COVID-19 Update: Labour market deterioration to dampen rebound

Different labour market policies result in different recovery shapes.

Key points

- The labour market could translate the ‘temporary’ COVID-19 shock to a more persistent downturn

- Governments have been alive to this risk and adopted unprecedented measures to support labour markets

- Workers in Europe and Japan appear less likely to lose their jobs, facilitating a swift return to work as economies re-open. US policies should have a similar effect, but uncertainty is higher

- US stimulus should minimise Q2 income losses. In Europe and Japan workers’ pay has been protected, but could be 20% to 30% lower, dampening the consumption rebound

- Uncertainty is highest in China, yet government focus suggests further policy support

- No government can perfectly offset the labour market impact on household incomes and spending. This will weigh on the growth rebound as economies re-open and will require ongoing policy stimulus to overcome.

Gauging the strength of the recovery

In our most recent publication1, we presented a number of real-time metrics which we would use to ground our forecasts in the economic data reality as it emerged. In this note we explain how recent data points to an even sharper deterioration in economic output in the second quarter (Q2) than we had considered just last month. This makes it all the more important to focus on how strong a rebound each economy might enjoy.

With an even steeper drop in economic activity expected in the initial lockdown phase of the crisis, we should naturally expect an even sharper rebound in subsequent quarters. However, beyond the immediate, mechanical expected surge in Q3, the key question is how quickly international economies can be expected to bounce back to their pre-crisis levels, and to reach the level of activity that would have prevailed if growth had not been interrupted in Q1. Also, we consider how different countries might see differing rates of rebound.

A number of factors will be critical. Most important will be the exogenous question of how the virus develops. This must still be treated as an unknown, although in our forecasts we assume a relatively benign scenario. There are then several endogenous factors, including the scale of policy stimulus in different jurisdictions and how indebted private firms will emerge from the shutdowns, influencing future investment behaviour. We will return to these questions in subsequent publications.

In this research note, we focus on how the reaction of the labour market might affect the shape of the recovery via its impact on household incomes and thus consumer spending. We argue that while every downturn begins with an idiosyncratic shock, it is in part how this shock disrupts the labour market that determines its depth and persistence. We consider how labour market reactions are likely to differ across key international economies and how this could influence the shape of individual recoveries.

Labour markets = household income

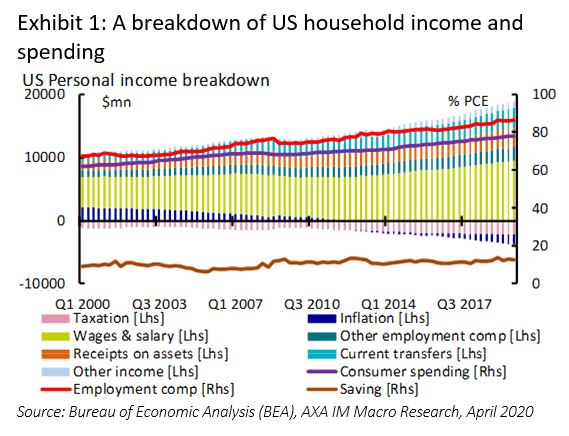

Labour markets are vital to economic activity because they provide the lion’s share of income to households. Below we illustrate this in the context of the US, but the same basic pattern is true across most developed economies. Exhibit 1 shows that, in the US, real compensation from employment constitutes over three-quarters of real income growth and has come to represent about 80% of real consumption – in turn the largest single sector of developed economies at around 70% of US GDP in 2019.

The labour market can affect the economy in two related ways. First, the loss of jobs can translate to a loss of income to households in the deceleration phase of economic activity. This forces households to cut expenditure and/or run down savings/increase borrowing. The former exacerbates the slowdown in economic activity initially, the latter dampens the rebound as households try to rebuild savings or reduce indebtedness even as incomes recover once workers are re-employed.

Second, detachment from the labour force can delay a rebound in consumption. Even as new jobs become available in the recovery, there is time and cost associated with finding new positions. Additionally, workers will often need to work for a period before receiving their first paycheck. Both factors further contribute to a loss of income, which is likely to be reflected in slower spending growth.

When coupled with the heightened uncertainty about future income that job losses entail, the resultant fall in consumer spending can start a demand-multiplier shock, where the initial impact reduces incomes, leading to slower consumer spending, which causes slower growth in other areas of the economy. This is the classic pattern of how a recession develops and persists.

