Why might China’s property dollar bonds remain a resilient yield generator?

- 07 August 2020 (10 min read)

The offshore US dollar bond market for China’s property developers has long been an area that many view with fascination. Its vast scale, the complexity behind how it was developed and its sensitivity to regulatory changes can be both appetising and concerning. Here we examine how this market came about - and the main reasons why we think it will continue to offer potential yield opportunities to fixed income investors in Asia.

What makes the China offshore dollar market unique?

The foreign currency offshore market is where Chinese companies utilise the US dollar (almost exclusively, but also occasionally the Hong Kong dollar and euro) bond markets for their funding needs, mostly when their funding channels are restricted by domestic regulations. This market, though secondary in size to the renminbi onshore market, is an important part of the Chinese fixed income universe. Usually offering a pick-up in yields over onshore bonds, Chinese offshore dollar bonds are often of interest to Asia high yield corporate bond investors.

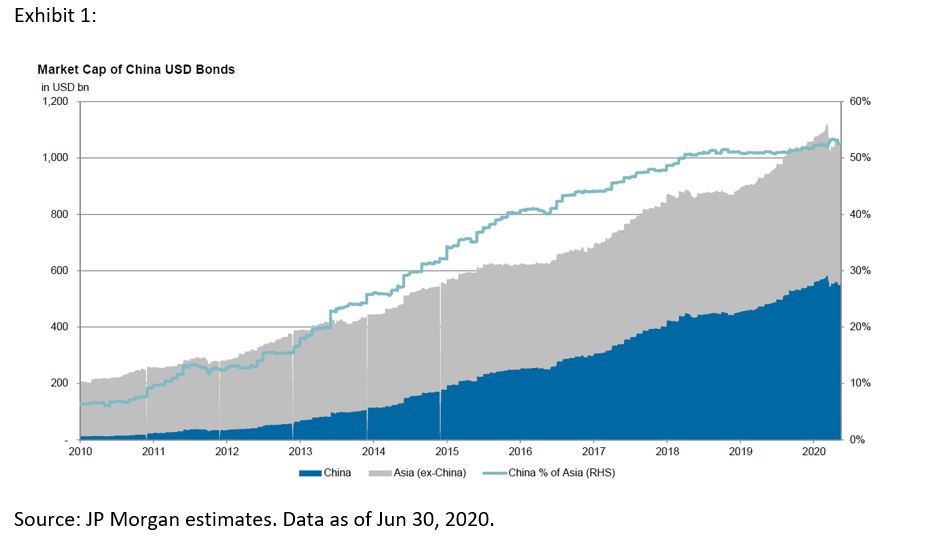

Consistently accounting for over 50% of Asia’s dollar credit market since 2018, China’s outstanding US dollar bonds have grown to an estimated $560bn as of the first half of 2020.1 China’s central and local state-owned enterprises, local government financing vehicles (LGFVs), and property developers have been aggressive users of the offshore financing channel.

On the supply side, $194bn was raised by Chinese issuers in the offshore market in 2019, accounting for 64% of the total supply of Asian credit. The market surged in 2017 as China tightened its policies on onshore bond issuance (mostly to property developers and LGFVs).

Chinese developers demonstrated resilience through COVID-19

As of end of June 2020, China’s high yield corporate bonds (excluding financials) account for 71% of Asia’s high yield market, while China property developers account for 72% of Chinese high yield bonds in the offshore dollar market2 .

The Chinese property sector has shown resilience and is one of the sectors that have largely recovered since the height of the coronavirus pandemic after global liquidity eased and investor sentiment improved. Differing from high yield sectors in other regions, China’s property sector benefits from a few factors.

For one, it’s backed by a strong onshore banking system and bond market. We have witnessed domestic regulators using their policy flexibility to relax regulation governing onshore bonds in the first half of the year, granting onshore funding sources to Chinese developers while the offshore was effectively closed for them.

