China: Fuelling recovery with an extra policy kick

Key points

- COVID-19 has dealt a serious blow to China’s economy and forced Beijing to substantially change its economic plans at this year’s National People’s Congress. The latter includes prioritising job stability over a growth target and radically changing its macro policies by introducing the largest stimulus package since the global financial crisis

- We estimate the explicitly-announced stimulus measures to be worth 4.2% of GDP. But once off-balance sheet resources are accounted for, the total fiscal firepower could reach 5-6% of GDP and be implemented through tax cuts, fee reductions and infrastructure investment

- The language describing monetary policy was kept intentionally vague to give the central bank operational flexibility. While a GFC-style aggressive stimulus was ruled out, the central bank still has ample policy room to play an instrumental role in the economic rescue

- Given our base-line assumptions, including no major virus relapse and a recovering global economy starting Q3, we think the proposed stimuli are sufficient to keep full year growth at around 2%. However, the risks around these assumptions are large, and given Beijing is data-dependent, the eventual stimulus package could be larger – or smaller – than meets the eye.

Two key messages from the NPC

As part of our ongoing series considering international policy responses and their effectiveness during the COVID-19 pandemic, we consider the implications of China’s latest policy announcements at this year’s National People’s Congress (NPC). We will break down the announced NPC policy measures, quantify their economic impacts and discuss how they will be implemented and financed, before giving our overall assessment on whether they will be sufficient to achieve economic growth this year. This follows a similar assessment of US policy stimulus1.

The annual NPC took place as China emerged from the ravages of COVID-19. The pandemic delayed this year’s event by more than two months, shortened the duration of meetings and changed the format of interactions, with all press conferences conducted via live streaming to minimise human contact. Besides the logistical changes, COVID-19 also created extraordinary uncertainties for Beijing’s economic plans. Never before had market expectations been so diverged and uncoordinated on even basic issues like whether Beijing would set a growth target, or if the fiscal deficit would exceed 3% of GDP.

We summarise the key policy signals from the week-long event in two messages. First, Beijing has placed job and social stability ahead of an explicit growth target as this year’s economic priority. Indeed, the decades-long tradition of setting an annual growth target was abandoned and replaced by a more flexible, but less quantifiable, objective of preserving stability in areas like employment and people’s basic livelihood. While this is different from our earlier expectation, we do acknowledge the pragmatism embedded in these objectives in the face of extraordinary uncertainties.

However, not announcing a growth target does not mean the authorities will accept any growth rate. To achieve the “Six Stabilities” – particularly those of creating nine million jobs and keeping the unemployment rate at around 6% – will require the economy to grow as indicated by Premier Li Keqiang. Accomplishing this, when the rest of the global economy is expected to contract at its fastest rate in over six decades, will not be easy. But Beijing – as per the second message from the NPC – seems prepared to provide the necessary backstop to get the recovery – already in motion since February – on a sustainable track.

How big is the stimulus?

There are three main categories of policy tools that constitute Beijing’s economic toolkit. Besides the usual fiscal and monetary instruments, housing market policy often plays a critical role in providing a counter-cyclical buffer to the economy. In this year’s work report, Premier Li reiterated the existing policy line of “housing is for living, not for speculation”, but offered some flexibility for local governments to fine-tune policies to suit local needs. Given the notable pick-up in activity since March, we do not think a wholesale relaxation of the existing housing market curb is likely any time soon. But the sector should benefit from the spillover effects of easier monetary conditions and accelerated urbanisation, where Beijing has set an explicit target for hukou2 conversions in different tiers of cities. The latter, coupled with continued “old town” renovation, should support land sales and housing construction this year.

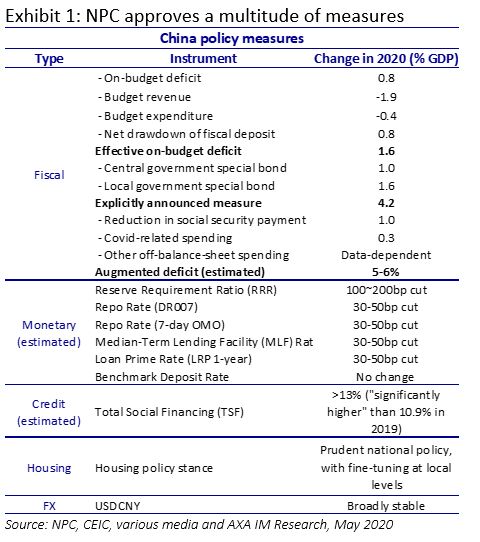

A bigger focus at the NPC was on fiscal policy. This had been less active than in many other countries, with stimulus also small by China’s own historic standards. To catch up, a multitude of easing measures were announced by different policy departments, consisting of a higher on-budget deficit (at least 3.6% of GDP), RMB1tn worth of central government special bond issuance, and an RMB1.6tn increase in the local government special bond quota, to RMB 3.75tn. In addition, the budget announcement also contained a transfer from fiscal reserves, worth 0.8% of GDP, to finance extra government spending. Taken together, we estimate the total announced fiscal package to be worth 4.2% of GDP (Exhibit 1).

