COVID-19: How the market reaction changed the Investment Grade credit landscape for UK insurers

Key Highlights

- The investment-grade credit market has been supported by central bank intervention during this crisis

- Given the backdrop of sustained, healthy spreads, we think IG credit could be attractive for insurers looking to bring risk back into portfolios

- There remains a risk of downgrades and defaults as ‘fallen angels’ reach record levels

- This emphasises the huge importance of detailed and responsive credit research, to best take advantage of this tactical opportunity

- Our teams continue to use ESG criteria to refine our investment universe, and seek out the companies that we believe will survive the crisis – and thrive in this new decade

The COVID-19 pandemic has brought upheaval to economies around the world, created unique conditions in financial markets and delivered an investment challenge for the insurance industry. Extraordinary times offer opportunities as well as risks, and a thoughtful approach to the investment grade (IG) credit universe may open a tactical window for insurers after the initial shock delivered by the virus.

The outbreak has changed the shape of our lives and prompted a monetary and fiscal response of unusual speed and scale. Central banks have, by and large, operated a “whatever-it-takes” approach, steadying the ship just when it seemed we might be overwhelmed. Soon though, companies will have to set sail alone.

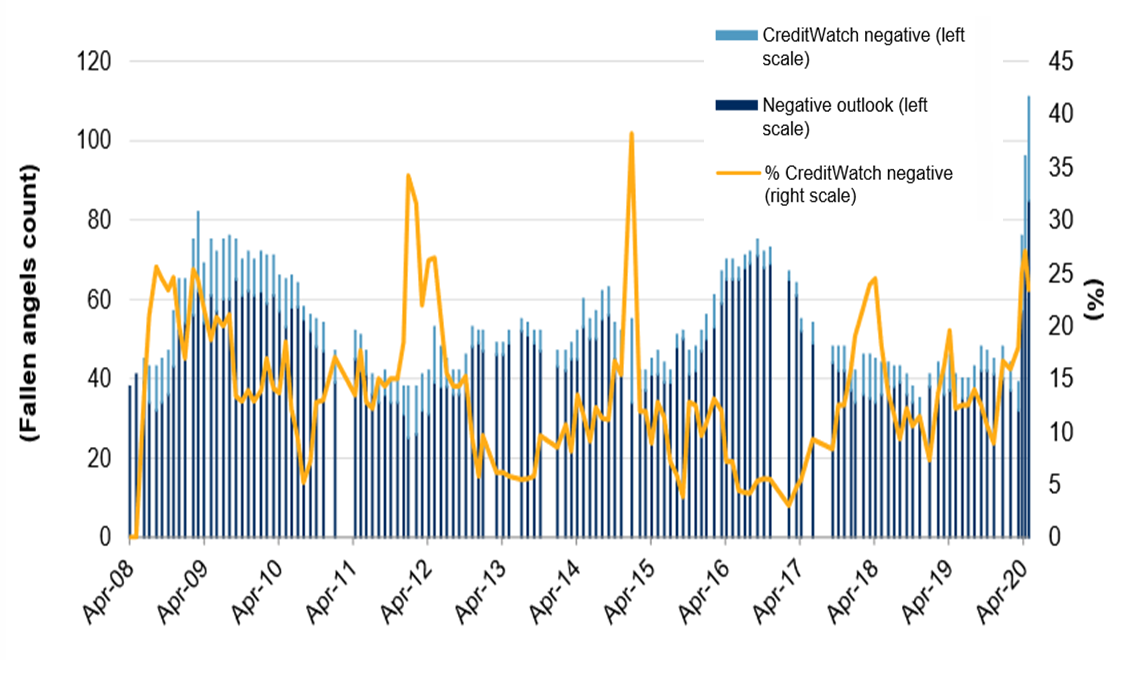

Across the ratings spectrum, defaults and downgrades will occur. In fact, we have already seen an unprecedented rate of so-called ‘fallen angels’ – corporate issuers moved down from investment grade and into the high-yield space (see chart below). It is likely too that we will see a second wave of defaults and downgrades, as ratings agencies review companies on negative watch, and as some business models succumb to the realities of these straightened times. Valuations in this environment can be hugely divergent within rating classes and can be deeply attractive. It is, in short, a moment to cheer the short-term effectiveness of the policy response to the crisis, and to venture forward with care.

