Thematic equities in focus - July

- 24 July 2020 (5 min read)

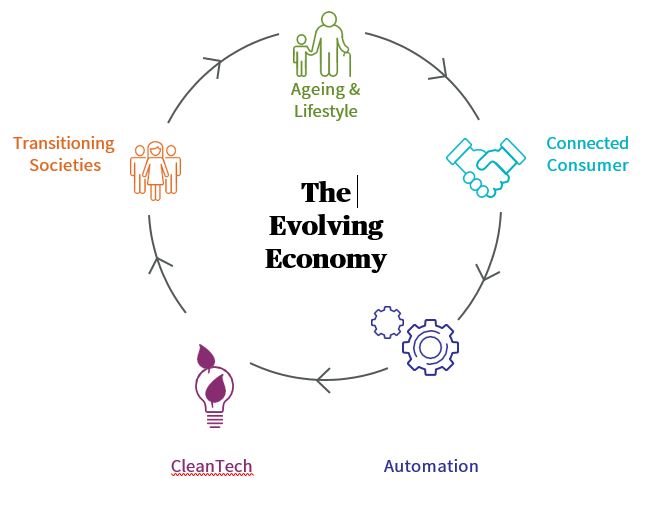

Changes create norms

Whilst the global economy has been significantly impacted by the COVID crisis and will take some time to recover, the macroeconomic conditions in major markets have improved in Q2 2020 with an immediate post-crisis monetary and fiscal support. The global equity market has viewed this positively and rebounded significantly over the same period. Whilst the near future remains cloudy – with countries gradually re-opening when other remain impacted by many cases – there is one element that no one can deny: our everyday life has changed. These changes are gradually leading the path towards new norms to which many companies of our 5 identified long-term secular growth themes are exposed:

Most readers of this article have directly or indirectly experienced a “Working-From-Home” (WFH) situation. Although the technological and operational setup has been quite new for many employees, remote working does not affect productivity and it appears that companies are starting to rethink their traditional “5 working days model” in the office. Some companies have already taken measures by extending working from home to their staff until the end of year – and few have even pronounced the word ‘forever’. It is clear that investments into WFH were strong over the last quarter and this is where our Connected Consumer theme has been a clear beneficiary with several companies enabling and securing remote work. This includes software tools for collaboration and project management, videoconference, customer communication or cybersecurity. Whilst the private and public sectors have reactively invested during the crisis, we believe that the “WFH model” is still in its infancy and expect more investments in this area over the coming years.

Companies within our Automation theme which provide robotic and automated solutions to various industries have seen a strong demand and behaved positively over the quarter. Conversely, we have seen a lower level of activity that in a normal environment on elective procedures – like robotic surgery for spinal issues – since most hospitals had to prioritize and cope with COVID related cases. However, we are reassured that the vast majority of elective surgeries are not cancelled, they’re just deferred – the patients will still need surgery/treatment in due course – and thus demand is likely to rebound strongly when it is safe to perform these procedures. As some healthcare names have been particularly hit in H1 2020, we have started to increase our investment in companies that we feel are starting to trade at substantial discounts to what we believe their earnings potential is in normalised economic conditions.

Similarly, we believe that people’s view on health and treatment will evolve in light of the pandemic, with greater acceptance of new technologies, contributing to improved life expectancy and placing our Ageing & Lifestyle companies at the forefront. Beyond keeping health, it is also clear that people have searched to maintain a decent wellbeing. This obviously includes ‘home’ fitness activities but also beauty, wellness and even pet ownership. Pet ownership is rising among older people and some studies have found it can be emotionally beneficial and improve mental health. Pet care is also known as a ’recession-proof industry’, no matter what’s happening in the economy, people continue to buy quality for their fully-fledged family member. Whilst the over 60 age group is dominating consumption in this industry with a growing demand for premium care products, pet ownership is also increasing among younger generations.

Elsewhere, the COVID is not postponing or slowing down the pattern towards a cleaner planet. Changes in consumer behaviour is disrupting parts of the CleanTech theme including the recycling and waste reduction area. The highest quality parts of this sector have responded rapidly, engaging with customers and adjusting their cost bases. Hygiene considerations have also increased the proportion of single use packaging in many settings. Whilst the drop in overall out of home consumption has more than offset this in the near term, we view the return to single use packaging as an opportunity for those businesses able to create more readily recyclable single use items and to recycle them efficiently. We note an increased emphasis in Europe on the importance of shifting towards a circular economy, with single use plastics a particular focus. Progress such as the introduction of a plastic bag tax in Japan from July highlights the increasingly global nature of this attention.

In Transitioning Societies theme, the activities were mostly dominated by the trajectory of the virus with data flow around cases. Whilst many countries are still on the fight against infection cases, priority remains focused on basic needs such as food or healthcare access. With the lockdown constraining the Emerging Middle-class mobility, we’ve seen an increasing use of digital channels for on-demand food, groceries delivery or healthcare diagnostics.

