The journey and the destination

- 01 April 2022 (5 min read)

Nowhere to hide

So far, 2022 has brought plenty for investors to weigh-up when thinking of how to position portfolios. In particular, the investment implications of the Russia/Ukraine conflict are complex. Early in the crisis, we believed it was logical to assume the conflict could have a negative effect on growth, particularly in Europe, which could push investors towards safe-havens.

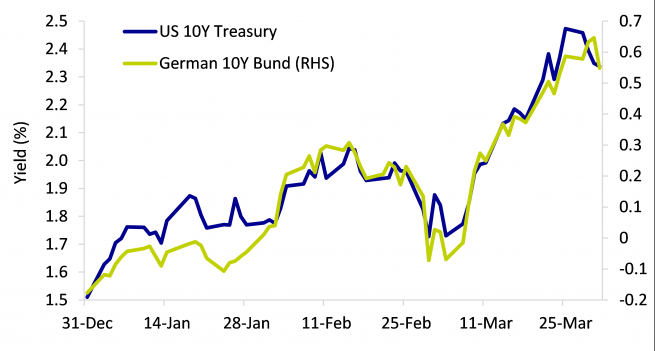

Looking at the below chart, this indeed proved to be the case as US 10-year treasuries rallied from 2.0% yield down to 1.7% into early March. However, this rally was short-lived as markets instead began to focus on the other direct impact from Russia/Ukraine – namely on exacerbating the rise in energy prices and the inflationary effect which that would cause – particularly in Europe. This caused government bond yields to sharply increase again throughout March, and we sit today with yield levels at highs not seen since before the pandemic in 2019.

As a result of these moves, markets are once again focusing on the actions that central banks will take to tackle inflation. The Fed hiked its base rate by 25bps a couple of weeks ago, but it’s what happens next that matters. Markets are currently pricing in future hikes by the Fed more aggressively than the Fed’s own officials are via its dot plot, which was not previously the case at the Fed’s December meeting. There is an expectation that the current dot plot will shift more hawkish, suggesting that the Fed will continue to hike – possibly as much as seven times this year, despite the threat to the recovery that this poses by tightening conditions too much.

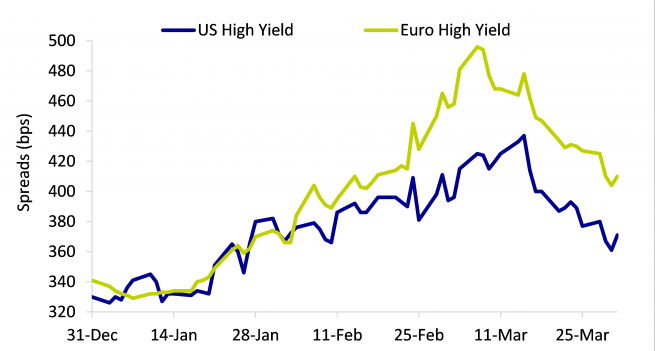

At the same time, high yield spreads have widened both in the US and Europe through much of the first quarter, despite rallying back in the last two weeks of March. Euro high yield has underperformed its US equivalent, as markets become jittery over what the Russia/Ukraine conflict means for growth prospects particularly in the European area:

For much of the quarter, this has created something of a ‘perfect storm’ market environment where there is nowhere to hide. In phases such as this, it is more important than ever for investors to keep focus on long-term goals and how to construct and manage portfolios to provide the best chance of achieving those goals.

An unconstrained approach

In our view, the main goal of an unconstrained, total return fixed income strategy is to deliver attractive risk-adjusted returns through the market cycle. These types of approaches recognise that fixed income is not a single asset class and doesn’t just mean ‘low risk, low return’. By using flexibility to take advantage of opportunities across the whole fixed income spectrum, an unconstrained strategy has the potential to use fixed income assets to provide a range of outcomes – capital protection, income, growth – by aiming to be in the right part of the market, at the right time.

At AXA IM, we have developed an unconstrained fixed income strategy around an approach which divides the fixed income universe into three buckets: ‘Defensive’, ‘Intermediate’ and ‘Aggressive’. This rests on the notion of low to negative correlation between the main fixed income risk factors: interest rate risk and credit risk, which presents the opportunity to actively manage the balance between these according to prevailing economic and market conditions and valuations. Inevitably, there will be periods where these correlations break down and all asset classes move in the same direction at once. We have observed these in the past such as the 2013 / 2015 tantrums and briefly during the March 2020 crisis – and we are in one such period again in 2022.

