Addressing climate change: how to integrate climate into your cashflow driven strategy

We believe cashflow driven investors should Assess, Integrate and Monitor (AIM) their portfolios through a climate-related lens to help deliver resilient, sustainable income to pay scheme members.

Highlights:

- Greater awareness of climate-related risks and regulatory requirements should be a catalyst for investors to assess their portfolio objectives

- Green bonds play an important role in climate-aware portfolios, however investors should not lose sight of the financial and climate-related benefits of maintaining a wide investment universe

- Risk-focussed portfolio construction and company engagement are essential to integrate climate-considerations to manage market risks and to drive progress towards a Net Zero carbon world

- Investors should monitor how their climate metrics improve over time as more issuers make stronger commitments and new investments are made that are more closely aligned to the Paris Agreement

Introduction

Our recent paper described why cashflow driven investors should act now to be ‘climate-aware’ in order to mitigate against portfolio risks, fulfil regulatory obligations and target alignment with the Paris Agreement. This paper focuses on how investors can implement climate considerations into their cashflow driven investment (CDI) portfolios. The urgency to implement climate-strategies has increased due to investor, regulatory and political momentum and a steadily warming global temperature. These emerging risks are a difficult bedfellow with the predictability required by cashflow driven investors. Climate change could significantly affect the performance of credit markets, one of the core components in CDI strategies.

Climate-aware, long-term credit has a natural alignment with the time horizon over which climate-related risks can materialise – what you invest in today should deliver sustainable cashflows for members while allaying climate-related risks. We believe investors can AIM for Net Zero by Assessing, Integrating and Monitoring their portfolios through a climate-lens to help towards the goal of delivering resilient, sustainable cashflows to pay pension scheme members.

Assess the suitability of your existing objectives

Investors today have greater access to the data, tools and approaches required to assess and manage climate-related risks. In addition, greater disclosure around climate is becoming a regulatory reality for UK pension schemes with the Task Force on Climate-related Financial Disclosures (TCFD) becoming mandatory in October 2021 for large schemes. For these reasons, we believe investors should now assess whether their existing investment strategy remains suitable to meet these climate criteria. Two high level objectives investors can set for climate investing are to:

- mitigate the material risks to portfolios from a range of temperature scenarios

- help limit the global temperature rise to 1.5-2.0°C above pre-industrial levels by 2100

Starting with the latter – this goal is typically targeted by aiming to produce Net Zero greenhouse gas emissions by 2050. Interim targets, such as halving emissions by 2030, can also be used to ensure the changes required are not left until December 2049. It is important for schemes to consider the expected pathway of carbon emissions over time. This can be a more robust method of assessing whether your portfolio is on track to achieve its Net Zero goals, compared to backward looking metrics.

Investors should also consider the risks to their portfolio in different temperature scenarios. The outcomes of these scenarios can help to determine how material the risks are to their scheme. Scenario analysis is another of the TCFD recommendations which will become mandatory for UK pension schemes, this time on a triennial basis or when investment strategy changes.

With a clear picture of climate-related objectives, investors can review what changes are required to mitigate the risks and target alignment with the Paris Agreement.

Integrate climate considerations into selection and construction

Be selective with issuers and exclusions

We believe that there can be no passive approach to either climate-investing or to CDI. Both require investors to be selective in the bonds and allocations they make to generate a high degree of resilience to market risks to deliver the cashflow requirements. Two questions we often come across in discussing issuers and sectors in climate portfolios relate to the use of green bonds and portfolio exclusions.

Does ‘climate-aware’ mean a green bond portfolio?

Many investors will understandably associate climate investing with green bonds. Green bonds, used to finance green and low-carbon technologies and projects, are part of the solution towards net zero emissions. However, we have to be selective to ensure the green bonds are fulfilling their financial- and climate-objectives. Our proprietary green bond framework aims to set a high bar to help us avoid ‘greenwashing’ – where a bond’s stated credentials don’t make the grade. In 2020, our analysts refused to pass 20% of green bonds as this burgeoning asset class expanded.