For another, China seemed to have rapidly taken control of the COVID-19 outbreak and some parts of the country’s economy have staged a V-shaped recovery since March 2020. The resumption of business, coupled with lowered funding costs, has benefited developers and ensured property sales to onshore home buyers have begun to return to normal.

A very Chinese dream

To put the world’s biggest housing market into perspective, it’s necessary to understand the significance of home purchases in Chinese culture. An aspiration deeply rooted in most Chinese people, home ownership symbolises ultimate success, the mark of adulthood, an essential for marriage, and ownership of one’s financial destiny. Chinese citizens devote as much as 74% of their savings to housing, compared to 35% in the US.3 As property prices remain resilient, housing is also perceived in China as the best value-preserving investment, a belief that was reinforced by the 2015 China stock market crash.

Fundamentals are solid but vary among regions

The sector has benefited from short-term policy easing and navigated through the worst impact of the pandemic so far. At the same time, we believe that longer-term secular trends of urbanisation and income growth, which have been propelling the Chinese property sector, should continue to provide support as the economy recovers.

China’s urbanisation rate was 60.6% at the end of 20194 , only higher than India and Indonesia among G20 countries, and it might reach 70% by 20305 . That means about 150 million rural residents will move to towns in the next 10 years, which will keep fueling demand for property. Though the urbanisation rate growth has moderated in China in recent years, compared to developed economies, it’s still on a relatively fast track and presents considerable investment opportunities.

Location, location, location

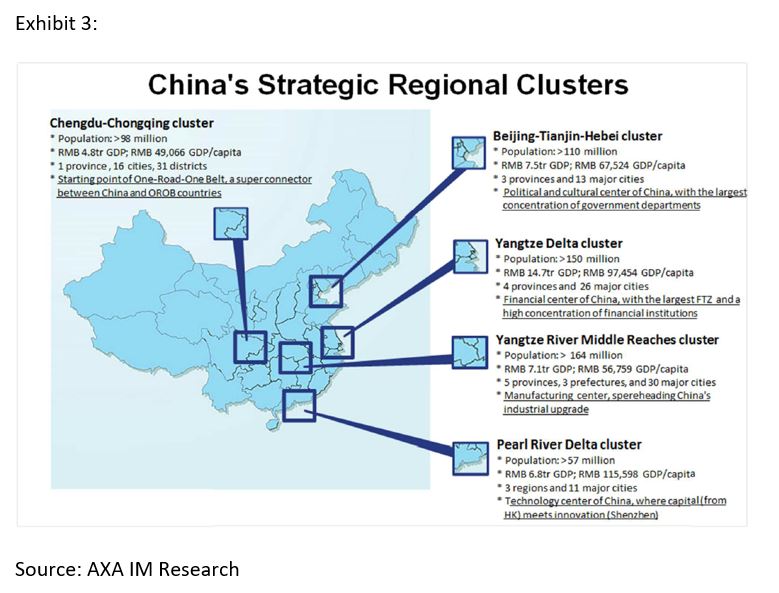

Some city clusters in China are attracting more population inflows and serve as strong urbanisation drivers due to their unique strategic position, including the financially-focused Yangtze River Delta region and technology-focused Pearl River Delta region. We believe properties in these regions are usually backed by more solid demand – that is, population inflow - than other areas in China and potentially present better investment opportunities.

Too big to fail?

Given its size and importance, China’s property market is highly regulated and, therefore, sensitive to policy changes. As a key pillar in the Chinese economy, real estate investment accounted for 7% of China’s GDP in 20196 , and over 24% when including both upstream and downstream activities in the industry chain, such as interior decoration, household consumption, etc.7

In addition, local governments’ fiscal income also largely relies on real estate-related sectors. In 2018, real estate related income contributed circa 52.7% of local governments’ fiscal income8 , testifying to the local economy’s heavy dependence on the real estate sector.

The property sector is, as a result, cyclical in nature. The Chinese government is actively using regulatory instruments, including home purchase restrictions and macro credit tightening, to manage supply and demand in real estate as part of its overall economic control.

While Chinese properties’ high sensitivity to changing policies pose a major challenge, the policies do tend to provide a certain level of downside mitigation.

