Tech stocks look set to potentially continue AI-led hot streak

- 30 January 2024 (5 min read)

Key points

- Technology stocks and the Nasdaq index’s superior 2023 return compared to broader equity indices reflects the exponential growth rate of the tech sector’s earnings

- Generative AI is forecast to significantly bolster productivity and add billions to the global economy

- Technological advancement across sectors will offer investors considerable opportunities to benefit from superior company earnings growth as companies use AI technology

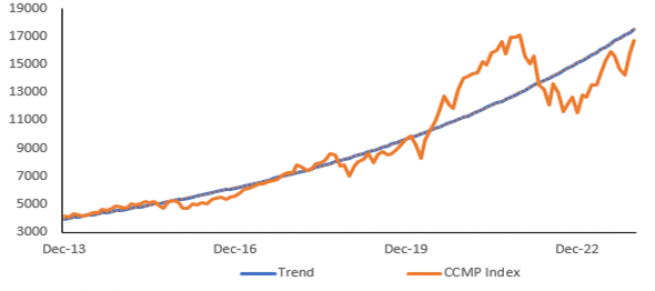

After dominating equity markets in 2023, technology stocks are showing no signs of letting up in the new year with the S&P 500 having already soared to a fresh high on the back of the sector’s momentum.1

Despite last year’s shaky macroeconomic backdrop, markets defied expectations - global equities finished the year 24% ahead, while the technology-heavy Nasdaq achieved a stellar 45%.2

For its part, the S&P 500 delivered a 26% total return – and the so-called ‘magnificent seven’ - Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla - accounted for 62% of this.3

These superior total returns reflected technology’s exponential growth rate, related earnings and of course the excitement around the rise of generative artificial intelligence (AI).

- PGEgaHJlZj0iaHR0cHM6Ly93d3cucmV1dGVycy5jb20vbWFya2V0cy91cy9mdXR1cmVzLXNpZ25hbC1tb3JlLXN0ZWFtLXNwLTUwMC1hZnRlci1yZWNvcmQtaGlnaC0yMDI0LTAxLTIyIj5TJmFtcDtQIDUwMCBlbmRzIHdpdGggcmVjb3JkIGhpZ2ggZm9yIDJuZCBzZXNzaW9uIGluIHJvdyAtIFJldXRlcnM8L2E+

- RmFjdFNldCwgZGF0YSBhcyBhdCAyOS8xMi8yMDIzIChVUyBkb2xsYXJzKQ==

- PGEgaHJlZj0iaHR0cHM6Ly93d3cuZnQuY29tL2NvbnRlbnQvODcxNDllZTUtYWJhNS00YjJiLWI4YTUtMzkxOGVlNjgxYTBiIj5JbnZlc3RvcnMgdG8gbG9vayBmb3IgQUktcG93ZXJlZCBnYWlucyBkdXJpbmcgQmlnIFRlY2ggZWFybmluZ3Mgc2Vhc29uIChmdC5jb20pPC9hPg==

Generative AI, thrust into popular culture via applications like Open AI’s conversational AI engine ChatGPT, can create and produce text, images, video, and numerous other types of content.

Generative AI can use and manipulative huge data sets to generate outputs which are beyond the capability of humans. As such its potential to disrupt an abundance of industries is huge. It will also underpin new applications across sectors as diverse as autos, healthcare and finance.

Following last year’s success, investors will be closely watching the magnificent seven, all of which are reporting earnings over the coming weeks; investors will be hoping the considerable investment such firms have made in developing their AI offering will ultimately transform into long-term gains.

The long game changer

Hopes are certainly high for technology’s – and AI’s – long-term potential; McKinsey & Company believes generative AI could add trillions in value to the worldwide economy as it automates activities that presently take up much of workers’ time.4

Unsurprisingly, the topic was ubiquitous at the World Economic Forum’s annual meeting in Davos in January. Speaking at the event, European Commission President Ursula von der Leyen declared: “AI can boost productivity at unprecedented speed. First movers will be rewarded, and the global race is already on, without any question.”5

Certainly, much of the current rhetoric around AI - and its applications - suggests the momentum is just getting started. History shows that previous technology revolutions, from industrial to the information technology wave, delivered significant productivity boosts. And higher productivity should mean better economic growth and living standards, which in turn should boost returns across a wide range of industries.