Coronavirus is a special case. While we readily accept uncertainty over how the virus will develop, there is a good chance that most of the economic impact will be temporary and associated with lockdown phases imposed to minimise death tolls in different countries. Take restaurant activity, it all but ceases as an economy goes into lockdown, but it could resume quickly as the sector is allowed to re-open. Hence, government policies around the world have been focused on making sure that firms remain in business during the shutdown and persuading them to keep workers employed over the period to facilitate a swift return to work afterwards.

Governments have therefore pursued two specific objectives with regards to the labour market – to minimise the income loss during the economically inactive phase and to avoid a significant detachment from the labour market. But government policies to address these two goals have differed from economy to economy.

Considering the US

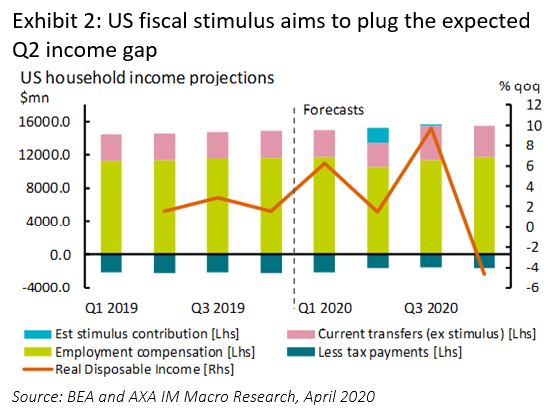

The US government’s response has been the most obvious, in part reflecting the relative lack of automatic fiscal stabilisers2, therefore it required more aggressive discretionary action. As such, the federal government’s $2.7tn fiscal expansion has gone a long way to plugging the hole in household income likely to arise from the drop in activity expected in Q2. The CARES Act included direct pay-outs to individuals ($1200 per adult, $500 per child, costing $250bn in total) and a $600/week unemployment benefits top-up for four months where eligibility has also been extended to the self-employed as well as contract and government workers (costing $260bn). This top-up means that two-thirds of US states (34) now have unemployment benefit that exceed their median wage3. And with 18mn continuing benefit claimants in the past five weeks, this will account for most of the allocated $260bn.

Exhibit 2 shows our estimate of the income effect of job losses of this scale. On our estimates, we forecast total compensation from employment falling by 11% quarter-on-quarter (qoq) in Q2. Unsupported, this would likely have led to consumption falling by around 10%. The exhibit also shows the expected contribution of additional unemployment benefits and direct payments from the CARES Act. These come on top of the usual automatic stabilisers, also observable in expected reduced tax payments in Q2. In combination, we estimate real disposable income to be broadly stable in Q2 compared with the estimated 11%qoq counterfactual. In turn, this should mitigate downward pressure on consumer spending4, and the second-round effect of the initial shock.

US labour market detachment

It is more difficult to assess the scale of labour market detachment in the US. The government has created the Paycheck Protection Program. This scheme allows for loans to small businesses (less than 500 workers) to cover payroll, rents, mortgage interest or utilities costs, but allowing that at least 75% of the loan must be for payroll. The loan is ‘forgiven’ proportionate to the number of employees kept on the payroll, providing an incentive to furlough workers, rather than make them redundant.

So far $659bn, or 3% of GDP, has been allocated to the scheme. An initial $359bn for the scheme was quickly exhausted and, at the time of writing, around half of the subsequent $310bn has been allocated. With at least 75% of these loans going to protect payroll, small businesses should receive around $0.5tn in payroll support. With the loans initially referencing two-months, this would effectively cover the entire 59mn small business workforce at the 2019 median wage rate ($936/week). However, these loans have a salary cap of $100k – more than double the median wage – suggesting the actual number covered is likely to be lower. On the face of it, this would suggest that between 20% and 37% of total US employment is covered by this government scheme.

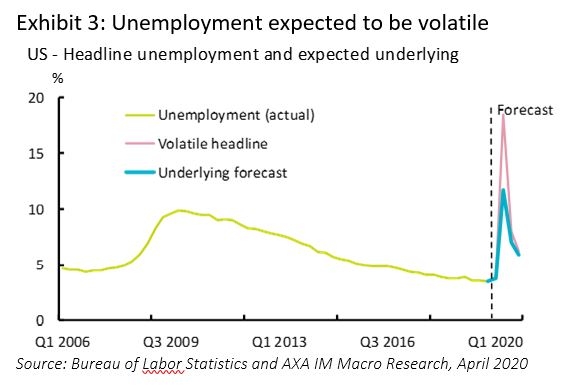

Alongside this, the number of new unemployment benefit claimants topped 30mn in six weeks, with 18m continuously claiming after five weeks. If reflected in overall unemployment, the US jobless rate could approach 20% in May. The US may face large numbers of workers having become detached from the labour market and seeking new employment, risking a second-round consumption impact. Assuming it takes the average worker one quarter to find a new job5, this would result in household incomes contracting sharply in Q3 – as government stimulus is due to recede.