Flexible, straightforward and more transparent

Chinese developers’ willingness to tap into offshore liquidity at a higher cost to refinance has established them as key players in the Asian high yield market. At the same time, the high leverage of Chinese property developers has long been an unnerving risk factor to many investors. That said, in the four years to the end of 2019, there has only been one default from the offshore Chinese property sector among a total of 26 defaults in the broader Asian US dollar credit market.9

On the other hand, property developers, compared to other industrial sectors, are potentially able to be more flexible with cash flow control as they can easily slow down their land acquisition when the market stagnates. Their balance sheets are relatively straightforward, with all the sales records, inventory and land values easily accessible. As most property developer issuers are listed in either China’s H-share or A-share markets, they also tend to be more transparent and timelier when communicating to investors. All these factors can help market participants make a better-informed judgement on the potential default risks.

Opportunities amid COVID-19 in the Chinese property sector

We expect more consolidation in the sector as companies navigate their way through the pandemic, and more divergence between different regions within China. In terms of fundamentals, we favour developers with more exposure in the larger tier one and tier two Chinese cities and solid land bank profiles in both size and location. Commercial names - for example mall operators and logistic centres - on the other hand, might face some pressure due to their exposure to the heavily-impacted retail sector during COVID-19.

We also believe that short-dated bonds of financially sound issuers in the Chinese property sectors are better positioned to be cushioned from the worst impact of the coronavirus. High yield issues maturing within four years should potentially perform better than longer-dated issues as their performance is less vulnerable to spread widening. As the Chinese government is still limiting new offshore issuances for refinancing purposes only, we don’t expect much more bond supply from Chinese property firms this year. In the existing pool, short-dated Chinese property bonds should be well-supported in the near- to medium-term.

- QXNpYSBVU0QgQ3JlZGl0IE1hcmtldCwgQSBTdGF0aXN0aWNhbCBDaGFydCBCb29rOiAxSCAyMDIwIGJ5IEpQIE1vcmdhbi4gRGF0YSBhcyBvZiBKdW4gMzAsIDIwMjA=

- QXNpYSBVU0QgQ3JlZGl0IE1hcmtldCwgQSBTdGF0aXN0aWNhbCBDaGFydCBCb29rOiAxSCAyMDIwIGJ5IEpQIE1vcmdhbi4gRGF0YSBhcyBvZiBKdW4gMzAsIDIwMjA=

- aHR0cHM6Ly93d3cuc2NtcC5jb20vYnVzaW5lc3MvYXJ0aWNsZS8yMTc0ODg2L2FtZXJpY2FuLWRyZWFtLWhvbWUtb3duZXJzaGlwLXF1aWNrbHktc3dlcHQtdGhyb3VnaC1jaGluYS13YXMtaXQtdG9vLW11Y2g=

- aHR0cDovL3d3dy54aW5odWFuZXQuY29tL2VuZ2xpc2gvMjAyMC0wMS8xOS9jXzEzODcxODQ1MC5odG0=

- aHR0cHM6Ly9maW5hbmNlLnNpbmEuY29tLmNuL2NoaW5hL2duY2ovMjAxOS0wNC0wOC9kb2MtaWh2aGlxYXgwOTU5ODIyLnNodG1s

- aHR0cDovL3d3dy5zdGF0cy5nb3YuY24vdGpzai96eGZiLzIwMjAwMS90MjAyMDAxMTdfMTcyMzU5MS5odG1s

- aHR0cHM6Ly93d3cuc29odS5jb20vYS8zODU1NDg1NDdfMTIwNjIxOTU0

- aHR0cHM6Ly93d3cuc29odS5jb20vYS8zODU1NDg1NDdfMTIwNjIxOTU0

- UmVwb3J0OiBBc2lhIENyZWRpdCBPdXRsb29rIGFuZCBTdHJhdGVneSAyMDIwLCBKUCBNb3JnYW4sIEphbiAyMDIw

Not for Retail distribution

This document is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document. Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ. In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.