Short duration bonds: a natural complement to corporates’ cash allocation

With falling interest rates and sticky inflation, holding liquidity buffers in cash or money market funds is becoming increasingly costly. Short duration bonds could be a natural complement to cash allocations for corporates looking to improve real returns.

Liquidity is more important than ever for corporates seeking to optimise their cash balance. They must preserve capital and generate returns within specific risk parameters in an uncertain environment. But with falling interest rates and sticky inflation, holding liquidity buffers in pure money market funds is becoming increasingly costly.

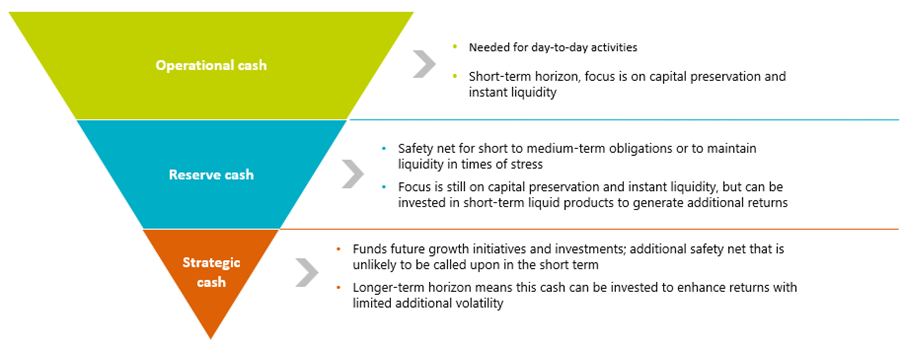

Different types of cash for different needs

Not all cash is equal. Rather than a single element cash holdings can be divided into three main categories: operational, reserve and strategic.

Different liquidity needs for different investment strategies

Source: AXA IM as at 30 September 2025. For illustrative purposes only.

Operational and reserve cash are typically held in bank accounts or money market funds, as instant liquidity and capital preservation are paramount. However, for strategic cash, corporates face more complex decisions, balancing the goal of enhancing returns with the need to preserve capital.

In this context, we believe short-dated bonds could offer an attractive alternative. With maturities up to five years, these bonds typically offer higher yields, natural liquidity and low volatility, making them a natural extension to enhance cash returns with limited additional risk.

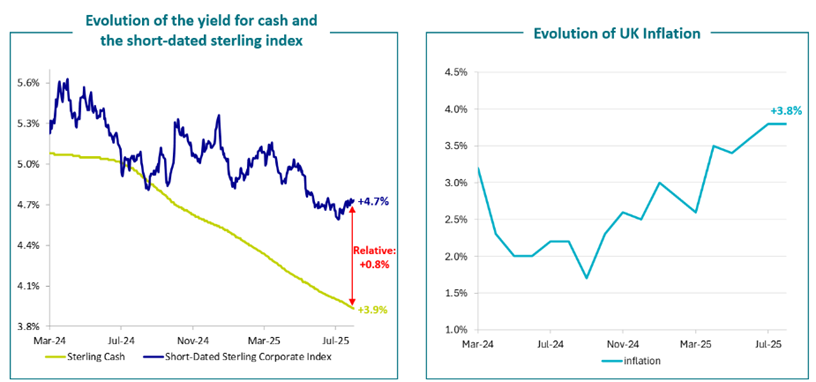

Cash is no longer king

In the recent past, there was little opportunity cost to holding cash compared to short-dated bonds as interest rates and short-dated bonds yields were close to zero and inflation remained subdued. Cash also proved to be a safe haven for corporates as interest rates rose sharply in 2022.

But now the dynamic has shifted. Central banks have begun – and are expected to continue – cutting base interest rates, leading to lower cash returns. Meanwhile, elevated and sticky inflation is eroding real returns (nominal returns minus inflation).

As a result, cash yields have decreased over the past two years, while short-dated bonds yields have also declined, but to a lesser extent. This means that short-dated bonds yields now offer a premium of 80bps over cash. Furthermore, the real yield (including inflation) for cash investors was only 0.1% as at August 2025, making short-dated bonds a potentially attractive alternative to mitigate the negative impact of continuing high inflation.

Additionally, there are pressures stemming from political uncertainties and US tariffs that could further increase costs and impact margins over the long term, highlighting the importance of an optimised cash management strategy.

Yields on cash have fallen faster than short-dated bonds while persistent inflation undermines real returns

Past performance is not a reliable indicator of future results.

Source: AXA IM, Bloomberg as at 31/08/2025. Left hand chart: The graphic represents the short-dated sterling corporate index and cash yields. Short-Dated Sterling Corporate Index is represented by the ICE BofA 1-5 Year Sterling Corporate & Collateralized Index. Cash is represented by the ICE BofA British Pound 3-Month Deposit Bid Rate Average Index (L5BP). Right hand chart: The graphic represents the evolution of the UK CPI as represented by the UKRPCJYR Index. Latest data available is at 31/08/2025.

Short-dated bonds, a natural and compelling solution to enhance cash returns

The dual challenge of higher operating expenses and lower cash rates means that corporates need to consider additional alpha sources to achieve greater real returns on cash. In a falling rates environment, there is an opportunity cost to staying invested in cash or money market funds as not only does the yield on cash keep falling as central banks cut interest rates, but you also miss out on the expected positive performance of short-dated bonds on the back of lower front-end yields.

Short-dated bonds can help address corporates’ challenges as they offer yield enhancement, provide a regular steady income, and have natural liquidity, with limited additional sensitivity to interest rate and credit spread moves. They can also provide a natural funding source, with regular dividend distributions.