- PGEgaHJlZj0iaHR0cHM6Ly93d3cubWNraW5zZXkuY29tL2NhcGFiaWxpdGllcy9tY2tpbnNleS1kaWdpdGFsL291ci1pbnNpZ2h0cy90aGUtZWNvbm9taWMtcG90ZW50aWFsLW9mLWdlbmVyYXRpdmUtYWktdGhlLW5leHQtcHJvZHVjdGl2aXR5LWZyb250aWVyIj5FY29ub21pYyBwb3RlbnRpYWwgb2YgZ2VuZXJhdGl2ZSBBSSAtIE1jS2luc2V5PC9hPg==

- PGEgaHJlZj0iaHR0cHM6Ly93d3cud2Vmb3J1bS5vcmcvYWdlbmRhLzIwMjQvMDEvdXJzdWxhLXZvbi1kZXItbGV5ZW4tZnVsbC1zcGVlY2gtZGF2b3MiPlVyc3VsYSB2b24gZGVyIExleWVuIHNwZWVjaCB0byBEYXZvcyBpbiBmdWxsIHwgV29ybGQgRWNvbm9taWMgRm9ydW08L2E+

Fresh opportunities

The AI evolution we have witnessed to date has certainly been remarkable. While the focus has been mainly on infrastructure - cloud computing, computing capacity, and semiconductors – a plethora of sectors stand to benefit. Banking and finance, supply chains, media, marketing, life sciences, robotics and medicine could be among the biggest winners.

In addition, as AI likely weaves its way through multiple industries, numerous sectors across the tech spectrum are gearing up for potentially significant growth.

The metaverse, which allows individuals to interact with each other in shared online spaces, is expected to generate up to $5trn in value by 2030 – roughly the size of Japan’s economy. Already vital to the metaverse’s evolution, generative AI is making it even easier to transform ideas into highly realistic content and experiences.6

In addition, as concerns over online security ratchet up, the global cybersecurity market should enjoy ever-increasing growth with some reports forecasting it could reach $425bn by 2030 – up from $154bn in 2022.7

- PGEgaHJlZj0iaHR0cHM6Ly93d3cubWNraW5zZXkuY29tL2NhcGFiaWxpdGllcy9ncm93dGgtbWFya2V0aW5nLWFuZC1zYWxlcy9vdXItaW5zaWdodHMvdmFsdWUtY3JlYXRpb24taW4tdGhlLW1ldGF2ZXJzZSI+VmFsdWUgY3JlYXRpb24gaW4gdGhlIG1ldGF2ZXJzZSAtIE1jS2luc2V5PC9hPg==

- R2xvYmFsIEN5YmVyIFNlY3VyaXR5IE1hcmtldCBTaXplIFsyMDIzLTIwMzBdIHRvIFJlYWNoIFVTRCAoZ2xvYmVuZXdzd2lyZS5jb20p

Industrial policy driving growth

Advances in AI are also driving improvements in semiconductor design and production, as chips need to become increasingly complex - and semiconductors are big business, Globally, the semiconductor market witnessed sales of $600bn in 2021, but it is expected to grow to a $1trn industry by 2030.8

Government policy is also helping to spearhead growth. The US CHIPS Act is injecting $52bn into technology innovation, focused on semiconductor design and domestic semiconductor production.9

Elsewhere the US Inflation Reduction Act (IRA) introduced in 2022 should help drive a new wave of growth and innovation by helping the private sector – and investors – decarbonise energy, transportation, agriculture and other emission-intensive sectors. The IRA has earmarked billions of dollars in new spending and tax breaks to increase clean energy investment, cut healthcare costs, and raise tax revenues.

- VGhlIHNlbWljb25kdWN0b3IgZGVjYWRlOiBBIHRyaWxsaW9uLWRvbGxhciBpbmR1c3RyeSB8IE1jS2luc2V5

- Q3JlYXRpbmcgSGVscGZ1bCBJbmNlbnRpdmVzIHRvIFByb2R1Y2UgU2VtaWNvbmR1Y3RvcnMgYW5kIFNjaWVuY2UgQWN0IG9mIDIwMjIgKENISVBTIEFDVCk=

The next wave

Following 2023’s rally US equities are certainly expensive, and it would be unwise to expect the Nasdaq to match last year’s run over 2024.

But in our view, AI will offer considerable opportunities to benefit from superior company earnings growth. Naturally, some firms will shed market share if they fall behind the technological curve. In addition, how AI is regulated and used is of utmost importance.

But the potential is vast; forecasters often underestimate the pace of the technological development and adoption. We expect this theme to be a major influence on markets and investors, over the years and decades to come. Exposure to the US technology sector has been a winning strategy for the last decade and we expect this to continue for the foreseeable future.

Related Articles

View all articles

US cements itself as the global centre of tech innovation

- by Tom Riley, ,

- 29 May 2024 (5 min read)

How generative AI is transforming e-commerce

- by

- 26 April 2024 (5 min read)

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.