However, a number of points suggest that the current number of jobless claimants could exaggerate the true scale of detachment from the labour force:

- Small businesses may have laid workers off, unsure of their ability to access PPP loans, but may rehire them. The terms of loan forgiveness6 say that companies have until 30 June to restore full-time employment (and salary levels) for any changes made 15 February to 26 April. As such, only workers still unemployed after 30 June should be considered detached. This may account for some of the difference between continuing and cumulative initial jobless claims – that stood at 8.5mn last week – although new job gains could account for around two-thirds of this discrepancy7.

- Larger firms are not covered by the PPP. Large retail firms have been sending workers home without pay. They are eligible for jobless claims, but still effectively employees and in some cases have maintained medical insurance. These workers would be expected to resume work as activity resumes. Bloomberg estimated that more than 1mn workers were involved in such arrangements on 8 April.

A recent Atlanta Fed (FRBA) survey7 suggested over three-quarters of gross staffing reductions were temporary lay-offs or furloughed workers. If these were swiftly ‘re-hired’ this would suggest an overall unemployment rate of around 7.5%, over 10ppt lower than we estimate the peak. Exhibit 3 illustrates a separate approach to estimating the unemployment rate, following Okun’s law8 based on expected changes in GDP. This approach suggests around 12% in Q2 but falling back to 7.5% by the end of Q3. There is significant uncertainty about the true and persistent impact of this shock on the US labour market, but for now we expect a large portion to be short-term lay-offs and not fully detached.

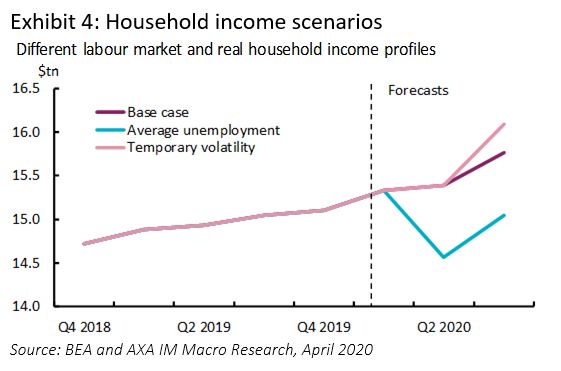

Exhibit 4 illustrates how different employment scenarios translate to household income. If all current claimants were only temporarily unemployed income growth could be sharp in Q3. In our base case, we forecast real income growth flat in Q2, supported by government stimulus, before rising again in Q3 to resume the previous trend expansion. However, if all of those currently claiming were truly “average unemployment” then we would expect real incomes to be 5.5% lower than our base case in Q2 and 4.5% below the base in Q3. Such declines would have a meaningful impact on consumer spending.

China – ensuring job stability takes priority

In China uncertainty over the labour market impact is compounded by the lack of good quality data over time. The well-followed, surveyed unemployment rate only dates back to 2014 and shows a peculiarly modest decline in the latest reading, despite anecdotal evidence pointing to a sharper worsening of labour market conditions.

Based on our estimates of work resumption, we assess that there were 70mn to 80mn people who either lost their jobs or were unable to work due to production shutdowns at the end of March. The majority, at 50mn to 60mn, were likely in consumer-related sectors, such as restaurants, catering, hospitality, wholesale and retail, which together account for about a quarter of all employment in China. The remaining 20mn were likely in construction, industrial and traditional manufacturing sectors where faster work resumption would have helped limit job losses.

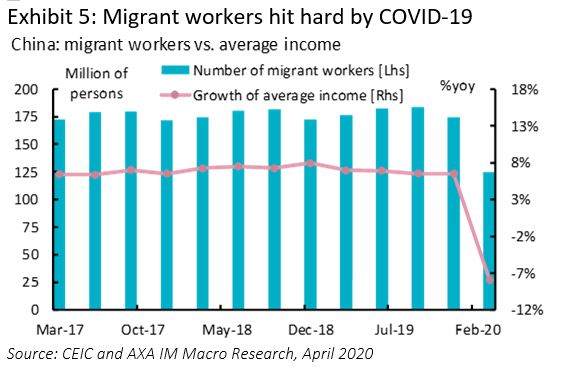

On the supply side, China’s 170mn migrant workers were among the worst hit by the production suspensions in many low-paying jobs. The official data showed that 25mn people who left for home before the lunar new year did not return to work by the end of Q1 (Exhibit 5).