Fallen angels hit record levels

Source: AXA IM, Moody's as of 18/05/2020

Recovery positions

On the business side, the outbreak will likely have an uneven impact on the insurance industry. Motoring accident claims have tumbled as lockdown left us all in our homes, leaving auto insurers with much improved loss ratios. The claims environment elsewhere will take time to properly understand – but one early estimate from Lloyd’s of London put the combined global claims and investment impact at more than $200bn1. With this in the background, and the regulatory response still a work in progress, the initial reaction on the investment side makes sense. UK insurers responded either by de-risking or by taking a wait-and-see approach.

The majority fell into the latter camp, choosing to leave their allocations mostly untouched to see how the story played out, but even here there have been defensive moves towards higher quality, as a way to mitigate rating migration risk. That remains a useful strategy to build efficient portfolios, but as the first signs of a steady recovery emerge, we believe attention should turn to the careful addition of investment risk.

Presently, we see IG credit as potentially offering one of the most attractive entry points for insurers – spreads are wider, as much as double where they were in January, but yields are similar to where they were in 2019 for many parts of the corporate bond market, including BBBs.2

Quarterly GDP numbers will be dire for the second quarter (Q2), but we expect a bounce back from Q3 – in the US and in Europe – as economies move out of lockdown. We remain aware that this will be uneven, subject to changes in the path of the virus, and in credit markets the effects will be skewed by which assets are included in central bank purchase programmes. Insurers are generally conservative and will remain so – and will have ratings downgrades uppermost in their minds. Therefore, we expect to see most take a cautious route back into credit, opting for the names and sectors receiving central bank support.

Issuers in this part of the market may not offer the most upside potential, but that backstop of central bank support means they should come with a measure of downside protection. Insurers, and especially life companies with longer-dated assets, will also be aware that the pandemic has helped to lock in the “lower-for-longer” story around interest rates. The hunt for yield isn’t ending any time soon.

Bright spots

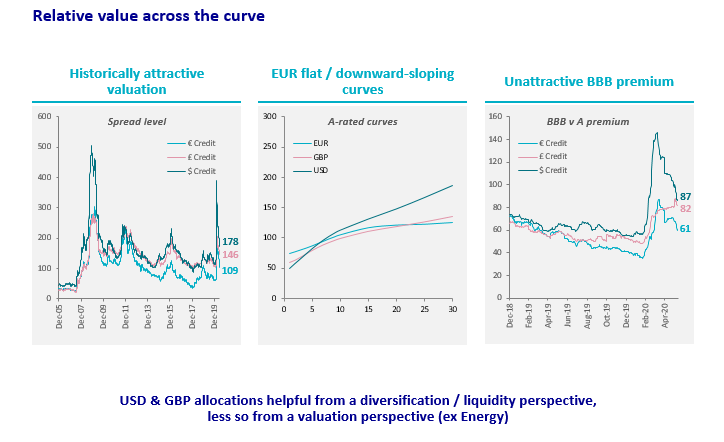

So, if an insurer has the means to boost risk – whether from new money or a need to re-risk – where should they look? First, and most simply, in euro credit spreads are double the level of last year. Looking deeper, on the back of central bank support we’ve seen heavy issuance in the US and Europe. That has triggered an aggressive curve steepening – the A-rated dollar curve is the steepest it has ever been. We believe this could be a unique opportunity to capture attractive levels of spread by adding to long-dated credit, but we don’t expect these opportunities to last. Insurance and pension scheme investors will be seeking higher yields and contractual cash flow assets.

When we think of the opportunities in IG, we think the sharp economic contraction favours defensive, non-cyclical bonds which are generally less vulnerable to earnings fragility. We think the utility sector is attractively priced alongside some select names in the auto sector. Together with some parts of the construction and transportation industries, these are areas insurers could consider to effectively redeploy capital.

