Inflation: Real interest rates should continue to decrease over the course of 2021

- 20 November 2020 (5 min read)

Key points

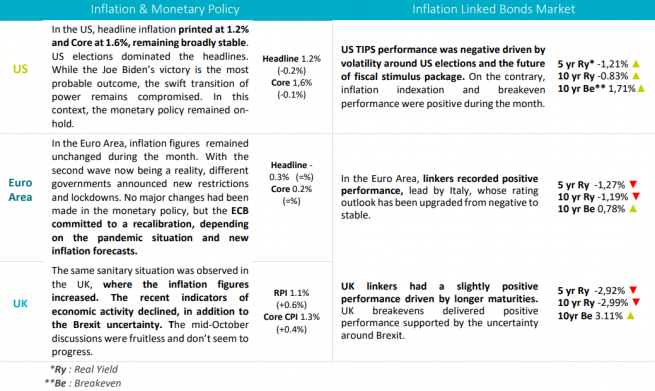

- In the US, marked by turbulent power transition, pandemic remains concerning and the macro situation will not change much before mid-2021, despite the good news around the vaccine.

- In the Euro Area, with the second wave now being a reality, different governments announced new restrictions and lockdowns.

- In the UK, while the pandemic worsened mirroring the Euro Area situation, uncertainty around Brexit continues and discussions are at a standstill.

What’s happening?

Portfolio positioning and performance

| Key Strategies | Performance | |

| Real Yields | During the month, we kept a low risk profile in the context of volatility around US Elections. We closed our short real duration position in the Euro Area and continuing to favor Australian linkers and front end US TIPS. | + Long real duration position in Australia. - Long duration in front end US TIPS |

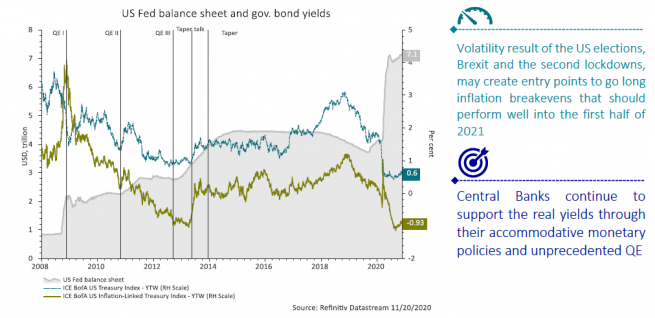

| Breakevens | During the month, we icreased our short breakeven exposure in the Euro Area, of which we took profits into month end. We are looking into opprtunities to go long breakevens that should perform well into the first half of 2021 | + Short breakeven position in the Euro Area |

Outlook

United States

The Federal Reserve & the US Treasury continue their aggressive series of non-conventional measures to support the economy. We believe that US real yields should continue to move lower over the coming months and favour long duration positions.

Euro Area

The new increasing Covid-19 cases and more restrictive measures throughout Europe compromises the economic rebound. European inflation has gone in negative territory and is expected to remain quite low in the coming months.

United Kingdom

In the UK, leading indicators declined adding to the Brexit uncertainty. Nevertheless, we expect the Brexit developments to be back on the radar and to weigh on Real Yields and Breakevens.

No assurance can be given that the Inflation strategy will be successful. Investors can lose some or all of their capital invested. The Inflation strategy subject to risks including credit risk, liquidity risk, derivatives and leverage risk, contingent convertible bonds risk.

Not for Retail distribution

This document is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document. Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ. In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.