China in a bull shop

Laurent Clavel and Serge Pizem discuss their macroeconomic and asset allocation convictions for May 2019.

According to Laurent Clavel, Head of Research at AXA Investment Managers: “We see world trade and Chinese slowdowns bottoming out, Eurozone should follow whilst the US modestly slows”.

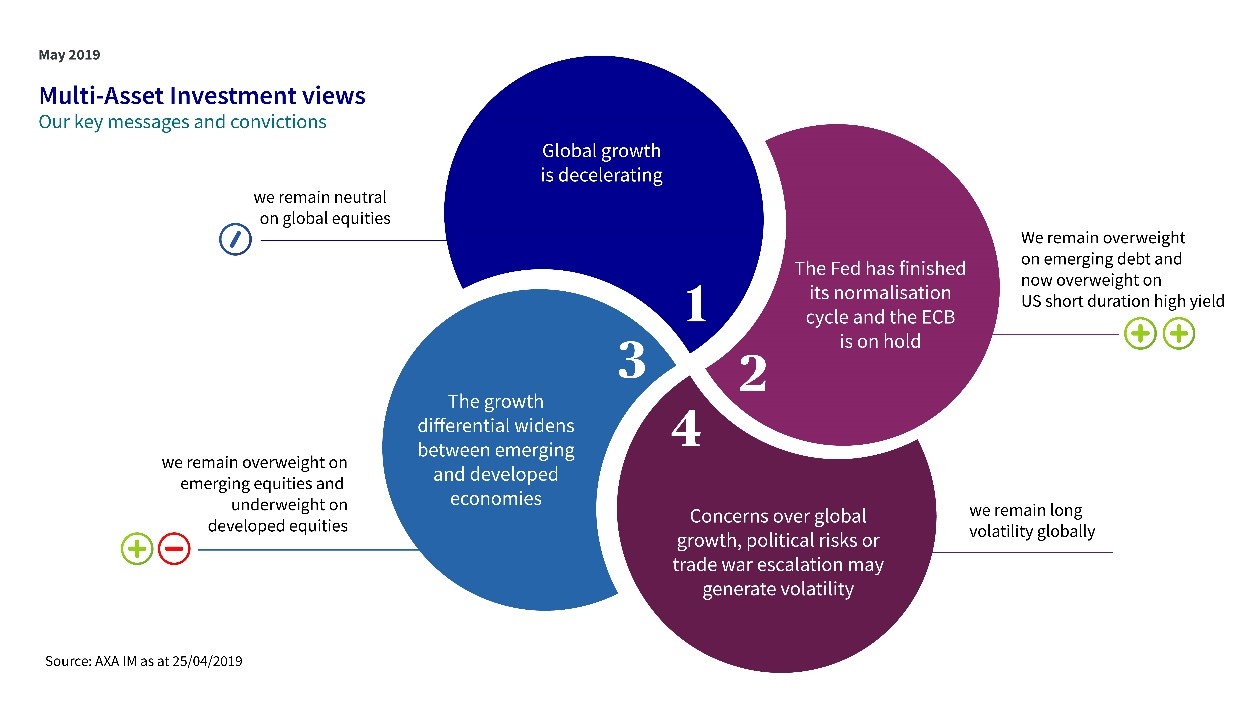

- With the “policy put” in place (dovish US Federal Reserve and European Central Bank, fiscal stimulus in China and Eurozone), we have been waiting for signs of a cyclical upswing…

- … getting us to focus on China and Asian trade; both point to the slowdown bottoming out.

- This is good news for the Eurozone where the sequential improvement has been very modest so far.

- US GDP should slow for the third consecutive quarter, partly on temporary factors. Still, our US recession probability model has been worryingly nearing its relevant threshold.

“With the “policy put” in place ; which includes the downgrading of the Fed’s “dots” and the announcement of the early end of its balance sheet unwind, the ECB’s renewed dovishness in the extension of its forward guidance, adding the significant Chinese fiscal stimulus (worth more than 2% of GDP) and the more modest fiscal boost in various Eurozone member states ; the stage was set for a sequential economic acceleration. The main source of this slowdown came from Asian trade and China. Yet, the Chinese demand should bottom out in the next few months. We also observe a rise in lending since January – reflecting Chinese stimulus – which historically has preceded an upturn in activity by about six months. This is reassuring as Chinese imports are still contracting sharply. Moreover, according to our indicators, Asian export growth seems to hint his bottom.