In reality, however, we think that even this will likely represent the floor of the growth support from the public sector. Besides the announced measures, there are plenty of off-balance sheet resources that are likely to be tapped to boost spending further. These could include lending by policy banks, investment by local government funding vehicles (LGFVs), spending financed by land sales, and activities of major government-owned enterprises, such as China Rail Corporation. During normal times, these entities behave in accordance with market forces, but in times of crisis, they can serve as effective quasi-fiscal tools for Beijing to ramp up spending. The lack of explicit guidance on these activities affords Beijing some flexibility to adjust the eventual size of policy stimulus. We think the overall fiscal impulse, taking into account both on- and off-balance sheet resources, could reach 5-6% of GDP. This will be larger than the stimulus in 2015-16 – which was around 2% of GDP – but pales in comparison to that implemented during the global financial crisis at more than 10% of GDP.

The language describing monetary policy was kept intentionally vague, with no numerical targets. While the Premier’s work report reiterated the overall policy stance as “prudent”, the two added words “flexible” and “appropriate” suggest there is leeway for the People’s Bank of China (PBoC) to adjust policy according to evolving macro conditions. The report indeed called for further reductions in the reserve requirement ratio (RRR) and interest rates to lower funding cost, and projected money supply and credit growth to be “significantly higher” than those of 2019. The PBoC heeded the call last week for “creating new policy instruments” by introducing two new facilities to aid credit supply to median, small and micro businesses, similar to the Federal Reserve’s Main Street Lending Program1. We think the role of monetary policy will not simply be to finance government spending, but to act as an independent source of stimulus that works in tandem with fiscal policy.

How will the stimulus be spent?

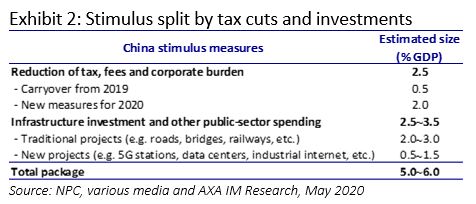

Despite lacking concrete details, we think the proposed stimulus package will be evenly split between tax/fee cuts for businesses and workers, and infrastructure investment, supporting urbanisation and technology upgrade for the real economy.

Beijing has earmarked RMB2.5tn (circa 2.5% of GDP) for tax and fee reductions this year. Roughly RMB500bn of this is carried over from tax cuts in 2019 (Exhibit 2), while the rest are new measures to be delivered through:

- A Value-Added Tax (VAT) rate cut to 1% from 3% on taxable sales revenue for small taxpayers until the end of 2020

- Exemptions of corporate social security contributions for micro, small and medium sized enterprises until the end of 2020

- VAT exemptions for public transport, catering, accommodation, tourism, entertainment, cultural, and sports services until the end of 2020

- Delay in collection of income tax for small and micro businesses and self-employed individuals until 2021.

The second leg of the fiscal push will be delivered in increased infrastructure investment. We think the vast majority of special local government bonds will be used for this purpose, while a portion of the central government bond issuance could be called upon for support too. Once the added resources from LGFVs are accounted for, the total funding for infrastructure investment could top RMB5tn, equivalent to a RMB2tn increase – or 2% of GDP – from 2019.

Compared to past investment spurs, we expect some novel aspects in the current operation. The first is a stronger push for public and private partnership (PPP) in projects that present clear commercial prospects. The head of the National Development and Reform Commission (NDRC) encouraged local governments to fully leverage the flexibility of using special bonds as equity seeds to draw in private-sector capital to amplify the stimulus power of fiscal resources.

A critical determinant of PPP success is the nature of the investment projects involved. For traditional public projects, such as roads and bridges, whose future profitability is either unclear or weak, getting “pure” private-sector investors (i.e. non-state-owned enterprises) interested to co-invest has been a struggle. But with new infrastructure, we think Beijing stands a better chance of success. According to the NDRC, a sizable portion of this year’s fiscal resources will be spent on building digital and high-tech infrastructure, including 5G stations, industrial internet, big data centres and “urbanisation-related” projects to create smarter cities. To the extent that Beijing is successful in combining public and private capital, the eventual stimulus impact could be a multiple of the initial fiscal outlay.

How will the stimulus be financed?

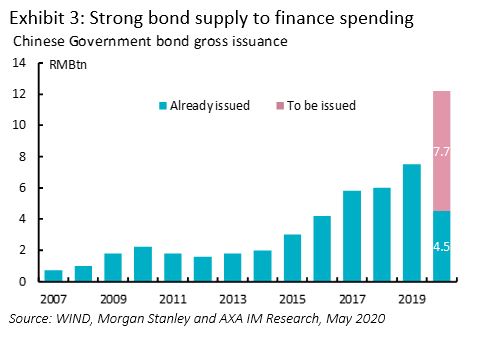

The combined tax cuts and infrastructure spending could push total government bond supply above RMB12tn in 2020 (Exhibit 3): Strong bond supply to finance spending). Bond issuance had already picked up prior to the NPC, as almost RMB3tn of the local government bond quota was frontloaded, putting some upward pressure on bond yields.

