How institutional investors can make a social impact in portfolios

The momentum around net zero investing has helped focus the minds of institutional investors on ways to tackle climate change and how to respond to the changing policy landscape. This has led to fundamental change in how pension funds and insurers view their portfolios over the longer term – leading to the steady integration of environmental risks and opportunities.

It is perhaps understandable that social factors – the S in ESG – have appeared to take a back seat as a result of this carbon ‘tunnel vision’.1 Their dispersed nature contrasts with the linear clarity of the net zero narrative. However, these social factors lie at the heart of corporate strategy and can potentially give clues to future corporate fragilities. For any investor seeking to protect against downgrades or defaults – and looking to support a more sustainable economy over the longer term – it may be time to discover how they could be successfully integrated. At AXA IM, we see a spectrum of implementation possibilities for institutional investors who want to take an active view around social investing.

The first option is to focus on the potential financial benefits of making sure the ‘S’ forms an important part of the ESG analysis carried out by your asset manager. Social factors such as supply chain management, human capital policies and discrimination can have direct and immediate effects on company valuations, and we think there are clear advantages in addressing such material risks as investors seek to improve risk-adjusted returns. In fixed income, this is about avoiding defaults and downgrades – in equities it can be about improving alpha, or excess returns. To do it, investors might set exclusions criteria or tilt portfolios to issuers with better performance on social factors, as well as supporting active engagement that encourages businesses towards more sustainable practices.

To take a step up in the social spectrum, investors may wish to apply a ‘do no significant harm’ principle to portfolios, involving the removal of issuers associated with the worst negative impacts from social factors. This would be from a purely non-financial perspective, although we would expect a risk mitigation effect and a close correlation with tail-risk ESG scores which we believe can be aligned with more resilient financial performance. This principle is gaining traction with regulators and forms a key pillar of the EU Taxonomy – new European rules designed to define the activities companies can claim are climate-friendly.

A further enhancement of social integration in portfolios can be delivered through the pursuit of a measurable positive social contribution. This may involve favouring issuers with best-in-class social practices around things like gender diversity at board level or workplace accidents, even if a company is not directly involved in socially progressive business activity. Investment philosophy will play a role here: Do you believe companies that make a good social contribution will hold less risk over the longer term?

The fourth and final stage of the social investing spectrum moves into the realm of pure ‘impact’. At this point investors can consider social and sustainability bonds as well as companies where the social impact is deliberate, genuine and measurable. It also opens up the possibility of detailed key performance indicators (KPIs) that offer alignment with the Sustainable Development Goals (SDGs), the United Nations targets that are helping set the direction and drive the momentum for countries and investors alike.

Overcoming challenges

To integrate social factors in portfolios, whichever approach is favoured, we need appropriate metrics. In this social space, that throws up some intriguing challenges, compared to our now familiar climate-related metrics:

- Uniformity: The S in ESG is a many-headed beast. Everything related to staff, suppliers, consumers and other stakeholders contains a social element, as do many of the factors primarily considered as environmental concerns. The dispersed nature of social factors risks blurring the focus or forcing compromises between them. Contrast this with the single and specific goal of achieving net zero by 2050 and the uneven approach to social investing is unsurprising

- Unity: Whereas climate and net zero enjoy a relatively strong consensus between governments, investors and consumers, the picture around social is less joined up. Investors are steadily getting there, and many consumers are already thoroughly engaged, but we believe policy and regulation often struggle to properly address the many and varied fragilities at play in social – partly due to the lack of uniformity described above, and partly due to the political challenges involved

- Urgency: Climate change is now understood as a clear and present danger. The timeframe has been established and the need for action aligned with that goal. Social effects, however, could take longer to emerge and be attributed to multiple factors. Some effects will be immediate, but may be related to an individual issuer, such as in the handling of human capital.

So how can investors address these challenges? We think the 17 SDGs offer a genuinely powerful framework that helps to overcome the issue of uniformity – it can be argued that most of them relate to social considerations directly or indirectly, often in combination with the environment. Their breadth of coverage and universality are precisely what is required if an investor wants to reshape a portfolio with the goal of either mitigating against social risks, or directly contributing to social good.

Scoring remains a combination of the qualitative with the quantitative – an inexact science – but we have seen that most issuers can be scored against most of the SDGs using third-party data and our own research. That delivers a scoring system that runs from +10 to -10 to cover both risk-mitigation from potential significant harm and verifiable positive impact. A lot of issuers fall somewhere in the middle but importantly, standout problems can be identified, and it is becoming clear over time that regulatory requirements (e.g. the EU Taxonomy) may be mapped across the SDGs. We do recognise that these are a starting point in the social investing journey and the market will likely evolve over time – as in the case of climate investing.

Putting it to work in portfolios

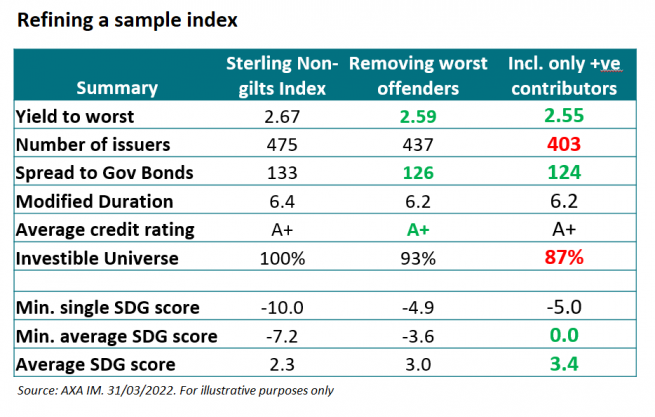

As an illustration of how using the SDG framework could work in practice, we looked at the impact in the investable universe when excluding the worst offenders – and identifying any potential effect on financial results. Where that line is drawn is down to the individual investor, but in our sample analysis, we used the sterling non-gilts index and excluded any issuer with an overall SDG score of below -5.2 We would consider this an appropriate ‘do no significant harm’ policy.