Schemes, in our view, should not be tempted to limit themselves only to green bonds or the lowest emitting issuers and sectors. This could expose them to the risk of ‘coldwashing’ – where a portfolio reports very low emissions but fails to drive wider and longer-term industry decarbonisation, one of the fundamental principles of the Paris Agreement. We believe there should be a healthy balance between green bonds and other assets that can fulfil investors’ objectives.

Should I remain invested in high-emitting companies?

Rather than exclude entire sectors, such as the oil & gas or construction industries, we believe investors should be selective to pick the climate leaders within each sector to maintain exposure to a diversified opportunity set and to finance a whole-of-market transition. This balanced approach has multiple potential benefits and can enable investors to more actively contribute to the net zero goal while also retaining the widest possible opportunity set to deliver client cashflows.

This is where our 43-person credit research team comes into play – the size and strength of the team allows us to build on the climate and wider ESG-related data we receive to fundamentally assess the strength of each issuer, their exposure to climate-related risks and their commitment to achieving a net zero world. We have deliberately chosen for our credit analysts to have full responsibility for issuer-level ESG and climate research rather than a separate team which may not appreciate company- and sector-specific nuances.

The same principle holds for our portfolio managers - we want our investment teams to be aware of and manage all the inherent risks, including climate change, to generate the best financial outcomes for our clients.

Build resilience through portfolio construction

With the objectives set and a clear focus on the role each issuer has to play, portfolio managers can seek to construct a long-term credit portfolio that offers predictable cashflows with a steadily decreasing emissions profile. Long-term credit investors should carefully consider bond maturity and undertake active engagement with issuers to bolster resilience to climate risks.