Current global trade weakness explains subdued readings in global industrial output and manufacturing surveys, including some of the most recent US business surveys. As the consensus view on Eurozone macroeconomics was very hopeful (in terms of timing and magnitude), the latest European business surveys came in below consensus expectations. To date the sequential improvement has been very modest. An improvement in Asian activity and global trade should support industrial indicators over the coming quarters. More importantly, business confidence has remained elevated in services, dissipating fears of a contagion of the past manufacturing slowdown.Meanwhile, the US economy looks set to slow for the third consecutive quarter, at around 1.5% annualised in the first quarter of 2019. We however see this to prove partly temporary with retail and government spending rebounding to support the second quarter – around 2.5% – and with some residual seasonality also persisting.”

Click here to read our macro-economic views of the month.

Serge Pizem, Global Head of Multi-Asset Investments at AXA IM exposes his asset allocation views for the month to come: “The overall backdrop leaves us with a risk appetite that is modest but rising, in spread product in particular – US High Yield and emerging market debt – amid the renewed trend of lower global rates. Within equities we direct our overweight in Emerging Markets and euro banks, where the rebound in valuation multiples year to date has lagged in comparison to US stocks. We maintain a neutral stance in terms of duration exposure amid global fixed income. This is a prudent stance while we navigate a potential turning point in global growth where more proof signals are required before turning cautious on duration.”

- We overweight emerging markets assets, both debt and equities as a more dovish Fed, a peaking US dollar and cheaper valuations are supportive.

- We maintain Euro core government bonds at neutral as a lower growth and falling inflation should cap bond yields.

- We remain prudent on US and Eurozone equities given valuation levels and lower expected earnings growth.

“The most recent strength of equity markets was primarily driven by improvements in Chinese economic data. However, we think that the recovery of the global cycle of output and trade is unlikely to be confirmed before this summer.

Firstly, the situation remains particularly difficult in Europe. Softness appears the most severe in Germany’s manufacturing sector but is nonetheless wide-spread across the region.

Secondly, green-shoots in China are currently the best hope for a Eurozone manufacturing rebound. However, there is usually a lag of 6-months between turn-arounds in China and turn-arounds in the European manufacturing sector. In the meantime, European Union exporters may have to contend with additional risks such as rising oil prices and potentially US tariffs on car exports.

Thirdly, the US economy, which was the last to feel the effect of the global slowdown, should continue to decelerate as the positive impact of the Trump Tax give-away fades.

Equity markets valuations are now back above their long-term average in a context where things may get worse before they get better. We therefore prefer to maintain our current neutral position on equities and to move to an overweight on Fixed Income where we favor carry trades in High Yield credit and Emerging markets debt.”

Click here to know more on our asset allocation views for the month.

Disclaimer

About AXA Investment Managers

AXA Investment Managers (AXA IM) is an active, long-term, global multi-asset investor. We work with clients today to provide the solutions they need to help build a better tomorrow for their investments, while creating a positive change for the world in which we all live. With approximately €730 billion in assets under management as at end of December 2018, AXA IM employs over 2,350 employees around the world and operates out of 30 offices across 21 countries. AXA IM is part of the AXA Group, a world leader in financial protection and wealth management.

- Visit our website: www.axa-im.com

- Follow us on Twitter @AXAIM

- Visit our media centre: www.axa-im.com/en/media-centre

AXA Investment Managers UK Limited is authorised and regulated by the Financial Conduct Authority. This press release is as dated. This does not constitute a Financial Promotion as defined by the Financial Conduct Authority and is for information purposes only. The content herein may not be suitable for retail clients. No financial decisions should be made on the basis of the information provided. Any mention of a strategy is not intended to be promotional and does not indicate the availability of an investment vehicle.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.