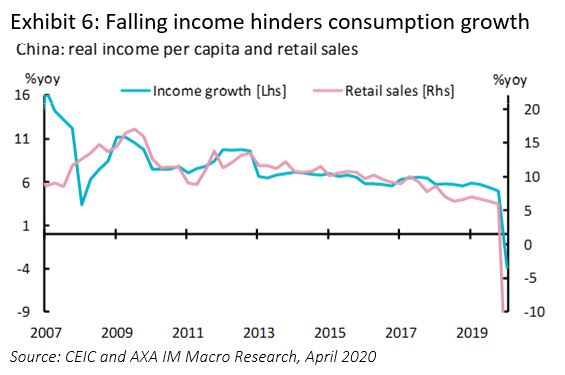

While the economy has recovered from the “sudden stop”, fears of labour market deterioration have not dissipated. Sluggish consumer spending, which is likely to have been exacerbated by the loss of income during the sudden stop, combined with now worsening external demand, are impeding a swift normalisation in the labour market. Given the severity of the anticipated global recession, a 20% fall in China’s export growth, similar to that seen during the global financial crisis, could shave off another 6 to 7mn export-related jobs in Q2, equivalent to 1.5% of urban employment. This is before we consider the multiplier effect of job losses in other trade-related sectors. The sharp contraction in global demand therefore poses considerable risks for prolonging a labour market shock that could hold back the overall economic recovery in the second half (H2) of this year (Exhibit 6).

It is therefore paramount that Beijing acts swiftly and forcefully to prevent permanent scarring in the labour market. Our 2020 growth forecast of 2.3% is consistent with the unemployment rate rising to 8.2% (from 5.2% at end-2019), implying job losses of around 13mn. But even this outcome will require more policy easing than is currently in place.

China has so far been cautious with policy easing – laudable given the cost-and-benefit trade-off of China’s past stimuli. But this is not the time for such frugality. Besides the furloughed migrant workers mentioned above, there are also 8.7mn university graduates expected to enter the job market this year. Without enough work to keep them occupied, a sharp rise in unemployment could create economic instability that could eventually morph into social and political problems. The Politburo – the main policymaking committee – has taken this matter seriously and is now putting “protecting job market stability” ahead of a numerical growth target as this year’s top economic task.

We therefore expect Beijing to announce further and significant policy easing measures at the upcoming National People’s Congress meetings in late May specifically to address rising joblessness. If those policy initiatives fall short of what is required, we would envisage a much more permanent impact on the Chinese labour market and, accordingly, downside risks to our growth forecasts for this and next year.

Eurozone – short-time work protects most jobs

The impact of the coronavirus is affecting each Eurozone economy differently, but the pain of recession and shape of recovery will again be dependent on labour market reactions. Several factors will play in different directions. The economic shock is impacting sectors which are heavily labour-intensive, but Eurozone countries have implemented short-time work schemes to limit the unemployment rise. Still the pain is unlikely to be equal across countries.

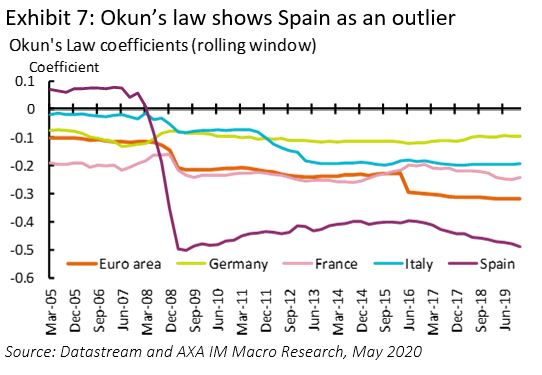

Again, we use Okun’s law as a starting point to consider the unemployment reaction. Analysis across countries suggests significant heterogeneity, with more Spanish labour market sensitivity than its peers (Exhibit 7). A 1% decline in GDP growth translates into a 0.5 percentage point (ppt) increase in the unemployment rate in Spain, against only a 0.1ppt rise in Germany. A rolling regression shows that coefficients vary quite a lot over time, increasing during recession – France, Italy and Spain during the 2008/2009 global financial crisis and Italy during the sovereign debt crisis.

