Time to think about the downside

Never be short duration for too long, be wary of risk assets when they are too expensive, always assume the England football team loses. Those three assumptions have served us pretty well over the years and into 2021, but before we get to bond land, congratulations to Italy on their hard-fought victory.

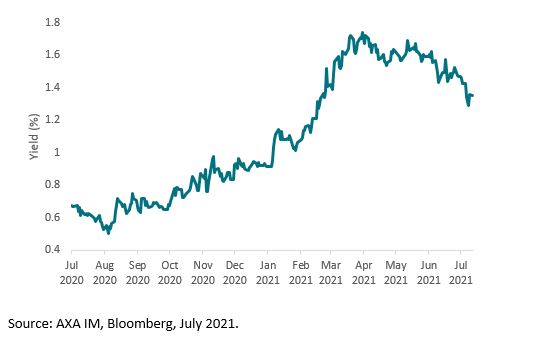

Duration extends its Q2 run

There is a big rally going on in government bonds. It is now more than three months since bond yields peaked at 1.74% in US Treasuries and, since then, we have seen a 50 basis point rally, which has accelerated recently (as of mid-July). There is much debate about what is driving this move: some argue that it is very technical driven with negative or short duration investors being squeezed and CTA accounts (derivative and momentum) potentially driving the market lower in yield as they close their short positions.

From a fundamental perspective, some argue that it's the end of the reflation trade and the market is now pricing in a less perfect growth and inflation outlook. From a valuation perspective, it's difficult to argue that investors are driving markets lower in yield because they see the market as cheap but, with the benefit of hindsight, clearly 1.75% was very cheap!

As ever, if you mix all of those views together – a combination of what we would call Macro, Valuation, Sentiment and Technical factors – we conclude there are more buyers than sellers and should move with the markets. We have been adding duration over recent months and are now benefiting from the underlying move.

Chart 1: Ten-year Treasury yields have fallen back over the second quarter

Time for caution on credit?

Credit spreads have benefitted year-to-date from strong demand, improving fundamentals and lower default expectations. On most metrics, credit yields and spreads are looking rich but, much like government bond yields, it is entirely possible that yields and spreads can stay expensive or become even more expensive, given the various supporting factors.

That said, credit is certainly back to pre-Covid valuations and is more expensive in places than post the Global Financial Crisis. In certain parts of the market, it is more expensive than ever.

We have stopped adding to credit risk and in some markets have reduced exposure, moved to short duration, and preferred investment grade over high yield. We are looking to hedge other parts through the usual use of duration or credit default swaps. We suspect that volatility will be a buying opportunity for many investors looking for some cheaper entry points into credit, but maybe over the quiet summer weeks and months the market gives back some of the 2021 gains.

And as for the football?

Despite the euphoria and subsequent disappointment on Sunday, England fans are still proud of the team – after all, a final appearance does not come round very often. You might not have picked England or duration to perform three months ago, but it is also worth listening to the contrarian case!

What is unconstrained fixed income ?

This provides the potential flexibility to capitalise on opportunities across the fixed income spectrum as and when they arise

FIND OUT MOREDisclaimer

This promotional communication does not constitute on the part of AXA Investment Managers a solicitation or investment, legal or tax advice. This material does not contain sufficient information to support an investment decision.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Before making an investment, investors should read the relevant Prospectus and the Key Investor Information Document / scheme documents, which provide full product details including investment charges and risks. The information contained herein is not a substitute for those documents or for professional external advice.

The products or strategies discussed in this document may not be registered nor available in your jurisdiction. Please check the countries of registration with the asset manager, or on the web site https://www.axa-im.com/en/registration-map, where a fund registration map is available. In particular units of the funds may not be offered, sold or delivered to U.S. Persons within the meaning of Regulation S of the U.S. Securities Act of 1933. The tax treatment relating to the holding, acquisition or disposal of shares or units in the fund depends on each investor’s tax status or treatment and may be subject to change. Any potential investor is strongly encouraged to seek advice from its own tax advisors.

Past performance is not a guide to current or future performance, and any performance or return data displayed does not take into account commissions and costs incurred when issuing or redeeming units. References to league tables and awards are not an indicator of future performance or places in league tables or awards and should not be construed as an endorsement of any AXA IM company or their products or services. Please refer to the websites of the sponsors/issuers for information regarding the criteria on which the awards/ratings are based. The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested. Exchange-rate fluctuations may also affect the value of their investment. Due to this and the initial charge that is usually made, an investment is not usually suitable as a short term holding.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.