The unwind of the UK’s Corporate Bond Purchase Scheme: A potential liquidity opportunity for DB pension schemes

At a time of elevated outright yields and credit spreads, the unwinding of the Bank of England’s (BoE) Corporate Bond Purchase Scheme could offer UK defined benefit (DB) pension schemes a strong liquidity opportunity with which to further de-risk their investment strategies and increase holdings of cashflow generative assets.

After a decade of pretty consistently lowering interest rates and buying bonds, 2022 saw the reversal of this expansionary policy from the BoE as monetary easing was replaced with monetary tightening to combat rising inflation. Base rates have seen consecutive increases from end-2021 to reach 1.75% at the time of writing – levels not seen since 2008 – and are expected to continue to rise. Rising policy rates have driven yields up across the curve.

Lower growth would likely negatively impact corporate profitability and balance sheets, removing some of the strong fundamental support for corporate bonds. However, companies are generally starting from a relatively healthy position, and wider spreads help compensate for this increased risk, in our view.

Rising inflation, the threat of recession and monetary tightening are typically signs of negative times for investors. However, for institutional investors rising outright yields have offered cheaper entry points to de-risk investment strategies. Looking ahead it appears that these times are likely to continue, at least in the short term.

Higher yields have been driven by rising base rates but also through quantitative tightening, as the BoE has started to reduce the size of its £895bn Asset Purchase Facility (APF). The APF consists of £875bn of government bonds and £20bn of sterling investment-grade corporate bonds purchased and held by the central bank through its quantitative easing operations.

The Corporate Bond Purchase Scheme (CBPS), launched in August 2016 and further expanded in 2020, accounts for the £20bn corporate bond portion of the APF, designed to improve liquidity and reduce the yields on corporate bonds to reduce the cost of borrowing and stimulate issuance within the market. The CBPS focused on non-financial companies (excluding building societies, banks and insurance companies) that made a material contribution to economic activity within the UK.

In February 2022, alongside an increase in the Bank Rate, the BoE’s Monetary Policy Committee (MPC) voted to reduce the size of the APF by ceasing to re-invest proceeds of government bonds, and importantly, by rather unexpectedly deciding to unwind the CBPS.

Bonds for sale

Further information was announced in August 2022, with details of the process and timings for unwinding the CBPS.

Despite holdings totalling £20bn, the amounts sold back to the market are expected to be lower than this as bonds with maturity shorter than 6 April 2024 will not be sold, but rather held to maturity. The BoE will also aim to reduce its balance sheet through issuer buy backs, further reducing the requirement to sell bonds into the market.

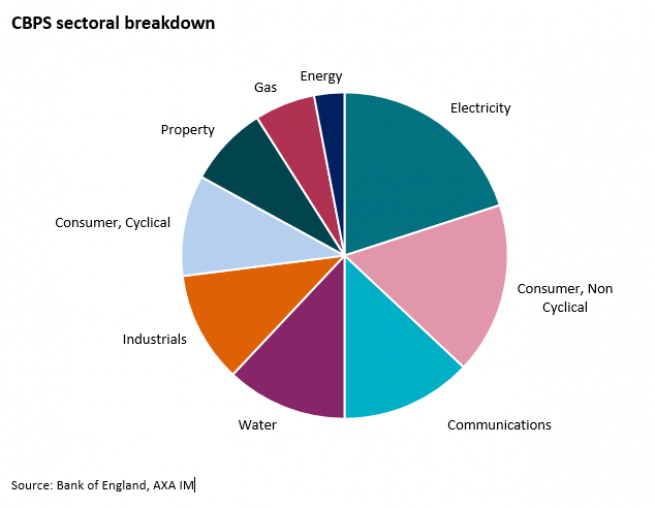

Although the exact amounts of CBPS holdings are not (and will not likely be) published, the bank has announced that £13bn of nominal value will be eligible for sale and published details of the 310 bonds across 107 issuers which will be sold. The sectoral breakdown of these holdings is shown below.

Sale process

Timings

Sales to the secondary market will take place at twice-weekly (Tuesday and Wednesday) multi-stock auctions:

Corporate bond sales programme to commence in the last week of September

Sales to be completed no earlier than towards the end of 2023

Sales programme to be paused to reflect periods of lower activity, first instance to occur between 9 December 2022 and 9 January 2023.

Most bonds held will be available for sale every week, with the key exception of bonds from issuers within the energy and gas sectors, which will be offered on a fortnightly basis due to the small weightings of these sectors. This is owing to the BoE’s greening process that occurred following the implementation of the CBPS.

Amounts

To achieve the above timeframes, the BoE expects to deliver sales of around £200m nominal per week.

Further, in an effort to preserve the diversification and construction of the CBPS and to avoid an overconcentration of sales, the bank will only sell a maximum of 5% of the outstanding nominal value of each bond (for bonds with outstanding nominal value greater than £100m; for bonds below this the full amount will be available for sale), limiting the sales of certain bonds within the portfolio.

Pricing

The BoE will set an internal maximum (reserve) spread for each bond and will not typically sell bonds at bids above this spread. The bank will decide on sales based on the attractiveness of such bids.

Bids will be allocated on a uniform spread basis, so that all successful transactions for any individual bond will be allotted at the same single spread known as the clearing spread.

Our view

At a time of elevated outright yields and credit spreads, the CBPS unwind should offer UK pension schemes a strong liquidity opportunity with which to potentially reduce risk in their investment strategies and increase holding to cashflow generative assets.

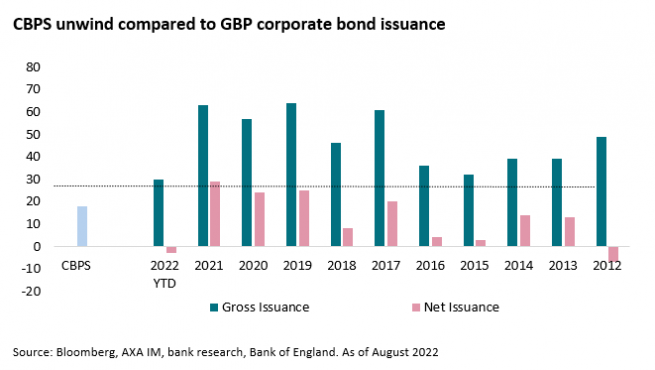

The unwind of the CBPS could offer a similar market environment to that of one with a high amount of bond issuance. These market environments can be advantageous for investors looking to enter or ramp up sterling investment grade credit allocations. In terms of size, a circa £10bn-20bn unwind of bonds is consistent with typical annual net issuance (new bonds to the market less bond maturities) for the sterling (GBP) credit market.

We believe that in a market environment of reducing liquidity and increasing transaction costs for trading corporate bonds, this CBPS unwind may potentially provide what is an unusual opportunity to reduce the costs associated with implementation of credit portfolios, capture the current elevated spreads and enhance portfolio cashflows.

Institutional Featured Solutions

We help institutional investors by building innovative and sustainable custom solutions to support ever-evolving financial, regulatory and stakeholder needs.

Find out moreDisclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.