Growth is what you buy, value is what you get

- 02 June 2021 (5 min read)

Fortune has favoured the value investor over the past six months or so. The announcement and subsequent rollout of vaccines has led to a sharp outperformance for value stocks since the end of October 2020, with sectors such as banking, energy, mining and tourism & leisure making up for poor performance from the initial impact of COVID-19.

We offer some thoughts below around the value/growth debate in the UK from our perspective as investors that seek growth at a reasonable price. Broad value outperformance naturally poses a challenge to our portfolios, but we believe our strategies are attractively positioned.

At times like these, the importance of sticking to our process is critical. End-investors can make their own decisions about tactical opportunities but there are strong reasons to believe in the longer-term outperformance of businesses that are increasing their economic output, and questions around the shorter-term desirability of value.

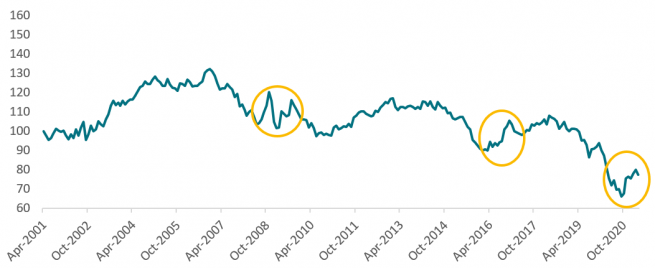

Déjà value?

This is not the first time that we have seen a period of sharp value outperformance. Looking at the data, there have been four major episodes of value outperformance over the past 15 years, mostly short lived. 2008 and 2009 both saw value outperform on hopes that the economy had seen the worst of the financial crisis, while 2016 saw strong absolute and relative performance as the global economy entered into a cyclical upswing and commodity stocks bounced off their cycle lows. The current period of outperformance has been the strongest, perhaps because of the extent of the lows reached in 2020, and the size of the subsequent stimulus.

Table 1: Value/growth outperformance since the Global Financial Crisis

| From | To | Value vs. growth performance | Absolute value performance | Absolute growth performance | Months of value outperformance | Months for growth to recover |

| 31 Jul 2008 | 30 Nov 2008 | 11.8% | -13.3% | -25.1% | 4 months | 3 months |

| 31 Mar 2009 | 31 Aug 2009 | 16.7% | 37.7% | 21.0% | 5 months | 7 months |

| 31 May 2016 | 31 Dec 2016 | 16.0% | 23.8% | 7.8% | 7 months | 32 months |

| 30 Oct 2020 | 31 Mar 2021 | 19.6% | 29.7% | 10.1% | 5 months | ? |

Source: AXA IM, FactSet. May 2021. Value and growth performance represented by MSCI UK Value and MSCI UK Growth.

Past performance is by no means a guarantee of future results, but sharp value outperformance has generally been short lived over the past ten years or so. Growth has on the whole recovered ground quickly, although 2016 represents a notable exception when it took almost three years to recover (those 32 months cover a period when growth was still outperforming, it just took longer to recover its relative outperformance in total). Of course, there are also longer-term periods when value outperforms (see chart below) but growth investors have still done better over the past two decades.

Caution now warranted?

The value/growth debate is naturally tied up with ideas of a regime shift, with inflation moving persistently higher and labour potentially getting the upper hand over capital. Value’s outperformance so far, however, appears to owe more to a reappraisal of the economic fallout of the pandemic rather than a fundamental change in the economy.

The banking sector is a good example of this. UK banks made significant provisions for bad debts at the start of the pandemic, with new accounting standards forcing them to set aside proceeds for bad debts upfront, rather than writing off the value of bad loans over a prolonged period. With the economic damage proving less severe than feared, these provisions are now being released, freeing up capital for dividends and share buybacks and driving a re-rating in bank valuations.