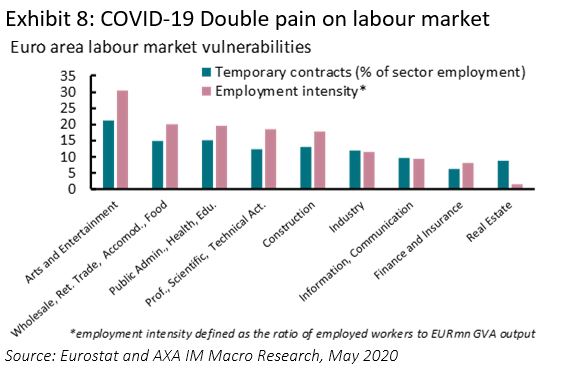

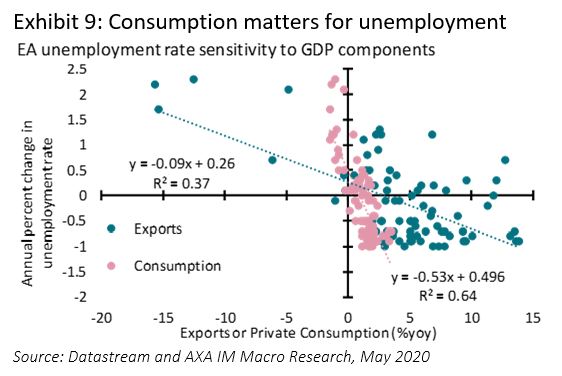

The scale of the labour market effect is also dictated by the composition of the shock, which affects each economy differently. COVID-19 is having the biggest impact on sectors like retail trade, accommodation and food, and art and recreation. These are among the most labour-intensive sectors and see widespread use of temporary contracts (Exhibit 8). This suggests the virus will impact the more labour-intensive and “fragile” sectors the most. This can also be seen in Exhibit 9, which illustrates that Eurozone unemployment is particularly sensitive to movements in the consumption component of GDP, while movements in foreign trade, for instance, have a much lower impact on unemployment – again reflecting the relative make-up of labour intensity in consumer services and manufacturing sectors.

Taking these factors into account, if Eurozone growth contracts by circa 20% in Q2 2020 as we expect, it would theoretically push the unemployment rate above 20% in Q2 (from 7.3% in Q1). However, most countries in the region have adopted or enhanced short-time work schemes, in which the government subsidises a reduction in hours worked or temporary layoffs. We expect these mechanisms to limit large-scale job losses, although country-by-country differences are likely.

A review of short-time working schemes

Germany was one of the first countries to increase access to its well-established Kurzarbeit scheme.

- The threshold for qualification was lowered – to a 10% fall in working hours, from 30%

- Coverage was extended to include temporary agency and fixed-term contract workers

- In addition to compensating 60% of the difference in monthly net earnings due to reduced hours, the labour agency now covers 100% of social-security contributions for lost work hours (from 50% government and 50% employer).

- Wage replacement rates have increased – lifted from 60% to 70% after three months and 80% after seven months until the end of 2020.

- Extended duration is possible to 24 months.

In France, the government has also eased access to chômage partiel. There is no minimum work-time reduction required and the scheme is available to both permanent and temporary workers. Employees receive an allowance of 70% of their gross salary (approximately 84% of their net salary, up to 4.5 times the minimum wage), and 100% for minimum-wage workers. The duration of the scheme has been lengthened from 6 to 12 months.

In Italy, multiple schemes apply to different types of workers, but a range of schemes now means that all firms with at least five employees can apply for some short-time working arrangement with a wage replacement of up to 80%. The long-standing scheme Cassa Integrazione Guadagni (CIG) has been extended to cover workers of smaller firms and more economic sectors with a wage replacement rate of 80% of the last wage for non-worked hours up to a maximum of €1,200 per month, and only permanent contracts are eligible9. There is another scheme, the Wage Integration Fund, a residual solidarity fund, which includes all employers, including those not organized in the form of a company, which employ on average more than five employees and who do not fall within the scope of the CIG. The replacement rate is also 80% of last wage for non-worked hours.

In Spain, the government has extended its relatively new Expedientes de Regulacion de Empleo Temporales (ERTE) which allows companies to temporarily lay-off staff or cut hours, while allowing them to claim unemployment benefits. The process has been shortened to five days, eligibility has been eased (workers no longer need to have worked 360 days in the past six years to qualify for unemployment benefits), and some temporary contracts have been included. The replacement rate begins at 70% of salary for the first six months, dropping to 50% thereafter. Companies triggering ERTE are exempted from 75% of employer social contributions and up to 100% for companies with less than 50 employees, if they maintain the positions for six months once activity is resumed. Here the scheme is tied to the State of Emergency – due to end 26 May – although discussions are underway to “untie” ERTE and extend it until October.

