2022 emerging market elections: The who’s who and the so what…

As democratic systems have been put in place across developing countries, investors have had to become increasingly vigilant around political events – especially elections and referendums. In many emerging markets, election years have coincided with a boost in fiscal spending, which has often led to a significant deterioration of already fragile fiscal positions. This in turn has increased dependency on foreign financing which, exacerbated by an acceleration of foreign capital outflows, can put further pressure on currencies and bond yields. Inevitably, a lot of developing country crises have occurred in sync with political cycles. However, as emerging markets see democratic traditions mature, financial and political cycles have decoupled somewhat, thanks to the improved quality of the fiscal and monetary framework.

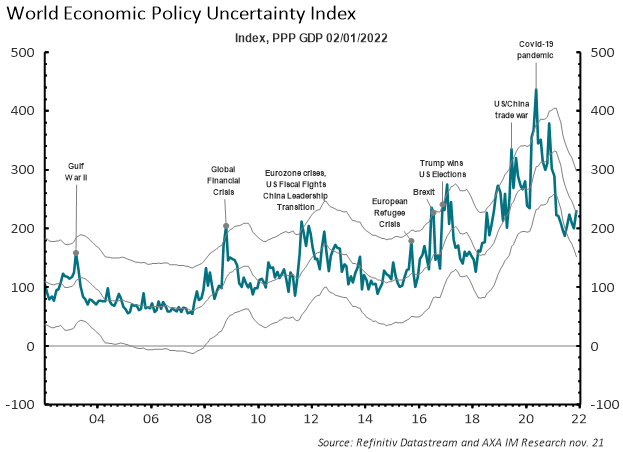

Exhibit 1: Politics and policies in focus

Since 2008, market sensitivity to politics has nevertheless increased, particularly in advanced economies, as highlighted by events such as the European sovereign debt crisis, the Brexit referendum and trade wars. Moreover, the ongoing COVID-19 pandemic has caused significant policy uncertainty across the globe. It has also likely exacerbated inequality and poverty, with lower-skilled workers most affected and poverty increased substantially in low-income countries with weak social safety nets. Poverty, income inequality and demographics make poll outcomes more difficult to predict and give populist candidates a stronger hand. Political volatility is thus again increasingly evident in emerging markets where voters can move decisively away from political incumbents. Such a reversal occurred unexpectedly in Zambia last year when opposition party leader Hakainde Hichilema scored a landslide victory over President Edgar Lungu with an unprecedented voter turnout.

This year several African countries, including Angola and Kenya, will go to the polls and the results could alter political and policy trajectories. Potentially controversial elections also loom in Latin America, with Brazil, Colombia and Costa Rica all going to the polls while Chile will hold a plebiscite on a new Constitution. In Asia, elections in the Philippines need to be monitored for shifting policy direction. In Europe, Serbia has an important electoral year, while populist Hungarian President Viktor Orbán may face defeat after 12 years in power. Given the current backdrop, one thing is certain – no matter who takes office, the economic, social and political challenges have increased in the post-pandemic world.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

Risk warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.