We think that digesting this bond supply will not be difficult but will require careful coordination from the central bank to keep liquidity ample. With the PBoC ruling out buying government bonds directly in the primary market, it will need to create enough incentives for banks, which hold two-thirds of all government paper, to pick up the slack. We expect at least another 100 basis point (bp) RRR cut in the remainder of this year, coupled with a 30-50bp reduction to interest rates (Exhibit 1). Our base-case does not anticipate a benchmark deposit rate cut, but such a move cannot be ruled out if growth and inflation surprise to the downside.

Increased foreign interests in Chinese government bonds (CGBs) can also help digest the CGB supply. Official data show that foreign holdings of CGBs rose to RMB1.39tn in April, accounting for 8.5% of the market. Rather than interrupted by the pandemic, foreign inflows to the onshore market have remained strong this year, supported by index inclusion – most recently into the JP Morgan Emerging Market Index – and continued market liberalisation, with a recent move being the removal of the QFII/RQFII3 quotas. Favourable valuation also makes CGBs attractive, in comparison to US Treasuries and German bunds, with currency-hedged yield premiums at 90bps and 300bps respectively at the time of writing. Barring any major disruption to capital flows (e.g. the US prohibiting investment in Chinese bonds as they have done so against Chinese equities), we think foreign holdings in CGBs could rise above 10% of the market by the end of the year.

Will the stimulus be enough?

A total stimulus package worth 5-6% of GDP is clearly not for a garden-variety economic downturn. Yet Beijing has also stuck to its words of not engaging in “flood-like” stimulus having endured the painful adjustments following its “RMB four-trillion” stimulus after the GFC. A more realistic and pragmatic package has been introduced, suggesting that the Chinese leaders are ready to face the consequences of record-low economic growth and a miss to their decade-long target of doubling GDP between 2010 and 2020.

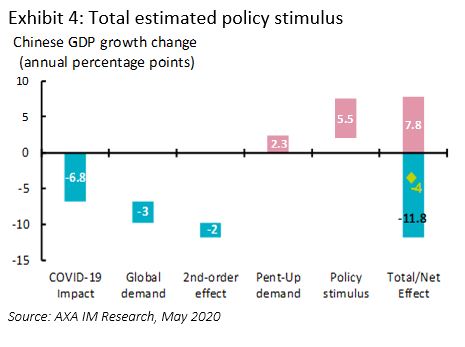

However, as discussed before, fulfilling Beijing’s stability objectives will likely still require the economy to grow, while the rest of the global economy is expected to contract. This begs a natural question: “Is the proposed package enough for the job?”. This is difficult to quantify, but a bottom-up analysis begins to answer this question (Exhibit 4) shows the key positive and negative growth drivers, and our estimates of their impacts.

To the downside, we have:

- The COVID-19 pandemic causing a 6.8 percentage point (ppt) growth decline, as seen in the first quarter

- An external demand shock cutting annual growth by 3ppt4

- An estimated second-order impact worth 2ppt of GDP5.

- Counter-balancing the negatives:

- pent-up demand, which assumes one-third of COVID-19-induced output loss will be recouped

- and an estimated stimulus boost to GDP worth 5.5ppt.

Aggregating these items, we derive a net GDP impact of -4%, which implies this year’s growth at 2.1%, down from last year’s 6.1%. This is very close to our current growth projection of 2.3% and within a range that we believe is the implicit growth target of Beijing at 2-3%.

The above estimates are subject to extraordinary uncertainties. There are plenty of macro risks – such as a relapse of the virus, worsening external demand and escalating Sino-US tensions – that could upset the delicate balances, leading Beijing to recalibrate its economic operations. The NPC has therefore not cleared all the cloud over China’s policy outlook. And as the only counterbalancing force against powerful economic headwinds, close monitoring of the efficacy of these policy operations will be needed to assess the future path of the economy.

- Page, D., “COVID-19 Update: US policy response”, AXA IM Research, 3 June 2020

- Formal permission granted to urban residents that entitle them to social welfares offered by cities. Beijing reportedly aims to grant 100m citizenships (hukou) to migrant workers this year.

- Qualified Foreign Institutional Investor/Renminbi Qualified Foreign Institutional Investor programmes

- Assuming gross export contract by 20% this year, with value-added exports at 14% of GDP, the GDP impact is 20%*14%=3%.

- This is arguably a highly uncertain estimation. The eventual size of the second order impact, even it is measurable, will be contingent on the speed and quality of the economic recovery, which is in turn significantly influenced by the efficacy of the policy easing.

Not for Retail distribution

This document is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document. Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ. In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.