Overall, the French and German systems are particularly attractive with generous replacement rates, long duration and an inclusion of temporary workers. Italian schemes are complex, but available to most firms with at least five employees. Meanwhile we doubt the Spanish ERTE will prevent temporary contract workers from bearing the brunt of the downward adjustment.

How is it working so far? A look at the data

In Germany, the labour agency reported that up to 26 April 751,000 firms had applied to Kurzarbeit, which could represent 10.7mn workers or circa 26% of employees. A total of 3.3mn short-time workers were recorded in Germany during the whole of the global financial crisis. At this stage the size of average working hour reductions per worker is unclear. Assuming short-time workers are on 66% of their normal hours, the shadow unemployment rate would have jumped to 17.5% in April, from 5% before the virus outbreak. In contrast, the unemployment rate rose to “only” 5.8% – some quantification of the size of benefit of this scheme.

In France, the short-time working scheme is relatively new, but the take-up is strong. The labour agency reported that 1.2mn companies (of 3.5mn registered) have applied to chômage partiel as of 28 April. This covers 11.3mn employees – almost one in two employees, with the number of hours worked covered equivalent to 12 full-time working weeks. This means that chômage partiel is preventing a dramatic surge in the unemployment rate to 50% (although in the absence of such a scheme, some companies may not have laid these workers off).

Italy has also seen a record surge in short-time working schemes. As of 3 May, the national statistical institute received 5.4mn cumulative demands, with a total of 12.9mn of covered workers, more than 55% of the total employed. As in Germany, we do not know how large the average working hour reduction is per worker. Assuming short-time workers work two-thirds of their normal hours, the shadow unemployment rate would have jumped to approximately 35%.

There is less data for Spain’s ERTE scheme. The Labour ministry said on 30 April that 3.4mn employees were affected by the scheme, corresponding to some 24% of the affiliates in the General Regime. But labour market data showed the pronounced duality of the Spanish labour market, with a rapid concentration of job losses among temporary employees. In Q1 already (where disruption started only in mid-March) the number of employees with temporary contracts was 2.2% lower on the year, compared with an increase of 2.4% in permanent contracts. The unemployment rate has risen to 17.2% in April, from 15.7% in March and we expect further significant rises in the coming months. We would not exclude that key sectors such as tourism or travel may need to downsize more permanently, limiting these firms’ ability to resort to these short-time schemes.

Participation: Another victim of COVID-19

At the same time, some labour market inactivity is being disguised by people withdrawing from the labour market – falling participation. In Italy, the headline unemployment rate declined to 8.4% in March (from 9.3% in February) as participation dropped (to 64.3% from 65.1%). With the activity lockdown and elevated uncertainty on the future operational environment for businesses, parts of the labour force have been discouraged from seeking work. If this artificially depresses the unemployment rate in the short term, it may have negative medium-term consequences, impairing attachment to the labour market.

Relative labour shortages may also lead to different overall labour market outcomes. Labour shortages have historically been much higher in Germany than other countries, with job vacancy rates at 3.2% in Germany vs 0.9% in Spain. German firms are thus even more likely to keep hold of their employees during the COVID-19 crisis as they know they may face difficulties rehiring later. This a much less pressing factor in Spain.

Overall, we expect the Eurozone unemployment rate to increase to around 11% in 2020, with smaller rises in Germany (7%) and France (11%) than in Italy (14%) and Spain (20%).

Japan – Prioritizing job security

Like Europe, a national consensus has emerged to prioritise job security in Japan, albeit at the expense of wage levels. This suggests Japan may minimise the risks of labour market detachment but could face the consequences of lost income over the coming months. Japan has revived and reinforced the Employment Adjustment Subsidy Program (EASP). The government has loosened the conditions of the programme during this economic downturn to heavily subsidise firms’ costs of temporarily furloughing workers. From 1 April until 30 June, the government:

- lowered the cut-off from drops in production/sales required for businesses to qualify for the program

- expanded coverage to include workers who were not part of the employment insurance (non-regular)

- increased the benefit (subsidy rate) to as high as 90%.

