Charting the post-virus growth and inflation outlook – and looking ahead to a climate-aware era

- 29 April 2021 (5 min read)

As part of a two-part webinar series for Insurance Ireland members, “Evolving economies - building resilience for a sustainable recovery and growth", AXA IM’s Head of Macro Research, David Page discussed:

- How central banks, including the ECB, are seeking to support economic recovery against a backdrop of mounting inflation concerns

- How the global economy might adapt to trends in digitalisation, working patterns, business models and global supply chain structures that have been accelerated by the pandemic

- How fiscal stimulus measures and long-term strategic planning around the world might help to ‘green the recovery’ that emerges post-virus, particularly given policy momentum around climate change

Highlights:

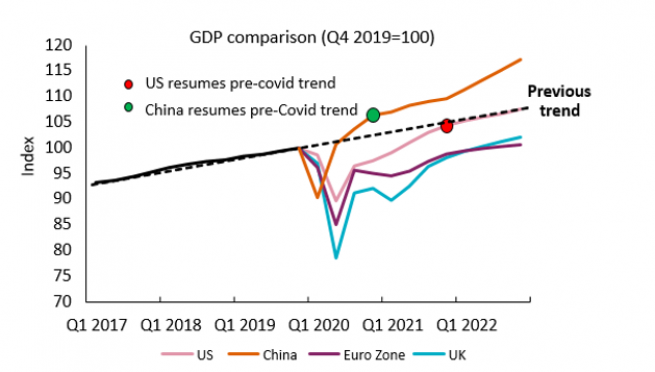

Optimism has been building around the pace of the recovery after an extraordinary year. China has managed to rebound very quickly by tightly managing the initial stages of the virus and any subsequent outbreaks. The US, meanwhile, has been buoyed by progress in the vaccine rollout and aggressive stimulus measures. We believe the US should regain trend growth towards the end of the year. Europe, however, has been far more subdued. Despite a relatively slow vaccine rollout, the European Union (EU) could still meet its target of inoculating 70% of people by the end of the third quarter (Q3), but this does suggest the possibility of strict restrictions through the summer, a risk to the outlook. The UK has fared better but still has the ripples of Brexit to contend with, which will likely soften the pace at which it can regain trend growth rates.

We expect to see the differential between US and EU growth narrow over time given the nature of stimulus packages in each region. The Eurozone fiscal stimulus is large and long term, designed to deliver a planned and consistent boost to growth – some countries will receive a boost that should deliver extra growth in excess of 3% per annum over the next five years. So, while short-term effects may be limited, we see room for optimism in the medium term. We also note that with the stimulus is funded on a mutualised debt basis – that should bode well for the stability of the monetary union more broadly.

For the time being, the Eurozone response has been dwarfed by that in the US where stimulus measures have equated to about 13% of GDP in total in the last six months. The latest $2.3trn package put forward by President Joe Biden’s administration also leans more towards investment-focused measures. This has represented a stark contrast to the response seen after the global financial crisis in 2008/2009, when governments chose austerity in pursuit of a short-term reduction in deficits and debt. Given the successful effect of the US stimulus in 2020/2021, it may be a model that will be replicated by others seeking to boost growth and long-term productivity.

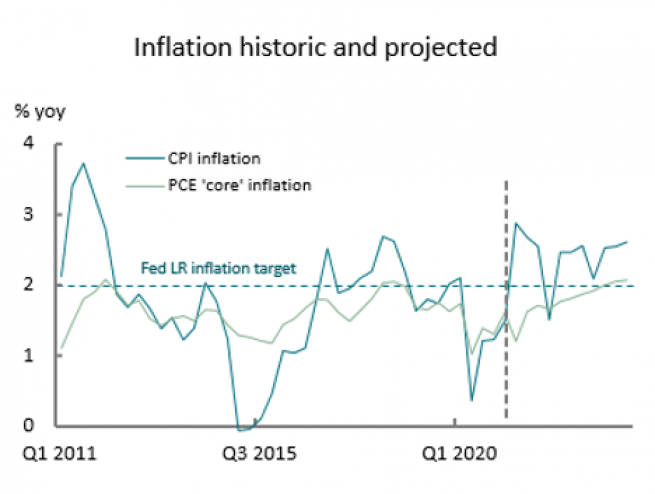

While confidence about the recovery is high, there is less certainty about the path of inflation. Historically, pandemics have had a depressing effect on prices, and despite a popular view that the effect of quantitative easing (QE) on money supply could drive inflation, that is not borne out by the data. There are competing effects at work here – while the pandemic may be disinflationary, the response to it can change all that. In the US though, core Personal Consumption Expenditures (PCE) inflation has been pretty steady because cyclical factors account for less than 40%, implying that any overshoot may be muted.