Crucially, however, banks continue to face the same long-term challenges as they did before the pandemic. Many struggle to make a decent return above their cost of capital and while higher interest rates would help to improve net interest margins, the Bank of England does not appear to be in a hurry to raise rates any time soon. From a naïve price perspective, there is still room for the FTSE 350 Banks index to recover its pre-COVID high, but there is probably not a lot of upside left.

While it might seem counterintuitive, we believe growth companies are better positioned to withstand the next few years than value stocks. Many of the trends from before the pandemic – and indeed strengthened by it – will continue to play out over the coming years, such as increasing digitalisation, the rising importance of brands, intellectual property or other intangibles, or even market consolidation. Growth companies tend to be on the right side of these secular shifts, have stronger balance sheets to either adjust to or exploit changes, and can use their pricing power to offset higher input costs.

Focus on the stock picking

Where we do take exposure to the banking sector, we prefer companies that have an opportunity to thrive for reasons over and above the prevailing macro environment. OneSavings Bank, for example, is seeing strong end-demand for its services as a niche lender – primarily focused on lending to professional landlords within the UK buy-to-let segment, and specifically those with a multi-property portfolios. This is an area of the market that the main high street lenders have exited, naturally leading to less competition for OneSavings Bank and the ability to generate superior returns.

In addition, we do not disregard a business just because it has a low valuation. We want to buy attractively priced growth stocks, not growth at any price. A good example of this is TI Fluid Systems, which essentially makes fluid delivery and carrying systems for cars. The business trades at a low price/earnings ratio as the transition to electric vehicles will ultimately render its petrol product line irrelevant.

We think the market is underappreciating the potential for TI Fluid Systems to transition to the world of hybrid electric vehicles and full battery electric vehicles by progressing products such as its battery cooling lines and blow-moulded plastic manifolds, with the company leveraging its existing relationships in the automotive industry.

To generate returns, grow your output

The question of what drives returns sits at the heart of the value/growth debate. Value investing, by its nature, relies on businesses whose value can re-rate higher as the market recognises a company is priced too cheaply. This puts investors on a constant treadmill of trying to find lowly valued companies before the market does, conscious that just buying lowly valued companies could lead to investing in value traps (some companies are ‘cheap’ for a reason).

Growth companies are arguably more in charge of their destiny: as they organically grow their output over time; this gets reflected in a rising share price. While short-term underperformance is never welcome, we believe that times like this allow us to add to opportunities, and help to demonstrate the consistency of our investment process and the strength of our commitment to it.

Stocks mentioned in this article are for illustrative/informational purposes only and should not be taken as a recommendation to buy or sell.

Why UK equities?

The UK equity market is a key geographical market and source of potential returns for investors globally

Find out moreVisit the fund centre

Access our UK equities strategies.

The aim of this Fund is to provide long-term capital growth.

View fundsThe aim of this Fund is to provide long-term capital growth.

View fundsThe aim of this Fund is to provide long-term capital growth.

View fundsNot for Retail distribution

This document is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This promotional communication does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee that forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Before making an investment, investors should read the relevant Prospectus and the Key Investor Information Document / scheme documents, which provide full product details including investment charges and risks. The information contained herein is not a substitute for those documents or for professional external advice.

The products or strategies discussed in this document may not be registered nor available in your jurisdiction. Please check the countries of registration with the asset manager, or on the web site https://www.axa-im.com/en/registration-map, where a fund registration map is available. In particular units of the funds may not be offered, sold or delivered to U.S. Persons within the meaning of Regulation S of the U.S. Securities Act of 1933. The tax treatment relating to the holding, acquisition or disposal of shares or units in the fund depends on each investor’s tax status or treatment and may be subject to change. Any potential investor is strongly encouraged to seek advice from its own tax advisors.

Past performance is not a guide to current or future performance, and any performance or return data displayed does not take into account commissions and costs incurred when issuing or redeeming units. The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested. Exchange-rate fluctuations may also affect the value of their investment. Due to this and the initial charge that is usually made, an investment is not usually suitable as a short term holding.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.