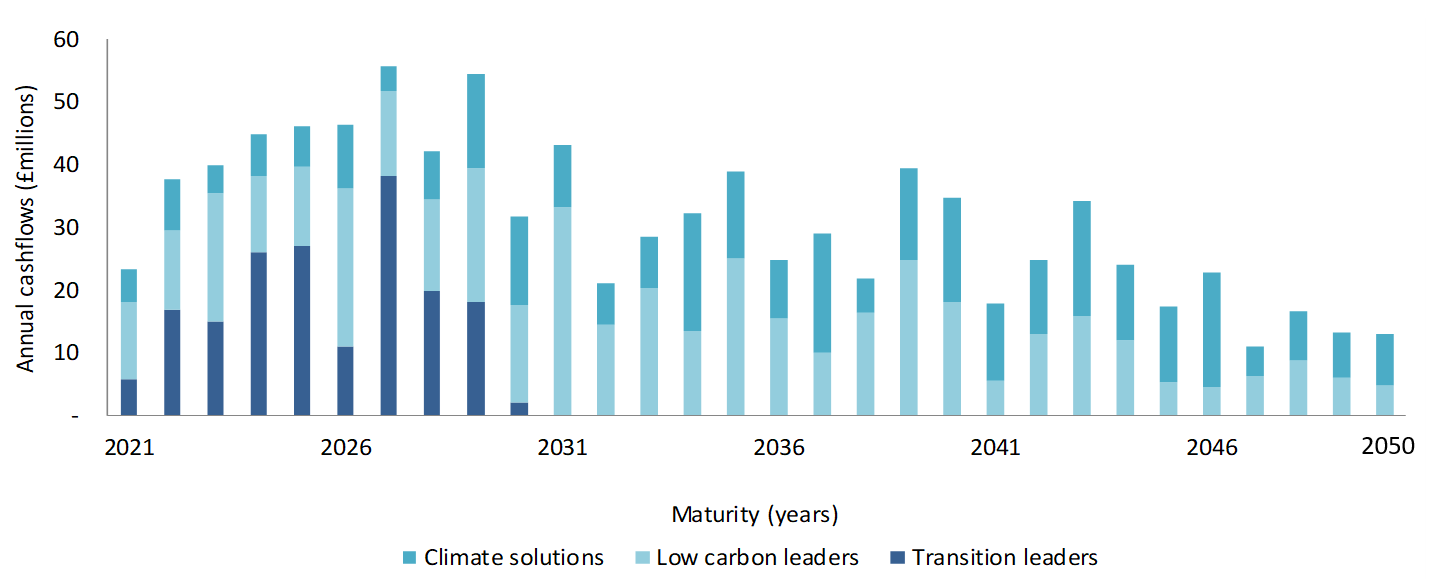

Higher-emitting companies will exhibit greater climate, and typically financial, risk than their lower-emitting counterparts and we believe these issuers should only be financed at shorter maturities. This helps our portfolio managers to manage the climate and financial risks within portfolios, avoid punitive transaction costs, and monitor the issuers against their transition pathway. By contrast, we choose to invest in issuers with lower policy, regulatory or financial risks for a much longer period. This maturity-dependent allocation, an example of which is shown in Figure 1, is particularly relevant in a long-term credit strategy as climate-risks could materialise many years after purchasing a bond.

Figure 1: Building financial and climate resilience in a long-term credit portfolio

Source: AXA IM and UBS Delta. Sample model long-term credit portfolio. For illustrative purposes only.

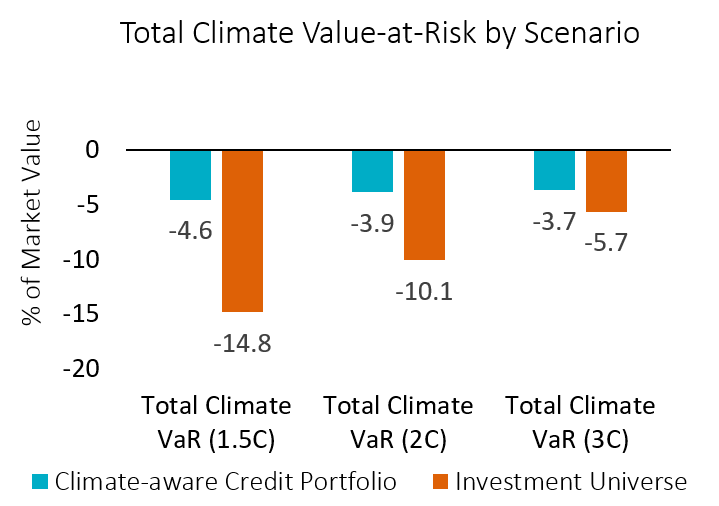

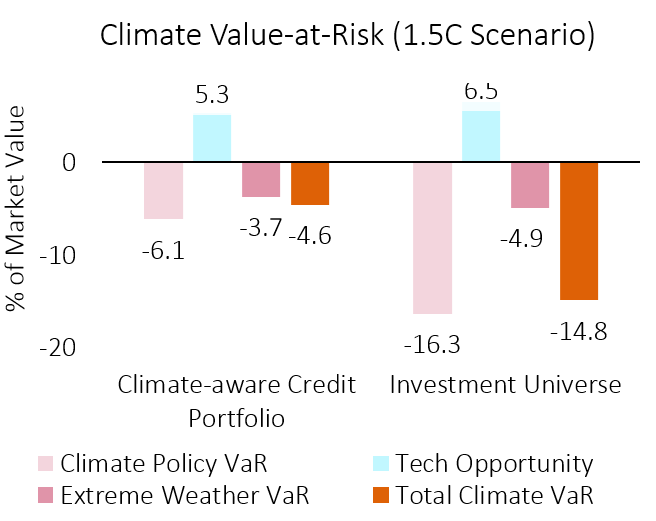

As part of the portfolio construction analysis, it is crucial to consider the amount of risk portfolios have in different temperature scenarios. Our investment team looks at climate value at risk (CVaR) as a metric to show how a portfolio could perform in a ‘cool’ 1.5°C scenario or a ‘hot’ 3°C warming scenario. Figure 2, overleaf, shows how a scheme can view the potential performance of its climate-aware credit portfolio relative to a reference universe under various temperature scenarios, as well as how the main climate factors impacting the portfolio can be assessed under a particular scenario.

