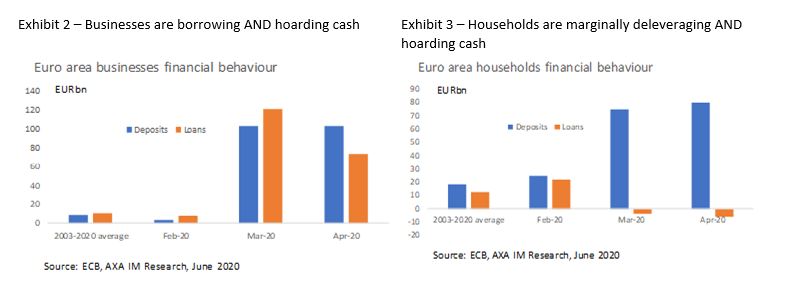

Fortunately, the April data points to the continuation of strong lending flows to the business sector. True, the record of EUR121bn of March was not bested, but the April flow of EUR73bn is still impressive, equivalent to 7 times the monthly average of the last twenty years (see Exhibit 2). Interestingly the flows of ultra-short loans (less than a year) was negative in April, which suggests businesses are not merely drawing on overdraft facilities. Origination of long-term loans (above 5 years) was robust (EUR40bn from EUR35bn in March). This is a positive development, since we are concerned that paying back principal over a too-short period could impair corporate cash flows once the economy exits from lockdown.

The data for April also confirmed that businesses in aggregate are not “burning cash”. Quite the opposite. A lot of this extra lending is hoarded as liquidity, as suggested by the continuation of strong flows of deposits, remaining at the record high of EUR 103bn in April. This probably reflects the success of the fiscal stimulus: the various “in work” unemployment benefit systems in particular have protected the firms’ cash flows, together with the delays offered to pay down tax liabilities.

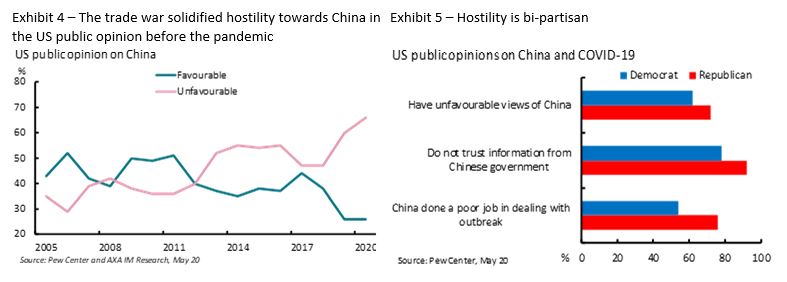

The monetary statistics also confirm that households have accumulated massive cash buffers during the lockdown. They added another EUR80bn to their bank deposits (mostly on their overnight accounts) in April besting the record-breaking EUR75bn in March (see Exhibit 3). This is equivalent to 15% of monthly consumer spending in the Euro area.

Not all this forced saving will find it way to actual spending once the lockdown is completely removed, as the deterioration in labour market prospects will trigger some precautionary behaviour. For now, the labour market is not “flying solo” across the Euro area. State support remains massive, even if some governments – in France for instance – have announced a measure of retrenchment (requesting employers to shoulder a higher share of the furloughed workers’ pay). So far, the rise in unemployment is stemming mainly from short-term contracts not being renewed or newcomers to the labour market failing to secure a job, but the likely wave of lay-offs has yet to come. Still, it is reassuring to face the next critical phase of the pandemic shock from a comfortable liquidity position.

However, monetary policy transmission is not equally swift across the Euro area. Some of the data pertaining to Italy is concerning. We don’t have seasonally adjusted data for country by country data, but the flow in Italy in March (EUR20.3bn, 16.8% of the Euro area total) was completely in line with its share in the Euro area GDP. The flows halted in April (0.4bn), while they accelerated in Spain and remained strong in France and Germany.

We are tempted to attribute the weakness in credit distribution in Italy to difficulties with the state guarantees system there. In principle it is very generous (guarantee of 100% up to EUR30k, 80% up to EUR800k) but banks were slow in originating the loans given the uncertainty in their responsibility in assessing the sustainability of this new debt.

With less access to borrowing, Italian businesses also failed to build up additional liquidity buffers. In April the outstanding level of their cash reserves had risen by only 2.1% relative to their pre-pandemic level, against 14.3% in France. This could impair the speed of the rebound upon exiting the lockdown. From almost every angle, Italy comes out as a specific risk within the Euro area.

US-China tension will not disappear easily

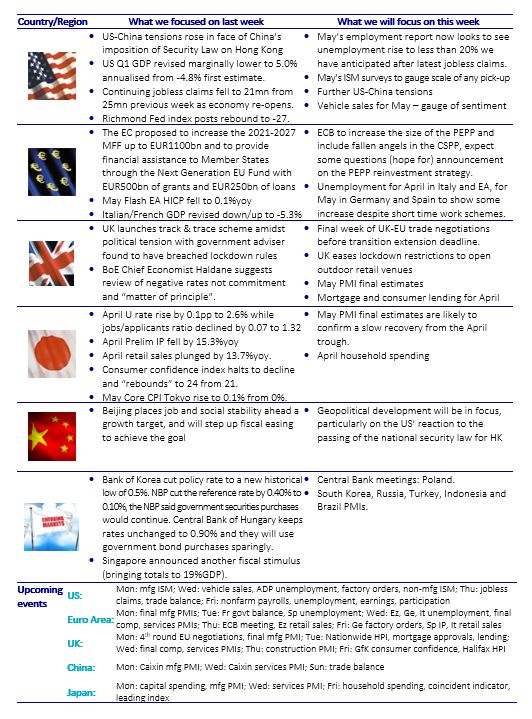

Last Friday the US equity market enjoyed a late rally as President Trump’s press conference was seen as less concerning than expected on the state of the US relationship with China. We would not bet too much on any lasting appeasement on this front though. We find it interesting that the “trade war” in 2019 coincided with a further deterioration in how China is viewed by the American public (see Exhibit 4). It seems that the argument that such policies are mutually detrimental did not bite. The hostility was heightened again in 2020 by the pandemic. But we would focus on the bi-partisan nature of such hostility. Democratic-leaning respondents to the Pew Centre’s poll are only marginally less negative on China than their Republican compatriots (see Exhibit 5). Given the popularity of the theme, we are convinced that “who is going to be tougher on China” is going to feature prominently on the campaign trail in the months ahead.

Not for Retail distribution

This document is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document. Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ. In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.