Source: AXA IM 10/6/2020

But there are parts of the market we believe it would be wise to steer clear of completely. That goes for airlines, where we have seen carriers severely impacted by enforced global lockdowns, with many not expecting to return to 2019 traffic levels for three years.

Clearly, we need to contend with that sharp spike in fallen angels moving from BBB to high yield, with particular risk in the BBB- space. Even some sectors with government support are likely to suffer downgrades. UK retailer Marks & Spencer is an example of where we have already seen a fall to high yield3 and we expect other parts of the industry to follow suit.

It’s worth noting that the BBB segment is not a one-way street. Right now, it makes up about 50% of the IG credit market and cannot simply be ignored. For insurers looking to build resilience in credit portfolios, this highlights the huge value in deep analysis. Each company must be assessed with fresh eyes, guided by the distinctive characteristics of this crisis.

Deeper analysis

Our research framework, as a matter of course, looks at the economic and monetary policy outlook, valuation issues around credit risks, market behaviour analysis, and technical work on the effect of regulatory measures and supply/demand factors on fundamentals. Into this framework we have included a series of updated considerations – including, for example, closer scrutiny of supply chains and manufacturing footprints that may become more localised due to the crisis.

The daily process of credit research now carries a heightened sensitivity to the pace and scale of changing conditions. As such, we closely watch government briefings for subtle changes in the nature and scope of support for some companies, as well as more lingering restrictions for others. There are many examples of rules which impacted one sector over another, or which have favoured one part of a sector. This is crucial to understanding the short-term impact on company cashflows, as is a full appreciation of how companies will fare in a 90% economy that is firing on fewer cylinders.

Once urgent liquidity concerns have been addressed, our credit analysts quickly turn their attention to earnings, cash flows and leverage. While government-backed loans and bond purchases from central banks should help alleviate immediate pressure and hopefully ensure the survival of sustainable businesses, they will not prevent the unavoidable fallout from the crisis on corporate leverage as measured by debt-to-EBITDA ratios4. For companies with sizeable underfunded pension obligations, leverage metrics could be further stretched as a result of low discount rates and reduced asset values

Sustainable futures for insurance investment

The importance of environmental, social and governance (ESG) criteria, meanwhile, can be heightened in difficult moments like this. In the midst of market stress, ESG factors help us to identify where the key risks rest over the longer term and allow us to further refine the universe of credits that we think will not only bridge to the other side of this crisis, but which are positioned to thrive as the decade rolls on. Insurance companies (likewise defined benefit pension funds) with long-term time horizons need the confidence to know that the allocations they hold are secure and predictable, and ESG is central to helping ensure this level of sustainability.

There are also long-term trends within responsible investment that we think will be accelerated post-crisis and could provide opportunities. These include renewable energy, a clean economy and sustainable transport, all of which will open the door for more financing around responsible business models. At AXA IM, we have been very active in the successful Green Bonds market, and we are seeking to take a leadership role in the growth of Covid bonds – designed to help companies fund emergency measures – and in the new Transition Bonds, which finance projects that help drive carbon-intensive businesses towards a eco-friendlier future.

These considerations will regain the market’s attention as we move past this crisis, but they still inform our approach as the path of the pandemic unfolds and help to reveal the best long-term opportunities right now. And that underscores the key to capturing the value in credit in this moment. It is all about careful initial credit selection, informed by deep bottom-up and fundamental analysis, while keeping a weather eye on the horizon.

- Financial Times, 14 May 2020. https://www.ft.com/content/51d32286-5264-4c93-80c3-3d0b0fd4558a

- Source: ICE BofA Global Corporate Index

- On 26 March, S&P downgraded M&S’ long-term sterling and foreign-currency debt from BBB-, the lowest level of investment grade, to BB+ which is regarded as sub-investment grade or ‘junk’. Fitch followed suit on 9 April downgrading M&S’ senior unsecured debt rating to BB+ and its short-term ratings to B from F3.

- The main aim of this ratio is to reflect the cash available with the company to pay back its debts.

Not for Retail distribution

This document is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document. Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ. In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

Risk warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.