Coronavirus and emerging markets: A three-tier challenge

- 22 February 2021 (5 min read)

The path of economic recovery from the coronavirus pandemic will depend on a number of factors but the primary focus right now is the vaccination of the global population. This should allow business activity to resume and economies to open back up, paving the way for a potentially robust rebound in economic growth.

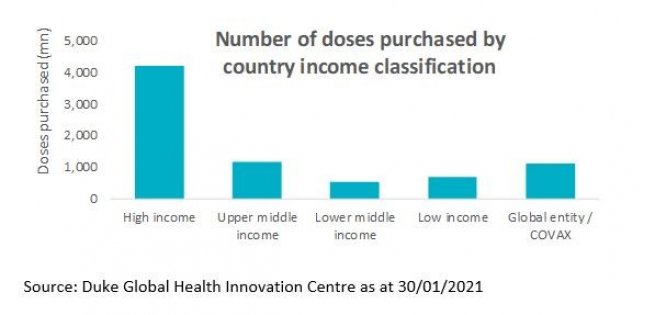

However, while the US, European Union and UK are among the countries that have already purchased hundreds of millions of doses of coronavirus vaccines, what is perhaps less clear is the degree to which emerging market (EM) countries have access.

What seems to be emerging is three tiers of countries, which are likely to have different levels of access to the vaccine. First there is a top tier of upper middle-income countries such as Brazil, Mexico and Indonesia, which are likely to have sufficient resources to secure a good pipeline. These three nations alone have already ordered almost 700 million doses, representing more than 9% of the global supply1 . At the other end there are low income-countries which will hopefully be assisted by organisations such as the World Health Organization and other philanthropic initiatives. Then there is a middle tier of nations which do not have the necessary resources to secure meaningful orders but are also lacking the support provided to low income countries. It is this tier, containing countries such as Sri Lanka, Ukraine and Azerbaijan, that perhaps will continue to suffer the most.

- U291cmNlOiBEdWtlIEdsb2JhbCBIZWFsdGggSW5ub3ZhdGlvbiBDZW50cmUgYXMgYXQgMzAvMDEvMjAyMQ==

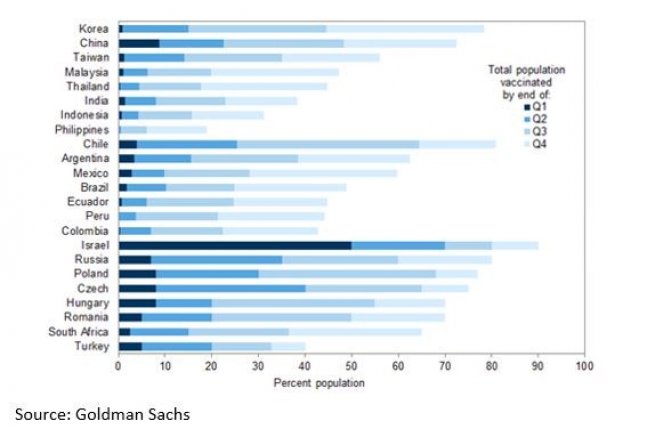

But while securing vaccines is one issue, another is overcoming supply constraints and being able to actually administer the doses. Here again there has been huge variation across developing countries. Some have made excellent progress, with Israel leading the way globally, having now vaccinated over 50% of its population, closely followed by the United Arab Emirates at around 35%2 .

However, most EM countries are lagging behind the vaccination levels in developed markets and many are not expected to achieve a 50% vaccination rate until late 2021. For example, despite securing a large order, Brazil has currently only received eight million doses for its 213 million-strong population, with 100 million doses negotiated with AstraZeneca not expected to be delivered until July.

- U291cmNlOiBHb2xkbWFuIFNhY2hzIGFzIGF0IDI5LzAxLzIwMjE=

There are additional factors for investors to consider such as how ready healthcare systems are to deliver mass vaccination, and the willingness of the population to accept it. Here EMs may have an advantage given the typically heightened awareness for vaccinations in areas such as Africa, while certain countries such as Brazil also have a good history in this field.

In addition, other vaccines such as those from Novarax, Johnson & Johnson and Russia’s Sputnik V are also entering the picture, and there are currently reported to be over 10 vaccines in Phase 3 trials which may help to improve supply. Meanwhile China has been publicly quiet on its vaccination policy and trials are fragmented at this stage. Given its industrial power and manufacturing capacity, many EM countries are looking at China for a cheap and available alternative in the coming months, which may also help to improve access to the vaccine.

What does this potentially mean for investors?

These variations in supply and potential for rollout emphasise the need to assess the EM debt universe on an individual basis and for investors to closely watch the rate that each country is able to administer the vaccine. For example, countries highly dependent on tourism may continue to suffer if they are unable to reach high vaccination levels and travellers do not feel safe. Domestic consumption is likely to be highly variable depending on what sectors can open up, how many people can gather and so on. The resumption of developed market growth will also be key as EM exporters to these countries could potentially start to benefit if production begins to ramp up.

We continue to have a preference for debt issued by corporates in higher/middle income countries that are well resourced and can potentially expect to return to higher levels of mobility sooner. We are very selective in lower income countries given their challenges in rolling out the vaccine, and prefer those supported by multinational organisations. If mobility is able to pick up in emerging markets as the rate of vaccination increases, this could potentially provide a big boost to market sentiment that could continue to drive flows towards the asset class and elicit further spread tightening in the first half of 2021.

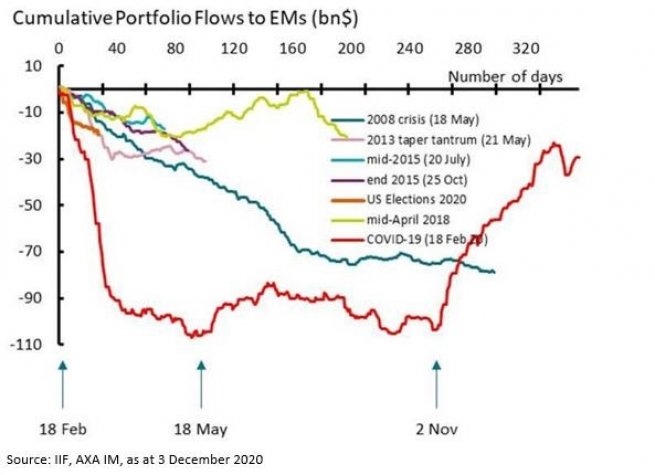

The chart below shows how investment flows into – and out of – emerging market debt has varied during different episodes of volatility. For example, the start of the 2008-09 global financial crisis was marked by a steady stream of outflows. However, during the coronavirus pandemic outflows have reversed significantly since the development of vaccines, indicating a significant swing in sentiment.

Finally, as economies begin to recover this should put some upward pressure on inflation and allow emerging market central banks to begin to normalise monetary policy, paving the way for asset purchases to begin to taper and interest rates – and therefore bond yields - to eventually slowly rise.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.