- ESG – environmental, social and governance

- We calculate SDG scores by looking at the best and worst scores among the 17 goals. If the lowest score is positive, then we simply assign the high score to that issuer. If the lower score is negative then we subtract that from the high score to arrive at a final ranking. Therefore, if a company has a high of +4 for Climate Action, but low of -6 for Reduced Inequalities, their final score will be -2.

That had some important effects. As one would expect, there is an improvement in the SDG scores – both the minimum individual SDG score and average SDG score increased, but what about the financial metrics? The yield to worst fell marginally to 2.59% from 2.67% and the spread to government bonds dipped to 126 basis points (bp) from 133.3 Our view is that these financial implications are negligible and can potentially be addressed using active management. This would allow investors to improve their social impact while aiming to maintain the desired financial characteristics of their portfolios. In addition, the exclusions allowed us 93% of the original investable universe while the average credit quality was unchanged. In our view, this shows that one is able to build a broad fixed income portfolio while also improving its social footprint.

Another illustration shows a possible alternative approach – including only issuers that achieved an overall positive SDG score. This ramps up the effect on all measures in our example. The average SDG score moves to +3.4 versus +2.3 for the universe while the investable cohort drops to 87%. The yield to worst dips a little more, to 2.55%, as does the spread, to 124bp. Again, we believe this effect on financial performance could potentially be mitigated by careful active management. More dramatic exclusions, for example removing any company that has a single negative SDG score, could have very damaging effects on future performance, so we advise caution on implementing harsh guidelines or restrictions unless investors are willing to accept potentially lower risk-adjusted returns.

The direct route: Social bonds

For all the possible advantages of this approach, and the ability to identify a positive overall social contribution, it remains difficult to measure direct social impact. This is an important distinction, and a gap that social bonds may be able to fill.

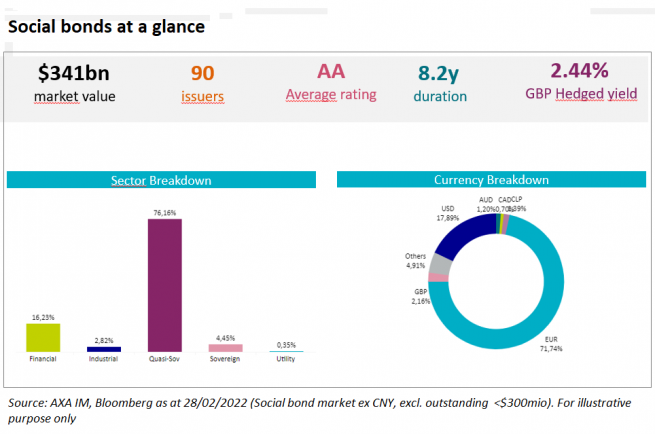

There has been some significant growth in this market, echoing and even surpassing the gains made in the green bonds market at the same point in maturity, and reflecting interest generated through the impacts of the pandemic. In 2021, social bond issuance was up 70% versus 2020 at $175bn, while its sister sector, sustainability bonds, saw issuance hit $157bn for the year.4

The market is currently driven by quasi-sovereigns but more corporates, including financials and industrials, have started to issue bonds in what may be a crucial signal to investors that this space could offer more interesting yields. Meanwhile, euro-denominated debt still makes up more than half the market, but dollar volumes are increasing year by year in another promising sign for the sector’s diversification.

- A bond's yield to worst is calculated based on the earliest call or retirement date and represents the lowest possible yield on a bond that stays within the terms of its contract (without defaulting).

- Source: AXA IM, Bloomberg as at 28/02/2022

Mirroring the use of social SDGs to refine your wider portfolio, social bonds offer very clear mapping to the SDGs, with direct and measurable KPIs. Common major themes might include health, with the target to increase the number of available beds in hospitals, or empowerment, with the goal to preserve or create new employment opportunities, particularly in underserved areas.

Social bonds are not created equal, and we believe it is important for asset managers to use clear and precise frameworks as we seek to ensure the quality of issuance. We demand verifiable KPIs that we can legitimately measure. We consider a high level of scrutiny to be our defence against ‘socialwashing’ just as it is for greenwashing – when an issuer’s claims outpace their actions.5

Using our proprietary AXA IM social bond framework we aim to delve into companies’ overall sustainable strategy; the projects in question; the specific use of proceeds from the bond; and the level of impact reporting. Crucially, if a social bond falls short on any of those we would choose not to invest.

Social investing is a small but growing area of importance for many investors. We believe it will rise to the fore over the coming years as investors, governments and consumers overcome the challenges currently faced in implementing social progress.

- https://www.axa-im.com/who-we-are/impact-investing

Disclaimer

The ESG data used in the investment process are based on ESG methodologies which rely in part on third party data, and in some cases are internally developed. They are subjective and may change over time. Despite several initiatives, the lack of harmonised definitions can make ESG criteria heterogeneous. As such, the different investment strategies that use ESG criteria and ESG reporting are difficult to compare with each other. Strategies that incorporate ESG criteria and those that incorporate sustainable development criteria may use ESG data that appear similar but which should be distinguished because their calculation method may be different.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.