Multi-Asset Investment Views: And the beat goes on

- 02 April 2024 (7 min read)

Our views

Since our last publication equity markets have continued to grind higher. We stay constructive despite strong performance year to date and think that there is room for more upside. Sentiment is positive but not overly so whilst positioning, which has clearly risen, is not extreme. It is not just the US market which is flirting with all-time highs but many others too including Japan, India, Italy, Eurostoxx 50, Korea and the DAX. The Eurostoxx 50 has even outperformed the mighty Nasdaq year to date. Whereas the initial leaders over the last 12 months were clearly the American ‘Magnificent 7’, boosted by the artificial intelligence (AI) theme, market is now differentiating between these companies, and this is a good thing.

Performance of the Magnificent 7 is very different year to date with Nvidia up over 90% but Tesla down more than 30%. Market breadth is expanding in the US and cyclicals and financials are catching up but this is not yet the case in Europe where a large chunk of performance is coming from the ‘Granolas’ – the European equivalent of the Magnificent 7. This is logical given the quality, cash flow generation and earnings power of this group of stocks but we would like to see breadth to expand more to maintain our confidence.

Some of the recent optimism was provided by central banks where activity was busy. The most important news was from the Federal Reserve. At its March meeting, policy was left unchanged, and the decision was unanimous as expected. However, the median rate outlook continued to see three cuts for 2024, most likely starting in June. Growth expectations were raised for 2024 (end year 2.1%) and future years growth also nudged higher to 2%. Expectations for cuts in 2025 were also reduced to three. Overall Chair Jerome Powell was confident that progress was being made on bringing inflation down even though it might take a little longer. The argument for a ‘soft landing’ which the economy is currently experiencing seems well supported in that growth is a little better, unemployment is stable whilst inflation subsides slowly.

The other big news proved to be a miniscule yet ground-breaking change in policy stance from the Bank of Japan (BoJ). The BoJ exited its negative interest rate policy and nudged rates to 0%-0.10% whist also abandoning its yield curve control policy. Whether this is enough to change the direction of the yen remains to be seen as commentary from the BoJ insisted policy would remain loose and purchases of Japanese Government Bonds would continue. The other major surprise was a 25 basis point cut from the Swiss National Bank mostly to ease pressure on the Swiss franc which hampers the country’s terms of trade. The European Central Bank (ECB) communication remains very prudent. We expect the ECB to loosen policy sooner rather than later and perhaps even stealing a march on the Fed.

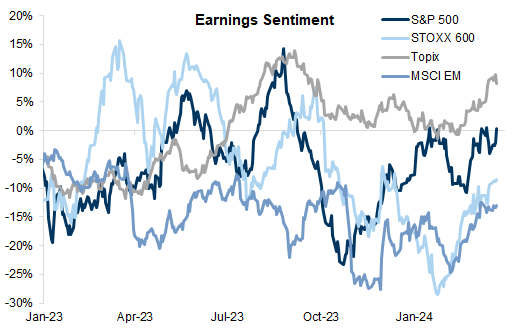

Moving back to equity markets, we now have more visibility on central bank policy whilst economic growth is relatively resilient. Even in the Eurozone, where growth is bumping along the bottom, there are some bright spots. The services sector is clearly doing much better than the manufacturing sector and given the drip-feed of stimulus and support the Chinese authorities are injecting into their own economy, there is hope that we can recover from low levels and demand for our exports could pick up. A better growth/inflation mix and lower rates should continue to be a positive support for equities. The earnings outlook is also improving and IBES consensus expects between 7%-9% for the major developed markets in 2024 and then improving to 10%-14% in 2025.

This, combined with higher pay-out ratios and share buy backs, should support some further equity market gains. Although AI and its expanding ecosystem remains a very powerful thematic there are plenty of others including defence, onshoring, GLP-1 (obesity drugs), cybersecurity and climate-related.

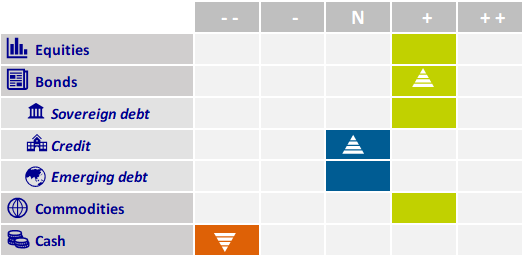

Our portfolios remain overweight equities. Whilst the US is clearly our preferred market we have also added to Japanese and Eurozone equity markets. The structural story for Japan remains and we can find many world class leaders in their field particularly in the semiconductor space at cheaper multiples. Eurozone stocks have done well and could do even better if signs of better growth are confirmed as valuations are not stretched relative to history. We also like the Nasdaq given its exposure to themes we favour such as AI, robotics, cybersecurity, semiconductors, and its superior earnings power.

Elsewhere in our portfolios we have begun to increase duration through Eurozone debt focused on the five-year part of the German yield curve whilst we are re-entering a steepener position on the US curve predicated on a bullish steepening between two-year and 10-year maturities as we approach the first cut from the Federal Reserve.

In terms of diversification trades, we remain overweight the US dollar (versus British pound in this case) and exposed to commodities (excluding agriculture and livestock) with supply constraints, geopolitical risks and rising positioning providing support.

Earnings sentiment improving (no upgrades/no downgrades)/no estimates

Source: FactSet, Stoxx,GS GIR

Related articles

View all articles

Hedging inflation: Fundamentals and scarcity

- by Chris Iggo

- 26 July 2024 (7 min read)

CIO Views: UK back in investors’ focus; Bunds in favour

- by Chris Iggo, ,

- 25 July 2024 (5 min read)

CIO Views: UK back in focus; China’s consumer challenge

- by Chris Iggo, ,

- 25 July 2024 (5 min read)

An investors’ guide to high yield bonds

- by

- 23 July 2024 (7 min read)

Pass the popcorn

- by Chris Iggo

- 19 July 2024 (5 min read)

Multi Asset Views - July 2024

- by Laurent Clavel

- 15 July 2024 (3 min read)

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ.

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

© 2024 AXA Investment Managers. All rights reserved

Image source: Getty Images

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.