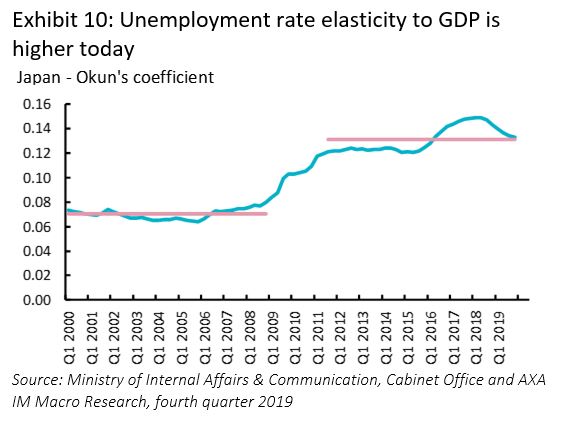

These adjustments to the EASP should help minimise the impact of the expected sharp drop in economic activity on rising joblessness. Looking at the long-run relationship between the change in unemployment and GDP growth (Okun’s law), Exhibit 10 shows that the responsiveness of unemployment to GDP doubled around the time of the 2008/2009 crisis – albeit remaining low overall.

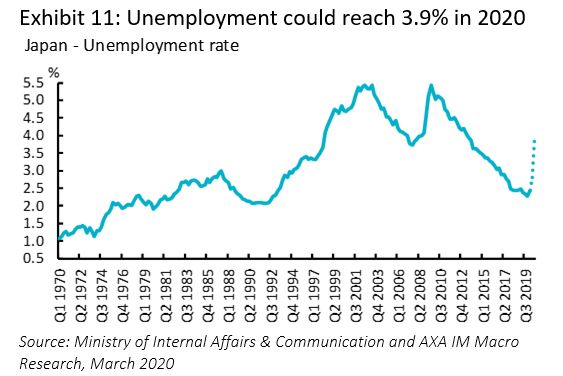

Based on this estimate, we forecast the expected major drop (-10.2%yoy) in Japanese Q2 GDP, should see the unemployment rate rise by 1.5ppt, reaching 3.9% in Q3 2020 (Exhibit 11).

Two additional uncertainties are:

- Responsiveness increased during the GFC and could do again. This presents upside risks to our forecast.

- The long-term trend of labour shortages due to deteriorating demographics may encourage firms to hoard labour. Labour shortages are expected to increase further by approximately 7% over the next 10 years. Forward-looking firms may attempt to hoard labour more now to avoid struggling to rehire workers in the future. This presents downside risks to our forecast.

So, despite a large growth shock, we expect Japanese unemployment to rise by a small amount relative to other international economies. This suggests that the risks of labour detachment in Japan should be relatively limited. However, this looks set to come at the cost of reduced household income in the short-term.

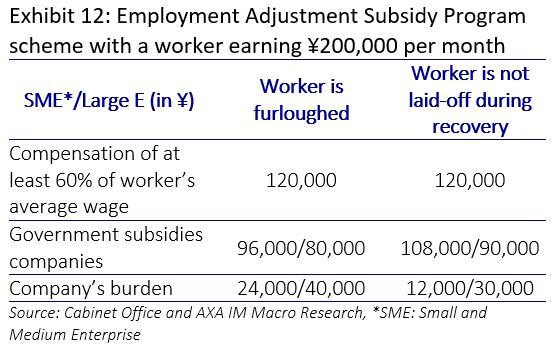

In concrete terms, companies whose monthly production/sales fall by more than 5% year-on-year are eligible to provide 60% of workers’ average wages in compensation to furloughed workers10.

Precisely to mitigate this expected loss in income, the government separately announced that it would make cash payments of ¥100,000 ($940) to all citizens, specifically targeting household’s net loss in income. To put this in context, February’s average total cash earnings across sectors was ¥266,706 ($2,500). Combining the furlough payments and direct cash handouts, on average, furloughed workers should receive 79% of their “usual” income if they return to work after two months (72% if after three months). Households would still stand to lose at least 20% of income over the coming months.

Admittedly the Japanese household saving ratio has risen to 25% in the latest quarter from 12% in mid-2018. This suggests Japanese households have some buffer to smooth income losses. However, preserving income is a necessary, but not sufficient condition for recovery. Consumer confidence will be an important gauge for whether households decide to unwind their savings and revive consumption. The April index is quite worrisome in this regard as it plunged to 21.6, breaking the last lowest point seen in 2009 (27.5).