The goal when creating and monitoring portfolios is to reduce the magnitude of the CVaR in absolute terms and to narrow the range of outcomes across likely scenarios – seeking to build resilience against the potential market impacts.

Figure 2: Measuring the risk – breaking down the climate impact

Source: AXA IM. For illustrative purposes only.

Engaging with companies is a key pillar to a robust climate framework. Investors can help protect their investments over the medium to long term by encouraging changes in business strategy in issues such committing to Net Zero by 2050. It is essential as a risk-monitoring and mitigation tool, particularly given the long time horizon for many pension schemes.

AXA IM have been able to encourage some of the world’s largest GHG emitters to lower their current carbon footprint and commit to robust decarbonisation plans. This supports investors in achieving their own carbon reduction plans and helps in reducing the financial risk of holding certain issuers.

We believe long-term credit strategies will have greater influence over target engagement companies due to them being long-term, stable providers of capital to companies.

Monitor how your portfolio evolves

Climate-investing is constantly evolving. Each day we see new and more ambitious commitments from companies and a greater breadth and detail in the data we receive. This information is critical to assess whether climate-aware credit portfolios are achieving their financial and climate objectives. Investors need to monitor their long-term credit portfolios through a new climate-focussed lens, acknowledging that each portfolio will follow its own path. Portfolio emissions and scenario testing are useful tools, but investors should also consider the depth and validity of the data, and how it changes over time.

Climate data coverage of the credit universe has increased sharply over recent years but there is further progress to be made. The depth of data – how much of the total emissions released by an issuer is recorded and published – has still some way to improve. One example is including in ‘Scope 3’ emissions those that are produced by companies upstream and downstream of the issuer held, rather than those of the company itself. While there are some calculation concerns with Scope 3 emissions at present, investors should expect the proportion of issuers reporting Scope 1,2 and 3 emissions to increase over time.

Investors should also witness the proportion of issuers committed to net zero emissions steadily improving. The Science-Based Targets initiative (SBTi) helps to assess whether a company’s climate targets are in line with what the latest climate science says is necessary to meet the goals of the Paris Agreement. A higher proportion of 1.5-2.0°C-aligned targets will represent a greater validity of the data used and stronger alignment to the goals of the Paris Agreement.

Investors should expect their climate-profile to consistently improve as more issuers make more ambitious commitments and our portfolio managers re-invest in bonds that try to ensure investors’ climate and financial-goals can be achieved.

Cashflow Driven Investing

CDI is changing the defined benefit pensions investment landscape

Find out moreNot for Retail distribution

This document is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This promotional communication does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee that forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Before making an investment, investors should read the relevant Prospectus and the Key Investor Information Document / scheme documents, which provide full product details including investment charges and risks. The information contained herein is not a substitute for those documents or for professional external advice.

The products or strategies discussed in this document may not be registered nor available in your jurisdiction. Please check the countries of registration with the asset manager, or on the web site https://www.axa-im.com/en/registration-map, where a fund registration map is available. In particular units of the funds may not be offered, sold or delivered to U.S. Persons within the meaning of Regulation S of the U.S. Securities Act of 1933. The tax treatment relating to the holding, acquisition or disposal of shares or units in the fund depends on each investor’s tax status or treatment and may be subject to change. Any potential investor is strongly encouraged to seek advice from its own tax advisors.

Past performance is not a guide to current or future performance, and any performance or return data displayed does not take into account commissions and costs incurred when issuing or redeeming units. The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested. Exchange-rate fluctuations may also affect the value of their investment. Due to this and the initial charge that is usually made, an investment is not usually suitable as a short term holding.

Sources:

All data sourced AXA IM, as at 31 December 2020 unless otherwise stated.

Source: AXA IM - Green bonds: How active management aims to make the most of a dynamic sector

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.