Inflation - Surprising rebound in inflation in July

- 01 September 2020 (5 min read)

Key points

- Headline inflation surprised to the upside across the main markets

- The ECB kept its monetary policy unchanged in July, judging the euro area to be in a "good shape".

- The Bank of England voted unanimously for a QE target of GBP 745bn

What’s happening?

| Inflation & Monetary Policy | Inflation Linked Bonds Market | |||

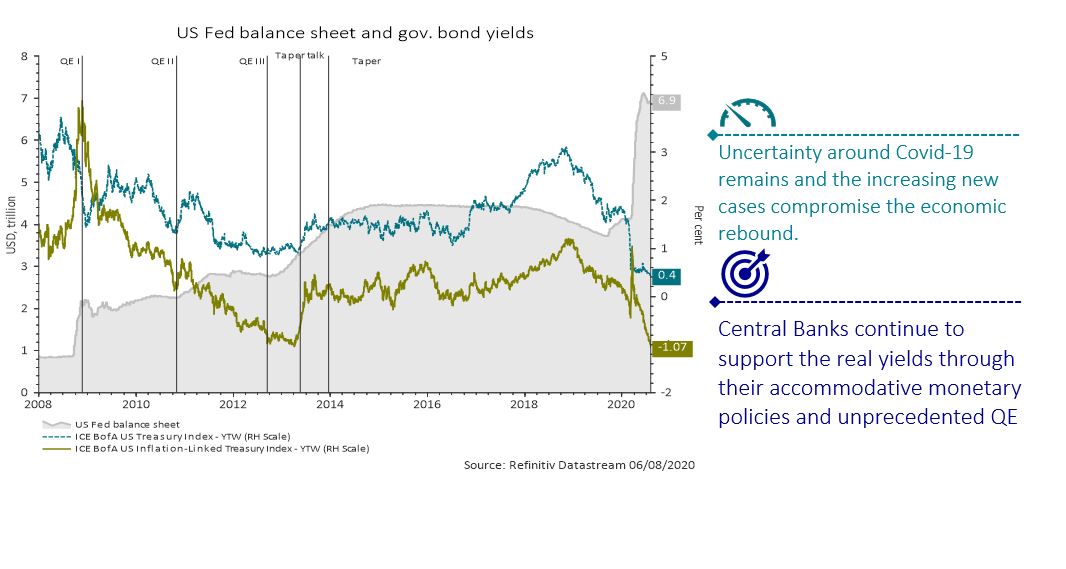

| US | In the US, headline inflation surprised to the upside at 0,6%. While the pandemic continues to weigh on the economic rebound, the Fed keeps its accommodative policy with the stable QE rhythm. |

Headline 0,6% (+0,5%) |

US TIPS performance was positive during the month. Real yields declined, with the longend out-performing. Breakevens continued their upward trend supported by leading economic indicators. | 5 yr Ry* -1,23% 10 yr Ry -1,03% 10 yr Be** 1,55% |

| Euro Area | In the Euro Area, the inflation figures were also positive. After the strong measures in June, the ECB kept its monetary policy unchanged in July, judging the euro area to be in a "good shape". | Headline 0.4% (+0,1%) Core 1.2% (+0,4%) |

In the Euro Area, linkers had a positive performance as well, Italian linkers, once again, were the best performers. Breakeven performance was also positive across all markets. | 5 yr Ry -1,18% 10 yr Ry -1,10% 10 yr Be 0,86% |

| UK | K In the UK, inflation rebounded slightly with the Core CPI coming at 1.4%. The Bank of England voted unanimously for a QE target of GBP 745bn and maintained the monetary policy stable. | RPI 1,1% (+0,1%) Core CPI 1,4% (+0.2%) |

UK linkers posted a positive performance, but it remained week with front end underperforming. | 5 yr Ry -2,77% 10 yr Ry -2,99% 10yr Be 2.99% |

*Ry : Real Yield

**Be : Breakeven

Portfolio positioning and performance

| Key Strategies | Performance | |

| Real Yields | During the month, we fully took profits from our long duration positions in the US and the Euro Area and added exposure to the front end of the Euro linkers curve, particularly France and Germany. We believe that short term bonds offered attractive valuations given inflation forecasts for the years to come. We also added a long duration position to Australian linkers. | + Overweight of short-term linkers in the Euro Area + Long real duration position in Australia. |

| Breakevens | At the end of July, we entered a tactical short breakeven position in the Euro Area and the US. |

Outlook

United States

The Federal Reserve & the US Treasury continue their aggressive series of nonconventional measures to support the economy. We believe that US real yields should continue to move lower over the coming months and favour long duration positions.

Euro Area

With the easing of lockdown measures the economy activity has started to show some signs of recovery. We see an opportunity in adding long positions in Core € Area real yields in portfolios.

United Kingdom

The UK linker market continues to trade rich versus other markets despite the Covid-19 shock. However, the return of “Brexit” headlines and ongoing support from Bank of England might bring support to the market even at these rich levels and we remain cautious in this regard.

No assurance can be given that the Inflation strategy will be successful. Investors can lose some or all of their capital invested. The Inflation strategy subject to risks including credit risk, liquidity risk, derivatives and leverage risk, contingent convertible bonds risk.

Not for Retail distribution

This document is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document. Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ. In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.