Euro area flash: Q1 GDP and April HICP

Euro area "flash" Q1 GDP slowdown, subdued path ahead

- Euro area GDP growth slowed down 0.1ppt to +0.2% q/q in Q1 22 coming in between ours and consensus expectation.

- We draw from countries' press releases that growth slowdown mainly comes from restrictive measures against Omicron wave affecting private consumption in France and Spain and negative external trade contributions in Germany and Italy.

- Euro area GDP is 0.4% above pre crisis levels in Q1. Country releases highlight ongoing meaningfully better growth performance in France while Spain is still lagging against pre-pandemic levels.

- Beyond a possible upside from services in the short-term, latest business cycle surveys are consistent with our below consensus growth forecast, displaying very limited positive momentum on a sequential basis on average this year. We project euro area growth to slow down to 2.1% this year - same as 2022 carry over - after 5.4% in 2021.

Euro area "flash" GDP growth slowed down to 0.2% q/q (0.189% at 3 decimal places) in Q1 22 from 0.3% q/q coming in between our forecast (0.1% q/q) and consensus expectations (0.3% q/q), consistent with GDP level 0.4% above pre pandemic levels (Q4 19). Owing to a strong H2 21, carry over for this year is at 2.1%.

Although there is no subcomponent breakdown by Eurostat, we gather from detailed releases in France and Spain that Q1 slowdown mainly came from private consumption affected by pandemic related restrictive measures, while high level qualitative comments by German and Italian statistical agencies suggest negative trade contribution at the heart of the activity slow down.

France remains top spot among the large euro area economies with GDP 1% above pre pandemic levels (Q4 19), while Italy is trailing 0.4% below pre crisis levels, Germany 0.9% below, and Spain lagging 3.5%.

Worrisome outlook despite possible upside in Q2. We maintain our baseline of subdued growth outlook, projecting flat sequential growth in Q2-Q3 before reaccelerating from Q4 22 onwards. Sharp deterioration in consumer confidence up to April concurs with our baseline that private consumption is likely to be severely affected by high inflation and economic uncertainty in the wake of the Ukraine crisis. Surprisingly good resilience of services surveys supported by the lifting of pandemic-related restrictions may generate upside surprise in Q2 to our current baseline (-0.1% q/q). However, we think it is unlikely to be more than a temporary offset to material slowdown in manufacturing activity likely to translate into contracting investment adding to households real income squeeze unseen since 2012 (c.-2%). Furthermore, concern on China growth outlook adds to the uncertain and worrying picture, especially for Germany. All in, while we acknowledge some upside risks against our Q2 forecast (-0.1% q/q), we remain comfortable with our below consensus projecting euro area growth to average 2.1%/1.2% this year and next (consensus: 2.8%/2.4%).

Market reaction. Flash estimate coming close to consensus expectation did not yield any meaningful market reaction.

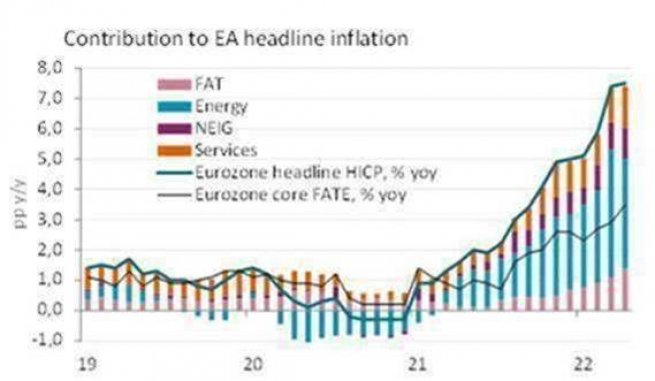

Euro area preliminary HICP inched higher to 7.5% year on year despite lower energy prices

- Eurozone April preliminary HICP headline came at 7.5% yoy, up by 0.1 percentage point from March

- Energy contribution is gradually replaced by food prices (6.4% yoy, +1.4ppt) and core in which pressures are also building up via service prices (3.3%, +0.6pp).

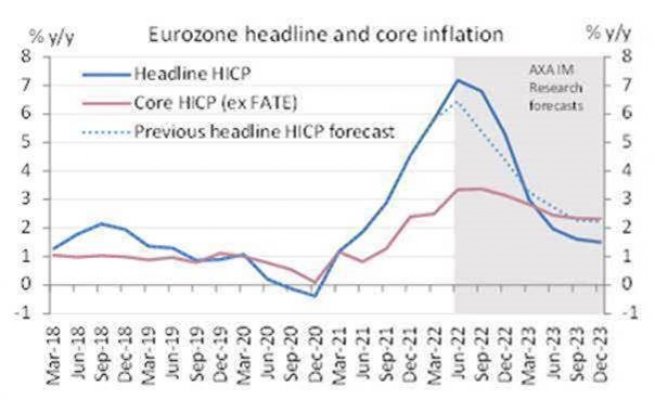

- We think eurozone HICP inflation is unlikely to recede quickly. We forecast headline inflation to remain above 6.5% yoy until the end of Q3. Overall, we anticipate inflation to average 6.1% this year (risks tilted to the upside), and remain above ECB target next year, underpinned by resilient core inflation.

- Although hard to justify macroeconomically, we cannot rule out a July ECB depo hike anymore.

Eurozone Preliminary HICP for April came at 7.5% yoy, in line with consensus and up by 0.1 percentage point (ppt) from previous month. As expected, energy inflation declined after the rebate on oil prices at the pump (baril also retreated by 10% mom in euro denominated) and some easing on gas spot prices that alleviated some pressure on very exposed country such as Spain or Italy. By contrast, FAT inflation (Food Alcohol & Tobacco) increased by 1.4pp to 6.4% yoy, a new record pace. Core inflation momentum continues to build up (3.5% yoy from 2.9%), mainly driven by an acceleration in services (3.3% yoy, +0.6ppt) while non-energy industrial goods continue to expand (3.8% yoy, +0.4 ppt).

Across countries, Germany and France surprised to the upside, reaching 7.8% yoy (+0.2pp from March) and 5.4% (+0.3 ppt) respectively while Italy was broadly in line with consensus at 6.6% (-0.2pp versus March print). On the opposite, Spain surprised to the downside, reaching 8.3% yoy from 9.8% and reflecting a material easing in fuel and electricity retail prices. Headline HICP inflation accelerated further in some countries such as in Estonia (+19% yoy, +4.2ppt), Lithuania (+16.6%, +1 ppt), Portugal (7.4%, +1.9ppt) or even the Netherlands (+11.2%, -0.5ppt).

We think eurozone HICP is unlikely to recede quickly. We forecast headline inflation will remain above 6.5% yoy until the end of Q3. In details, energy contribution should be gradually replaced by increased pressure from food prices. On core inflation there is much more uncertainty. On one side, supply bottlenecks are disrupting goods production again, so prices are likely to go up but with further risks to curb demand. Most recent labor market data for the first quarter has been quite resilient and we anticipate a further slight improvement by the end of this year which should gradually add pressure to core inflation. Overall, we anticipate inflation to average 6.1% this year (risks tilted to the upside), and remain above ECB target next year, underpinned by resilient core inflation.

On the ECB front, after ending APP at the end of June, our baseline call remains for a first depo hike in December, consistent with our macroeconomic scenario foreseeing a material weakening of the economy this year. Given the pent-up demand from services painted by latest business surveys, we acknowledged that September lift-off is a distinct possibility. In view of the latest inflation figure and rhetoric from Governing Council members, we cannot rule out a first hike in July, although would be somewhat disconnected from macro fundamentals in our opinion.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.