Job security is clearly Japan’s priority, but one final risk is the corporate sector’s capacity to carry this burden. The EASP scheme comes with a large administrative burden, particularly for SMEs, and a delayed pay-out, estimated at two months. The government is attempting to shorten this delay. Direct cash handouts to SMEs and individual business owners were also part of the latest fiscal package, to mitigate such concerns. However, looking forward, if a negative impact on profitability forces firms to further decrease the burden, they could do so by reducing the hours worked by employees and then laying off less protected part-time workers. This would risk a second-round of unemployment and household income loss, especially in the case of a soft recovery.

What to expect next – a key vulnerability

The labour market is a key channel that could transform a temporary shock into a persistent downturn. We suggest two main risks – income loss during the acute phase of the virus impact, and detachment from the labour market – i.e. genuine unemployment – incurring costs to find new employment as activity recovers. Both threaten to temper consumer spending as the economy recovers, causing a second-round shock to the economy even if the virus fades.

We consider the four largest international economies and find that each has approached these issues differently suggesting different associated risks. In Japan, and to a lesser extent Europe, governments have prioritised job retention. In Japan, we expect the unemployment rate to rise to 3.9% – an enviable rate by international standards – thanks to the Japanese government’s subsidisation of salaries. In Europe, the short-time work scheme practiced in Germany in the financial crisis has presented something of a model across Europe, with many countries following a similar pattern of government support to furloughed workers. These policies should mean workers can return to work relatively quickly once economies re-open.

By contrast, US unemployment looks set to rise towards 20%, but we consider much of this also to be temporary and to mask significant numbers of furloughed workers, which we estimate should see unemployment quickly fall back towards 7.5% as the economy re-opens. However, the large numbers involved provide a greater risk of a more persistent impact. In China, we also see significant uncertainty, based in part on the paucity of labour market data. However, we acknowledge that the Chinese authorities recognise this risk and have made it a top priority, which is likely to see policy specifically aimed at mitigating this risk.

Yet even if we suggest more of a risk in the US from a permanent labour market dislocation, the US also looks most likely to address lost income to households during the lockdown phase of the crisis. Our estimates suggest that income growth across households will be flat in Q2 (in aggregate) and should rebound towards the previous trend rate from Q3. This should underpin solid growth in consumer spending in Q3. By contrast, European workers incomes are being protected at about 80% of previous levels, while in Japan a similar level of protection over two months could soften towards 70% over three. While more likely to remain employed, protected workers in Europe and Japan look likely to suffer from lower incomes in Q2.

Overall, despite unprecedented levels of government support for labour markets, there is still likely to be a deterioration of household income positions in aggregate from lost labour income as a result of this crisis. While households have some capacity to absorb this reduction in the short term, over a period of quarters it is likely to weigh on consumer spending. This suggests a slower pace of growth than would have been the case before the crisis, which will dampen the more mechanical rebound in consumption that will occur as economies ease virus restrictions. This will stop economies recovering previous levels of activity without further policy support, something that we think will continue to call for accommodative monetary and fiscal policy even as global economies re-open.

- Page, D., “The drop in activity, the shape of recovery”, AXA IM Research, 9 April 2020

- Fatas, A. and Mihov, I., “Fiscal policy as a Stabilsation Tool”, Insead, 2016.

- “How unemployment benefit works”, Morgan Stanley, 1 April 2020.

- In fact, the process is likely to be more complicated. Consumer spending in Q2 is likely to be held down by store closures and enforced stay-at-home policies. In the short term, if incomes remain stable in Q2 as we expect, the savings rate should surge as households are unable to spend this income. This increased saving should then be spent in the subsequent quarters, lifting activity in these quarters.

- This is less than the average historical spell of 1.5 quarters, cited in Carroll, C., Crawley, E., Slacalek, J. and White, M., “Modelling the Consumption Response to the CARES Act”, April 2020, Journal of Economic Literature, which we assume to allow for the assumed temporary nature of lockdown.

- “PPP Information Sheet: Borrowers”, US Treasury, March 2020

- Altig, D. and Robertson, J., “COVID 19 Caused 3 new hires for every 10 Layoffs”, Federal Reserve Bank of Atlanta (FRBA), 1 May 2020.

- Okun’s law establishes the link between changes in unemployment rates and GDP growth.

- The duration can be up to 12 months for the CIG Ordinaria (CIGO) and 30 months for the the CIG Straodinaria (CIGS).

- The government will subsidize 80% of the cost of compensation for SMEs (two-thirds for large corporates). For companies that do not make workers redundant, subsidies will account for 90% for SMEs and 75% for large corporates. The subsidy is capped at ¥8330 per employee per day.

Not for Retail distribution

This document is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document. Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ. In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.