Long-only total return strategies cannot guarantee positive returns in all environments and will invariably see drawdowns when all asset classes fall in value. Instead, the approach is to use flexibility, diversification and active management to mitigate some volatility without losing focus on the longer-term goals.

Conviction with humility

The benefit of an unconstrained strategy is the ability to be conviction-led. This means, building a portfolio of best ideas aligned with the long-term objectives, without having to try and aggressively time markets. We strongly believe staying true to our convictions is ultimately far more likely to be in the best interests of investors in our strategy versus trying to shelter the portfolio from all volatility in the short-term.

This is because we distinguish between genuine risk and volatility. The former considers the destination, while the latter describes the journey. The broad definition of investment risk is the risk of permanent capital loss when the time comes to close an investment. Holding low volatility assets feels more comfortable on the ‘journey’ towards long-term investment goals. But it does necessarily make those goals more likely to be achieved. What matters is the time horizon of the investment and an investor’s tolerance for volatility along the way.

For investors who can afford to ride out short-term fluctuations, volatility can even be helpful rather than harmful in terms of periodically presenting opportunities to buy more of an asset you have a positive conviction on, at a cheaper price. Conversely, it is important not to allow short-term volatility to distract from those convictions (provided the investment thesis still stands) and turn volatility into genuine risk by panic-selling and thus realising permanent loss on the investment.

That is not to say that we ignore the investor experience. We understand the importance of balancing our belief in our convictions with having the humility to recognise when we may need to trim positions to deliver the experience investors expect from their unconstrained fixed income portfolio.

For example, so far this year we have been active on our duration exposure given our belief that market pricing for rate hikes appears to be too aggressive – adding duration when government bonds offered more compelling value, but reducing it when focus on inflation and rate hikes intensified. Again, this comes down to conviction – in this case that core government bond yields are nearing what we would determine ‘fair value’ and are starting to present an attractive buying opportunity. Furthermore, in light of the risks posed by both the current war in Ukraine and the potential for that to escalate beyond Ukraine’s borders, our natural instinct has been to own more safe-haven government bonds rather than risk assets. However, when we have felt that market momentum is strongly behind higher yields, we haven’t hesitated to reduce some of that duration risk to mitigate short-term volatility.

Where do we go from here?

Moving forward, despite market movements year-to-date, we still believe the risk factors of different components of fixed income (interest rate vs credit risk) provide enough diversification and low correlation over reasonable time periods to deliver attractive risk-adjusted returns. Where the historic correlation is brought into question, we would argue that the rates / credit diversification is clearly not perfect, but still better than many alternatives that we see suggested.

We expect 2022 to remain volatile due to the Russia/Ukraine conflict, as well as the expected shift in monetary conditions and the easing of asset purchasing programmes by central banks. A lot of this depends on what happens to inflation. Without question we are seeing very high inflation prints and this could well continue over the coming months given the reliance by the West on Russia for oil and natural gas supplies – in many cases reaching the highest inflation we’ve seen in many decades. However, our analysis concludes with the view that elevated inflation will not be permanent and is currently present for well documented and fairly understandable reasons – albeit it has been higher and has lasted for longer than we expected.

The big question for central banks in 2022 is how they approach the delicate balancing act of tackling inflation to bring it down to some level of ‘normalisation’ (whatever that means), which will naturally involve some degree of tightening monetary conditions, whilst also ensuring that the recovery is not disrupted too much. Looming in the background is the significant threat of a recession, highlighted by the recent inversion of the US 2s10s curve, which central banks will be keen to avoid.

In this environment, our conviction in a flexible and diversified approach to global fixed income investing is as strong as when we first launched the strategy 10 years ago. As suggested previously, current market weakness will at some point create attractive buying opportunities for bond investors, which makes us relatively optimistic that, albeit painful in the short-term, we should not rule out 2022 from a total return perspective just yet.

Our focus long-term focus remains constructing a portfolio which is structurally diversified, holds liquid fixed income assets and applies careful risk budgeting, as well as having the agility to respond as markets move.

What is unconstrained fixed income?

Find out more about global strategic bonds and total return investing

Learn moreVisit our fund centre

Visit our fund centre to find out more about our strategy.

This provides the potential flexibility to capitalise on opportunities across the fixed income spectrum as and when they arise.

View fundsDisclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.