We expect a rise in US inflation, but this should be sustainable and gradual, with core PCE inflation reaching 1.8% at end-2021, 2% by end-2022 and 2.3% by end-2023. Consumer Price Inflation (CPI) will be more volatile. Markets also have to factor in an interesting change in policy from the US Federal Reserve (Fed), which has not only started to aim for an overshoot of its 2% target but has said it will stop attempting to anticipate inflation, responding to rising prices only when they show up in the data. This could be an important difference as the anticipation approach has tended to subdue inflation effects.

The discussion around prices has affected US bond yields where we have seen a steady rise as inflation expectations have risen. Now too real interest rates are moving higher, signalling that the market is not taking the Fed at its word. The central bank has guided towards no rate hikes before 2024 but the consensus view is for two hikes in 2023. The more people expect the Fed to move earlier, then the more pressure will come on bond yields. In the Eurozone the inflation outlook is far more subdued considering the likelihood of a softer recovery. The European Central Bank expects 1.4% in 2023, materially lower than target. Japan is in similar position, even after 10 years of QE, highlighting that future inflation is likely to be driven by regional idiosyncrasies. Looking more broadly, the pandemic has muddied the waters around trends previously seen as definitively disinflationary, such as globalisation, technology and demographics.

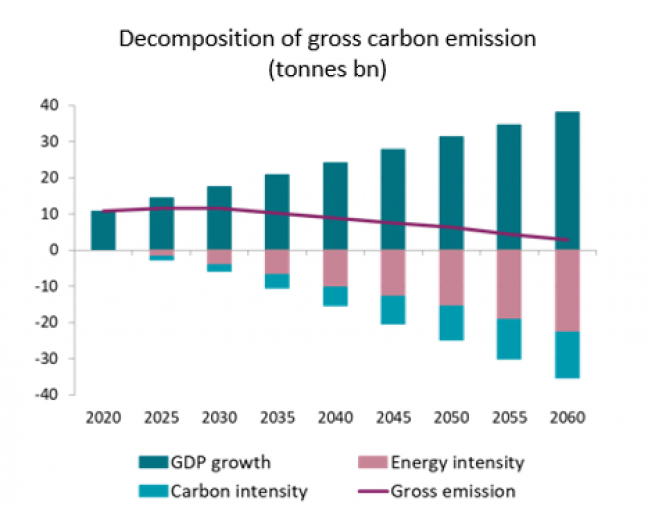

As we look beyond the pandemic recovery, and into the decades ahead, one theme dominates: Climate. In the US, $800bn of the latest $2.3trn stimulus package is earmarked for green investment to drive jobs, and a recent climate summit hosted in Washington saw new and expanded commitments on the path to ‘Net Zero’. Perhaps most significant has been a commitment from China for a carbon neutral economy by 2060. This follows an expected peak in emissions in 2030 and as such represents a far more dramatic cut than for other nations. China’s ambition will be expensive and involve writing-off relatively new investments in things like coal power. For the moment there is political consensus across large economies, and this has significant implications for long-term investors, maybe even more so if that consensus wobbles and economies start to move along different paths.

In Part II of the series, “Embracing change: equity investing and structural, long-term growth opportunities”, Amanda O'Toole, Portfolio Manager discusses key themes from the past 12 months and their implications for investors including:

- How lockdown has increased digital connectivity, transforming the way we work, socialise, shop, exercise and educate ourselves. These are not completely new habits, but COVID-19 has sharply accelerated the pace of the shift online.

- How the pandemic has highlighted the need for supply chain resilience among businesses, which is further driven by wider issues such as extreme weather conditions and geopolitical risks.

- How, as technology progresses and consumers become more climate aware, we are seeing a clear shift towards the adoption of cleantech by corporates and consumers. Corporates are increasingly committing to net zero targets and developing or buying innovative solutions to address their environmental challenges.

What is thematic investing?

The evolving economy is all about identifying companies that are tapping into multi-decade demographic and technological changes, regardless of their region or sector classifications

Not for Retail distribution

This document is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.