Thematic investing takes centre stage among fund selectors after AUM surged 77% last year

While the widespread adoption of a thematic approach to investing is still relatively new, thematic funds now contain around €572 billion1 of assets worldwide having grown at an annual rate of 37% since 2018. Not only that, but demand is accelerating, with thematic funds growing by 77% in 2020.

Fund buyers said thematic equity investing – defined as an approach which aims to gain exposure to companies which will benefit from clear long-term structural changes resulting from political, economic, and social forces – is increasingly core to client portfolios.

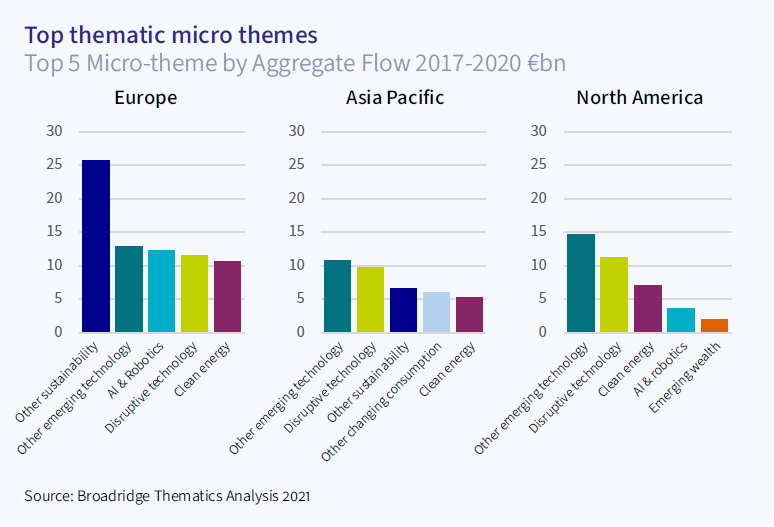

In research conducted by Broadridge on behalf of AXA Investment Managers (AXA IM), it found that there had been significant demand from fund buyers around the world for different types of thematic investing. ‘Multi-sustainable’ funds in Europe, emerging technologies such as disruptive tech, AI & Robotics in North America and Asia Pacific, and a range of other themes such as security/cybersecurity, fintech, semiconductors, connectivity and digitalisation have all been popular.

As well as broad sustainability trends, the research found the popularity of tech is reflected globally, particularly in the proportion of fund flows directed to this theme in recent years – as shown in the chart below.

Note: ‘Other’ technology is a micro theme we use to capture the opportunity arising from a range of other emerging technology focused themes, which are predominately clustered among security/cybersecurity, fintech, semiconductor, connectivity, and digitalisation opportunities.

Crucially, we have seen that the global pandemic has significantly accelerated many of the trends within the thematics universe, and prompted the emergence of new ones.

The survey found that climate change was an increasingly important issue for many of the fund selectors interviewed, particularly in Europe. This suggests that the urgency to address shortcomings around the topic of climate change was amplified due to the pandemic, as investors and asset managers, including AXA IM, explored a broader range of climate-related priorities. These included ‘Net Zero’ commitments, climate benchmarks and Paris Agreement-aligned investment opportunities.

In addition, many respondents highlighted that the pandemic had signified the ‘dawn of a remote economy’, with digitalisation boosted by its leading role in countering the pandemic.

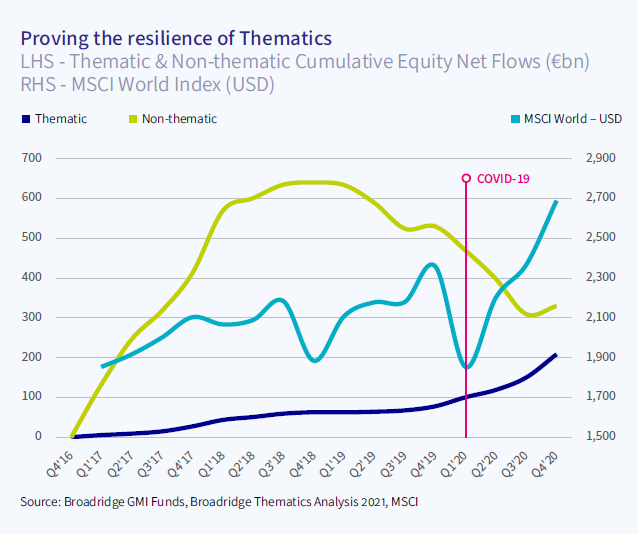

Thematic funds have also proven their resilience during COVID-19 – unlike many other types of funds, they have been able to raise assets against the backdrop of Covid . Where other non-thematic fund products may have seen some outflows since the outbreak of COVID-19 and the corresponding falls in stock markets (and indeed since the downturn in 2018 as well), thematic funds have continued to attract new investors.

While critics sometimes say thematic funds are only ever capable of raising assets in a bull market, the chart below illustrates that the strategies have been quite capable of presenting a strong case to investors in even the most distressed of market conditions.

Broadridge’s research also found that fund selectors use thematic products in varied ways and favour actively managed funds, with 73% of thematic assets being held in active as opposed to passive funds. While passive managers have attempted to capitalise on soaring retail interest in thematic investing, this remains the domain of active managers.

In the past, thematic funds were often seen as specialist or separate holdings, however increasingly, especially in Europe, they are used as a diversifier within global equity portfolios. Most investors see thematics as a long-term or strategic investment, with only one in four saying they use thematics in a tactical way.

We believe thematic funds have already transformed the industry. While thematic assets represent a small part of the overall funds market, this corner of the industry has taken almost two-fifths of all fund net sales since 2017 and it is not unreasonable to think it will continue to play an important role as we transition to this new normal of equity investing.

Disclaimer

Note to Editors

All figures are sourced by Broadridge and AXA IM and are as at 31st December 2020. The data referenced in this release only includes thematic funds that Broadridge tracks globally.

90 fund selectors across Europe, Asia Pacific and North America were interviewed during Q1 2021 for the White Paper, exploring their usage of and views on thematic funds on a qualitative basis.

To read the full White Paper, please click here: Thematic investing set to transform asset management?

This press release should not be regarded as an offer, solicitation, invitation or recommendation to subscribe for any investment service or product and is provided for information purposes only. No financial decisions should be made on the basis of information provided.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.