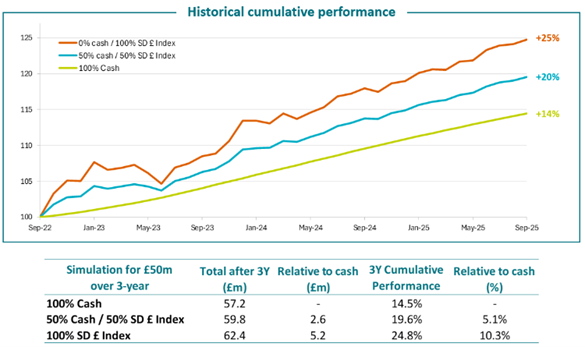

Short-dated bonds have provided superior returns to cash over the last three years with limited extra volatility

Past performance is not a reliable indicator of future results.

Source: AXA IM, Bloomberg as at 30/09/2025. For illustrative purposes only. Cash is represented by the ICE BofA British Pound 3-Month Deposit Bid Rate Average Index (L5BP) and the short-dated sterling corporate index (SD £ Index) is represented by the ICE BofA 1-5 year Sterling Corporate & Collateralized Index (UC0V).

Short-dated bonds have outperformed cash rates by +10% over the last three years with limited extra volatility. A £50m strategic cash allocation split 50/50 between cash and short-dated bonds generated circa +5% (£2.6m) more than a 100% allocation in cash over the last three years, demonstrating the effectiveness of using short-dated bonds to enhance cash.

We believe that an optimised approach is not all in cash or money market funds, but rather a tiered liquidity waterfall including short-dated bonds. In this way, corporates could benefit from higher yields and predictable income with limited additional volatility, while being better aligned with their longer-term goals and risk profile.

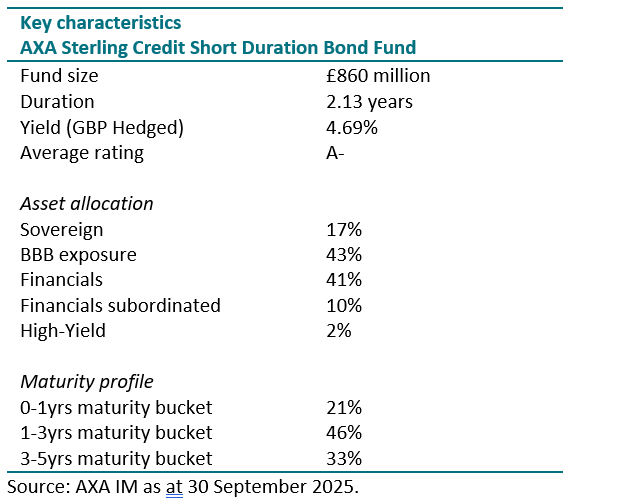

Why AXA Sterling Credit Short Duration Bond Fund?

Active management - Opting for active managers such as AXA IM in the short-dated bond universe compared to passive solutions offer additional advantages such as default risk mitigation, the avoidance of forced sales and the potential for further yield enhancement though careful bond selection and active changes in asset allocation.

Designed to complement cash holdings – The AXA Sterling Credit Short Duration Bond Fund is designed for investors looking for a reasonable pick-up in return compared to cash, without taking too much additional risk with their capital.

Conservative approach – The fund follows a conservative approach, with a significant emphasis on limiting drawdowns and generating income. This high-quality fund is unconstrained and actively managed, enabling the investment team to exploit investment opportunities across the short-dated sterling market (bonds with less than five years maturity), while targeting a minimum rating of A- at portfolio level. Additionally, the fund benefits from daily liquidity.

Recognised and longstanding expertise – The AXA Sterling Credit Short Duration Bond Fund is managed by a longstanding and multi award-winning investment team, with a proven track record of limiting drawdowns in market downturns, while generating attractive returns in up markets.

No assurance can be given that the AXA Sterling Credit Short Duration Bond Fund will be successful. Investors can lose some or all of their capital invested. The AXA Sterling Credit Short Duration Bond Fund is subject to risks including credit, ESG, interest rate, prepayment and extension, stock lending risks. Further explanation of the risks associated with an investment in this Fund can be found in the prospectus.

Disclaimer

Not for Retail distribution: This marketing communication is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This marketing communication does not constitute on the part of AXA Investment Managers a solicitation or investment, legal or tax advice. This material does not contain sufficient information to support an investment decision.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Before making an investment, investors should read the relevant Prospectus and the Key Investor Information Document / scheme documents, which provide full product details including investment charges and risks. The information contained herein is not a substitute for those documents or for professional external advice.

The products or strategies discussed in this document may not be registered nor available in your jurisdiction. Please check the countries of registration with the asset manager, or on the web site https://www.axa-im.com/en/registration-map, where a fund registration map is available. In particular units of the funds may not be offered, sold or delivered to U.S. Persons within the meaning of Regulation S of the U.S. Securities Act of 1933. The tax treatment relating to the holding, acquisition or disposal of shares or units in the fund depends on each investor’s tax status or treatment and may be subject to change. Any potential investor is strongly encouraged to seek advice from its own tax advisors.

For more information on sustainability-related aspects please visit https://www.axa-im.com/what-is-sfdr

Past performance is not a guide to current or future performance, and any performance or return data displayed does not take into account commissions and costs incurred when issuing or redeeming units. References to league tables and awards are not an indicator of future performance or places in league tables or awards and should not be construed as an endorsement of any AXA IM company or their products or services. Please refer to the websites of the sponsors/issuers for information regarding the criteria on which the awards/ratings are based. The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested. Exchange-rate fluctuations may also affect the value of their investment. Due to this and the initial charge that is usually made, an investment is not usually suitable as a short term holding.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ.

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.