It is likely that a number of the themes of the Evolving Economy will be the long-term beneficiaries of a shift in behavior, which has accelerated as a result of the current crisis. However, it’s not all about being exposed to the right theme, it’s also about selecting the right winners within a panel of many and varied companies. We believe a focus on quality companies with strong balance sheets, strong margins and cash flow generation are now more critical than ever. We retain the view that high quality management teams, operating businesses with a sustainable competitive advantage in their markets and with the benefit of secular tailwinds are best placed to weather the current storm. With this aim in mind, a fundamental stock picking with a deep knowledge of companies is paramount.

Connected Consumer theme

By 2021 the economic cost of cybercrime is set to reach $6tn or approximately 7% of global GDP – bigger than the cost of climate change1

Zscaler, Cloud-based security software

Zscaler provides a cloud-based platform encompassing several security services (web security, firewalls, sandboxing, antivirus) which allow businesses to create fast, secure connections between users and applications, regardless of device, location, or network. Performance and security on the cloud are key concerns for work-from-home setups, and Zscaler has seen an acceleration in cloud security deployments to address those needs.

Internet Security with Zscaler App

Automation theme

From 2020-2027, the global spinal surgical robot market is projected to grow at CAGR 14.2%2

Nuvasive, Spinal Robotics specialist

Nuvasive focuses on developing minimally-disruptive surgical products and procedurally-integrated solutions for the spine surgery. Less invasive spine surgery is associated with better patient care as well as faster recovery times and shorter hospital stays. The company also produces software systems for surgical planning and monitoring, access instruments, and implantable hardware.

Minimally Invasive Spine Surgery (left & middle pictures) - integrated technology platform (right picture)

Ageing & Lifestyle theme

90% of dog owners and 86%3 of cat owners consider their pets as important members of their family

Zoetis, Animal health business

Zoetis is a global leader in the discovery, development, manufacture and commercialization of animal health medicines, vaccines, and diagnostic products with a focus on both livestock and companion animals. It commercialises products across seven major product categories: vaccines, anti-infectives, parasiticides, other pharmaceutical products, dermatology, medicated feed additives and animal health diagnostics.

Pet care is known as a “recession-proof industry’, no matter what’s happening in the economy, people continue to buy for their ‘family member’

CleanTech theme

Urbanisation, population and income growth could see waste from cities grow 70% by 20254 .

Waste Connections, Integrated waste services company

Waste Connections is a Canadian integrated solid waste services company that provides non-hazardous waste collection, transfer, disposal and recycling services. The company is the 3rd largest waste management company in North America (US and Canada). With the United States being the largest consumer market in the world, providing an efficient waste management remains a strong priority.

Waste Connections recycling process

Transitioning Societies theme

With global consumption forecast to double from 2013 to 2025 and half this growth coming from emerging markets5 there is a large opportunity for brands in EM.

Foshan Haitian Flavouring and Food, Condiment specialist

Foshan Haitian is a China-based company producing and distributing seasonings. The company is the largest producer of soy sauce for Chinese cuisine. Soy sauce represents one of the most important condiment consumption in China and has seen an increasing demand from local consumer, food retail chains, food manufacturers, and restaurants. Globally, rising popularity of Asian cuisines is also driving up the product demand. Unsurprisingly, demand has been very resilient for Foshan Haitian’s products through the COVID crisis.

Foshan Haitian soy sauces encompassing several product range

- Qm9GQU0g4oCTIFRyYW5zZm9ybWluZyBXb3JsZDogdGhlIDIwMjBzIOKAkyBOb3ZlbWJlciAyMDE5LCBDeWJlcnNlY3VyaXR5IFZlbnR1cmUu

- VmVyaWZpZWQgTWFya2V0IFJlc2VhcmNoLCAyMDE5Lg==

- Q3JlZGl0IFN1aXNzZSDigJhBbmltYWwgSGVhbHRoIFN1cGx5IENoYWluIEJ1bGwvQmVhcuKAmSwgQVBQQSwgR2ZrIC0gRGVjZW1iZXIgMjAxOS4=

- Qm9GQU0g4oCTIFRha2luZyBvdXQgdGhlIFRyYXNoIOKAkyBHbG9iYWwgV2FzdGUgUHJpbWVyLCBKdW5lIDIwMTgu

- TWNLaW5zZXkgJmFtcDsgQ29tcGFueSwg4oCcR2xvYmFsIGdyb3d0aCwgbG9jYWwgcm9vdHM6IFRoZSBzaGlmdCB0b3dhcmQgZW1lcmdpbmcgbWFya2V0cyzigJ0gQXVndXN0IDIwMTc=

Not for Retail distribution

This document is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document. Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ. In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.